Spring is in full swing, and the housing market is picking up along with it. And if you’ve been wondering whether now is the right time to buy or sell, here’s the inside scoop on why this spring may be a great time to make your move.

1. There Are More Homes for Sale

After a long stretch of tight inventory, the number of homes for sale is finally improving. According to recent national data from Realtor.com, active listings are up 27.5% compared to this time last year.

Look at the graph below and follow the green line for 2025. You can see, even though inventory levels still haven’t returned to pre-pandemic norms (shown in gray), that number is higher than it has been going into the spring market over the past few years (see graph below):

Buyers: This means you have more choices, and you can be more selective.

Sellers: With more homes available than in recent years, you’re more likely to find what you’re looking for when you move. And knowing that inventory is still below more normal levels means there will be demand for your home when you sell it, too.

2. Home Price Growth Is Moderating

As inventory grows, the pace of home price growth is slowing down – and that will continue into the spring market. This is because prices are driven by supply and demand. When there are more homes for sale, buyers have more options, so there’s less competition for each house. Rising supply and less buyer competition causes price growth to slow, but it should still remain positive in most markets. As Freddie Macsays:

“In 2025, we expect the pace of house price appreciation to moderate from the levels seen in 2024, while still maintaining a positive trajectory.”

And while prices aren’t dropping at the national level, every market is different. Some areas are seeing stronger price growth, while others are cooling off or even seeing some price declines.

Buyers: The slower pace of growth means prices aren’t rising as quickly as before – and that’s a relief. Any home you buy now is likely to appreciate in value over time, helping you build equity.

Sellers: While prices are still rising, you might need to adjust your expectations. Overpricing your house in a more balanced market could mean it takes longer to sell. Pricing your house competitively is going to be key to attracting offers.

3. Mortgage Rates Are Stabilizing

One of the biggest hurdles for buyers over the past couple of years has been high, volatile mortgage rates. But there’s some good news – overall, they’ve stabilized in recent weeks – and have even declined a bit since the beginning of this year. And while that decrease hasn’t been a big drop, stabilizing mortgage rates has helped make buying a home a bit more predictable. According to Selma Hepp, Chief Economist at CoreLogic:

“With the spring homebuying season upon us, the recent improvements in mortgage rates may help invite homebuyers back into the market.”

Buyers: When mortgage rates are more stable, it’s easier to plan ahead because you have a better idea of what your future payment might be. But remember, rates will continue to be volatile. So, lean on your agent and your lender to make sure you know what the latest mortgage rate means for you.

Sellers: Slightly lower rates that are starting to stabilize are encouraging more buyers to move forward with their plans. That’s good for demand when you’re planning to sell your house.

4. More Buyers Are Returning

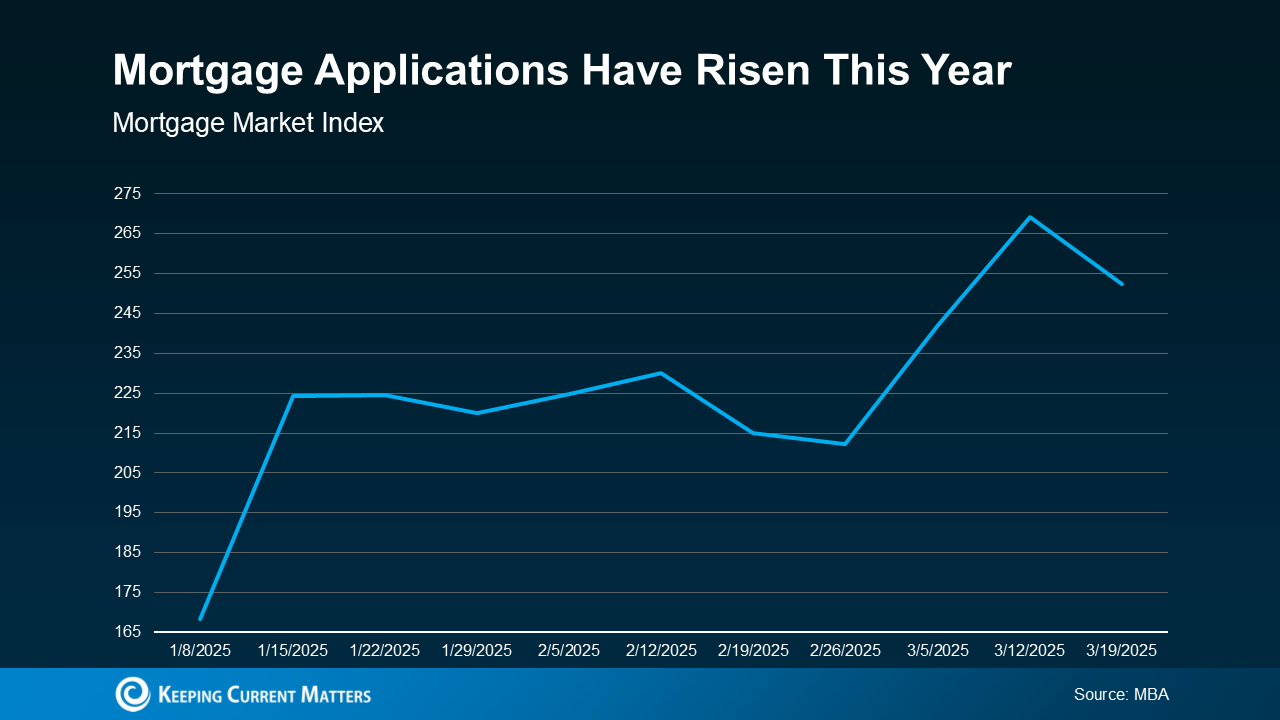

With more inventory, slowing price growth, and stabilizing mortgage rates, buyers are gaining confidence and coming back into the market. Demand is picking up, and data from the Mortgage Bankers Association (MBA) shows an increase in mortgage applications compared to the start of the year (see graph below):

Buyers: Acting sooner rather than later could be a smart move before your competition heats up even more.

Sellers: This is great news for you – more buyers mean a better chance of selling your house quickly.

Bottom Line

Do you have questions about what the spring market means for you? Connect with a local real estate agent and talk about how to craft your plan this season.

Who wants to go strawberry picking? Have you ever wanted to pick your own fruit, fresh from the farm? Is there any other family activity that’s as fun — and delicious? Not to mention educational, since you can help your kids learn about where their food comes from.

These hard-working family farms, near Los Angeles, and all over Southern California, offer the chance to go strawberry picking (or any other fruit in season) and enjoy seeing your food in its natural state. Sometimes called “U-Pick,” the idea is you and your family will do a bit of work and get to eat all the fresh fruit you gather.

In Los Angeles, we are lucky to be able to pick fruit all year long, nearby, within just a couple hours’ drive. The time to pick strawberries is in the spring. You pick cherries in the early summer, and apple picking happens in the fall. But there are also blueberries, apricots, plums, and pumpkins, too — just to name a few others. Plus there are all the vegetables!

Let’s go pick strawberries! Photo credit: California Strawberry Commission

Have you been searching for “Strawberry Picking Near Me in SoCal?” Or wondered about a “Strawberry Farm near me?” We’ve got you covered! You’ll find a U-Pick Farm Near Me on this awesome Google Map.

Pick Your Own Fruit: Locally Grown and Farm Fresh

We’ve got a great big list of farms to take kids where you can all pick your own fruits and vegetables. You can find U-Pick Farms in Orange County, San Bernardino, Ventura, and even San Diego County.

And if you’d rather not pick your own, most of these farms have terrific farm stands, some with drive-through, so you can get fresh fruit and veggies direct from the farm, whether you get your hands dirty or not.

Things to Know Before You Go

Wherever you go to pick, and whatever fruit you choose, we hope you and your family have a great time!

Fruits they grow: Strawberries, as well as other fruits and vegetables.

Farm Market Hours: Wednesday – Saturday 10:00 a.m. to 4:00 p.m. and Sunday 11:00 a.m. to 4:00 p.m. (Closed Mondays and Tuesdays)

U-Pick Information: $10 Admission. The picking season generally starts about April 15th each year. Be sure to check their website as well as Instagram and Facebook pages for the most up-to-date information.

Underwood: Moorpark Farm Center 3370 Sunset Valley Road, Moorpark, CA 93021

(805)529-3690

info@underwoodfamilyfarms.com

Fruits they grow: Strawberries, as well as many other fruits and vegetables including tomatoes, cauliflower, carrots, lettuce, and much more. Underwood is well-known for its seasonal festivals (Springtime Festival, Fall Harvest, and Christmas on the Farm).

Moorpark Farm Center Hours: Daily 9:00 a.m. to 6:00 p.m. Closed on certain holidays, closing early on the days before certain holidays. Check their website for details.

Underwood: Somis Farm Center

5696 E. Los Angeles Ave, Somis, CA 93066

(805) 386-4660 info@underwoodfamilyfarms.com

Fruits they grow: The Somis location has been open since 1980 and offers a variety of fruits, vegetables, and specialty food items (jarred products, pickled vegetables, dried beans, honey, farm fresh eggs, flowers, and more).

Pick-your-own strawberries, blueberries, raspberries, blackberries, tangerines, and figs are offered by the season. Strawberries are usually available from March through mid-June.

When you go, be sure to visit the animal center where you can see pygmy goats, alpacas, sheep, and chickens.

Somis Farm Market & Animal Center Hours: Daily 9:00 a.m. to 5:00 p.m. (6:00 p.m. as of 3/9/2025). Closed on certain holidays, closing early on the days before certain holidays. Check their website for details.

This farm has “U Pick Strawberries Near Me” if that’s what you’re looking for! Photo credit: California Strawberry Commission

In the fall, try our list of Farms for Apple Picking, many of which are located in San Bernardino County.

Pick Your Own Fruit — San Bernardino County

Los Rios Rancho 39611 Oak Glen Rd., Oak Glen, CA 92399

(909) 797-1005

info@losriosrancho.com

Fruits they grow: Los Rios Rancho was established in 1906 and is known as the “largest and oldest Apple Farm in Southern California.” While they are known as an Apple Farm, Los Rios Rancho includes more than 150 acres and offers a variety of organically-grown berries, pumpkins, corn, and more. More than three acres are dedicated to strawberries, and picking season usually starts in mid-May. They also host a number of special events and festivals throughout the year.

Current Hours: Thursday – Tuesday 10:00 a.m. to 5:00 p.m. (They are closed on Wednesday and they are temporarily closed on Thursday and Friday as well)

Family Farms

13406 Cypress Ave., Chino, CA 91710

(909) 717-5871

Fruits they grow: Family Farms in Chino welcomes families to pick their own strawberries seven days a week from 7:30 a.m. to 5:00 p.m. No reservation is needed. $10 per person, which includes entry and a basket of strawberries. For the most up-to-date information, be sure to check their Instagram and/or Facebook pages.

Fruits they grow: In late spring and early summer, you can pick Nicolson’s juicy, delicious strawberries from Thursday through Sunday, 10:00 a.m. to 4:00 p.m. Check their Facebook or Instagram pages for more information.

Berry Picking Farms — Orange County

Tanaka Farms 5380 3/4 University Dr., Irvine, CA 92612

(949)653-2100

info@tanakafarms.com

Fruits they grow: Tanaka Farms is a thirty-acre, family-owned and operated farm, established in 1940. Families can opt to take a Strawberry Picking Tour, which includes a guided wagon ride with multiple stops, allowing families the opportunity to pick fruit right where they’re growing. Strawberry Picking Tours are offered on Saturday and Sunday, beginning March 1st, 2025. Reservations may be made online. You can also opt to visit and pick strawberries without the tour. Tanaka Farms is also well-known for its seasonal festivals and many family-friendly events offered throughout the year.

Produce Market Stand & Gift Shop Hours: Daily from 9:00 a.m. to 5:00 p.m.

(Keep in mind — all tours and activities require a reservation.)

South Coast Farms

33201 Ortega Hwy, San Juan Capistrano, CA 92675

(949)661-9381

southcoastcsa@gmail.com

Fruits they grow: South Coast Farms was established in 1996 and is San Juan Capistrano’s only Family Farm. They grow all of their produce without the use of pesticides or fungicides. South Coast Farms U-pick is currently open on Thursday through Sunday from 10:00 a.m. to 4:00 p.m. Be sure to check their Instagram and Facebook pages for the latest updates.

The Ecology Center

32701 Alipaz St., San Juan Capistrano, CA 92675

(949) 443-4223

Fruits they grow: The Ecology Center provides an “immersive, interactive farm experience featuring educational programming and a hands-on strawberry U-pick.” Using a field guide, families will first tour the farm and then go into the fields to “experience the bounty of the only Regenerative Organic strawberries available in Southern California.” Many special events are offered throughout the year including seasonal festivals, farm dinners, special children’s offerings, and more.

Hours: Farm Stand is open daily from 9 a.m. to 5 p.m.

U-Pick Strawberries is available on Saturday and Sunday ($15 per person) from 9:00 a.m. to 1:00 p.m.

Tickets are required and must be purchased in advance (free for children under 2).

Manassero Farms

33 Irvine Valley, Irvine, CA 92618

(949) 554-5103

Fruits they grow: Strawberry picking season at Manassero Farms has just begun. The Strawberry Picking Experience includes access to the field and a single 1-pound container. For those who do not wish to pick berries and would just like access to the fields, a ticket is required. Children under 2 are free. Reservations are required.

Hours: Open Monday through Saturday from 9:00 a.m. to 5:00 p.m.

Open on Sundays from 9:30 a.m. to 4:30 p.m.

Photo credit: California Strawberry Commission

Strawberry Picking — San Diego County

Carlsbad Strawberry Company

1050 Cannon Rd., Carlsbad, CA 92008

(760)603-9608

info@carlsbadstrawberrycompany.com

Fruits they grow: Carlsbad Strawberry Company has been growing strawberries for generations! U-Pick is predicted to open in late March or early April. Check the website for the latest information. And while you’re there, be sure to visit with the sheep, goats, and rabbits on the farm. Once the season begins, U-Pick is available daily from 9 a.m. to 5 p.m. Tickets may only be purchased on-site. (Visit in the fall, and you’ll find an epic Pumpkin Patch and corn maze.) They also have tractor rides and Bounceland, which will reopen soon and includes jump houses and slides for children.

Kenny’s Strawberry Farm

953 Rainbow Valley Blvd., Fallbrook, CA 92028

(888) 236-0101

info@kennysstrawberryfarm.com

Fruits they grow: Kenny’s Strawberry Farm has been growing delicious strawberries for over a decade. U-Pick opportunities usually open sometime in February or March each year. Be sure to check the website for the most up-to-date information and hours. (As of February 27th, 2025 the U-Pick Farm is closed for the season. According to Facebook, they are already sold out!)

The 65th Annual Garden Grove Strawberry Festival is scheduled for Friday, May 23rd (1 p.m. to 10 p.m.), Saturday, May 24th, and Sunday, May 25th (10 a.m. to 10 p.m. on both days), and Monday, May 26th (10 a.m. to 9 p.m.). This popular yearly event features carnival rides, live musical performances, vendor booths, games, and, of course, strawberries (and other non-strawberry food). Details, including parking information, are available online.

The California Strawberry Festival will take place on Saturday, May 17th, and Sunday, May 18th (10:00 a.m. to 6:30 p.m.). The Festival features over 40 food vendors, live musical performances, arts and crafts booths, and a Strawberryland for Kids (featuring rides, face painting, and more). Ticket information is available online.

Q: Is strawberry picking a good family activity?

A: Yes, you can pick strawberries with your kids, and you’ll all have fun.

Q: When is strawberry picking season?

A: Strawberry picking season varies by location and climate, but generally it occurs in the late spring and early summer months. In North America, strawberry picking season typically runs from late May to early July, although this can vary by region.

Q: What should I wear for strawberry picking?

A: It’s best to wear comfortable clothing that you don’t mind getting dirty, as well as closed-toe shoes. You may also want to wear a hat and sunscreen to protect yourself from the sun.

Q: What should I bring when picking strawberries?

A: You’ll want to bring a container to hold your strawberries, such as a basket or a plastic container with a lid. You may also want to bring water and snacks, as well as cash to pay for the strawberries.

Q: How do I know which strawberries to pick?

A: Look for strawberries that are fully red and plump. Avoid strawberries that are unripe or overripe. You can also gently squeeze the strawberry to see if it’s ripe – it should be slightly soft to the touch.

Q: Can I eat the strawberries while picking?

A: It’s generally okay to eat a few strawberries while picking, but be sure to ask the farmer or staff at the farm if it’s allowed. They may have specific rules about eating while picking.

Q: Can I bring my pet with me to pick strawberries?

A: It’s best to check with the farm beforehand, as some may not allow pets due to health and safety concerns.

Q: Can I bring my own containers to pick strawberries?

A: It’s best to check with the farm beforehand, as some may have specific rules about the types of containers that are allowed. They may also provide containers for you to use.

Q: How much do strawberries cost when picking your own?

A: The cost of strawberries can vary depending on the location and the farm. You can expect to pay by weight or by the container. Prices may also vary depending on the ripeness and quality of the strawberries.

Q: How long do picked strawberries last?

A: Picked strawberries will typically last for a few days in the refrigerator. It’s best to eat them as soon as possible for the freshest flavor. You can also freeze strawberries for longer storage.

Disclaimer: MomsLA has made every effort to confirm the information in this article; however, things can often change. Therefore, MomsLA makes no representations or warranties about the accuracy of the information published here. MomsLA strongly urges you to confirm any event details, like date, time, location, and admission, with the third party hosting the event. You assume the sole risk of relying on any of the information in our list. MomsLA is in no way responsible for any injuries or damages you sustain while attending any third party event posted on our website. Please read our Terms of Use which you have agreed to based on your continued use of this website. Some events have paid to be listed on MomsLA.

Springtime is upon us and the milder days of spring are a perfect time to do a thorough spring cleaning and perform home maintenance. After a long winter, it is a good idea to spend time on preventive measures to help maintain your home and property throughout the year. Tasks such as cleaning out your gutters, checking for dead trees and branches and cleaning and inspecting home mechanical and plumbing systems, such as heating and air conditioning equipment, can help make spring a season of safety.

Cleaning and maintenance of your home should be done inside and out. Although the tasks are different, checking to see if all the elements of your home are in good working order can help keep your family safe and your maintenance expenses lower over the long run. And if a task is overwhelming and you want to leave it up to the pros, call us for referrals!

Fri, Mar 14, 2025

The Irishman (Huntington Beach): Corned beef! True Irish! Sunday & Monday open at 11AM. 424 Olive Ave, Huntington Beach, CA 92648

Mickey’s Irish Pub (Fullerton): 𝐂𝐀𝐋𝐋𝐈𝐍𝐆 𝐀𝐋𝐋 𝐋𝐄𝐏𝐑𝐄𝐂𝐇𝐀𝐔𝐍𝐒! Grab your green gear and head on down to your favorite pub in Fullerton on #StPaddysDay! We’ve got a 𝐋𝐈𝐕𝐄 fiddler, bagpiper, 𝐆𝐑𝐄𝐄𝐍 𝐁𝐄𝐄𝐑, special Irish food menu & 𝐌𝐎𝐑𝐄! 𝐎𝐏𝐄𝐍 𝐀𝐓 9𝐀𝐌! 𝐀𝐑𝐑𝐈𝐕𝐄 𝐄𝐀𝐑𝐋𝐘 𝐓𝐎 𝐀𝐕𝐎𝐈𝐃 𝐋𝐈𝐍𝐄𝐒! 100 N Harbor Blvd, Fullerton, CA 92832

Bangers and Mash with Guinness Gravy and fried cabbage

Braised Lamb “Meat Pies”—-puff pastry with mashed potato base and braised lamb, carrots and celery

Jameson Whiskey Glazed Chicken Wings

Corned Beef Grilled Cheese on Marbled Rye with Irish Cheese

Caramelized Onion and Guinness Dip with Irish Soda Bread Crisps

Irish Popcorn with Jameson Caramel

Guinness Brownie with Nitrogen Ice Cream

122 N. Glassell St., Orange

Durty Nelly’s (Costa Mesa): St. Patrick’s Day menu! Green beer, $7 Jameson shots, Karaoke at 6pm. 2915 Red Hill Ave., Costa Mesa

Malarky’s (Newport Beach): We are kickin’ off St. Paddy’s Day at 6am! Enjoy pints of green beer, brunch, drink specials, shamrock shenanigans & 𝐌𝐎𝐑𝐄! 𝐃𝐎𝐎𝐑𝐒 𝐎𝐏𝐄𝐍 𝐀𝐓 6𝐀𝐌! 𝐀𝐑𝐑𝐈𝐕𝐄 𝐄𝐀𝐑𝐋𝐘 𝐓𝐎 𝐀𝐕𝐎𝐈𝐃 𝐋𝐈𝐍𝐄𝐒! 3011 Newport Blvd, Newport Beach, CA 92663

Muldoon’s Pub (Newport Beach): Get ready for the ultimate St. Paddy’s Day celebration at Newport Beach’s favorite Irish Pub! Join us starting at 9am on March 17 for shamrocks, shenanigans, and nonstop craic as we raise a pint to Ireland’s biggest day! We’ve got a special breakfast & lunch menu, a live bagpiper & fiddler, swag & more! Arrive early to the party to avoid lines, Sláinte! 202 Newport Center Drive, Newport Beach

Sidedoor (Corona del Mar): St. Pat’s Specials and Leprechaun Seamus O’Malley! Celebrate St. Paddy’s Day at SideDoor! Get ready for a night of Irish cheer! Join us on March 16th from 5:30 PM to 7:30 PM for an unforgettable St. Patrick’s Day celebration! Sing along to lively Irish tunes, feast on Corned Beef & Cabbage ($31) and SideDoor favorites, and hear whimsical folk tales from Seamus the Leprechaun!

$24 ticketed event | Family-style seating

Tullamore D.E.W. flights, Guinness on draft, and more!

Don’t miss this magical evening of music, stories, and Irish spirit!

3801 East Coast Highway, Corona Del Mar

The Original Patsy’s Irish Pub (Laguna Niguel): St. Patrick’s Day is quickly approaching! Here’s a fun lineup for March 15-17!

– March 15: live band, “No. 12 Saloon” – 8:00pm to 12:00am

– March 16: live band, “The Universals” – 4:00pm to 8:00pm

– March 17: Patsy’s opens at 11:00am, $10 All day access ticket to entertainment and festivities:

Face painting

Photo ops

12:00pm to 9:00pm, Kitchen serving special event day menu

1:00pm to 3:00pm, “Plucky Charms” band performs

4:00pm to 8:30pm, “Selly & the Strays,” band performs

9:00pm to 1:00am, DJ and Dancing

28971 Golden Lantern #108, Laguna Niguel

Heritage Barbecue (San Juan Capistrano): Make your own luck this 𝗦𝘁. 𝗣𝗮𝘁𝗿𝗶𝗰𝗸’𝘀 𝗗𝗮𝘆 weekend with these chef-curated specials. Available until sell-out Saturday, March 16th and Sunday, March 17th! 31721 Camino Capistrano, San Juan Capistrano

Hennessey’s (several locations): Get ready for St. Patrick’s Day Weekend at Hennessey’s Tavern! March 14-17: Hennessey’s Tavern’s Famous CORNED BEEF & CABBAGE Plate is back for just $25! Served all day & night from March 9–17. Don’t miss out—grab yours before it’s gone for another year! Join us as we kick off the celebrations early because when St. Paddy’s falls on a Monday, the whole weekend turns green. Make Hennessey’s your St. Patrick’s Day headquarters, and let’s paint the town green together! 34111 La Plaza, Dana Point; 31761 Camino Capistrano, San Juan Capistrano; 213 Ocean Ave., Laguna Beach; 1773 Newport Blvd., Costa Mesa; 143 Main St., Seal Beach

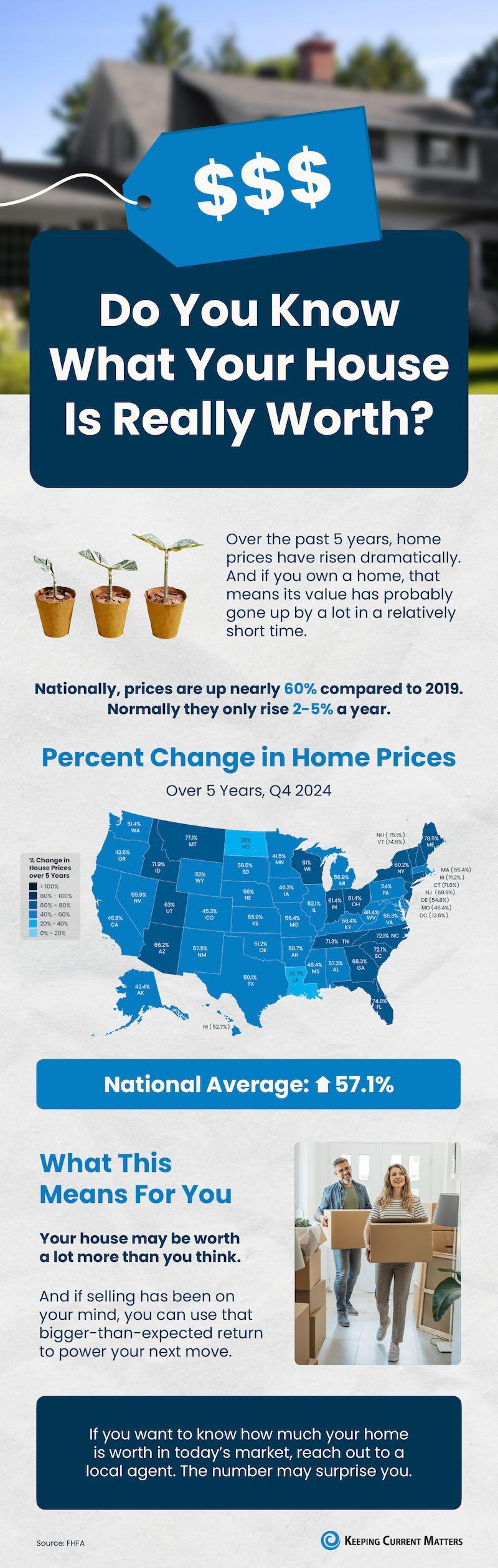

Over the past 5 years, home prices have risen dramatically. If you own a home, that means your house may be worth a lot more than you think.

Nationally, prices are up nearly 60% since 2019. And, if selling has been on your mind, you can use that bigger-than-expected return to power your next move.

If you want to know how much your home is worth in today’s market, reach out to CA Real Estate Group. The number may surprise you.

Let’s connect and plan your next steps. Find out if we’re the right real estate team for you!

One of the biggest benefits of going solar is that it’s pretty much a “set it and forget it” way to power your home with renewable energy. But for solar homeowners, depending on where you live, you’ll still need to clean your solar panels once or twice a year to ensure you’re getting the maximum energy benefit from your solar investment. Cleaning your solar panels is a relatively simple process though, and you can easily do it yourself or hire a professional service to take care of it for you.

Cleaning your solar energy system helps maximize your panels’ efficiency by allowing them to absorb the most sunlight possible. When dust or other particles cover your panels, it means they won’t be able to produce as much power — and ultimately that means you’ll lose some of the financial benefits of going solar. That’s why it’s important to keep up your solar panel maintenance, and clean them about every six months if you live in a dry or dusty environment.

In this article, we’ll answer some of the most common questions that solar panel system owners have about solar panel maintenance and how to clean them safely.

Key takeaways

Solar panels usually only need to be cleaned once or twice a year, or even less if it rains a lot where you live.

Cleaning your solar energy system helps maximize your panel efficiency by allowing it to absorb the most sunlight possible.

You can clean your solar panels yourself, or hire a professional cleaning service to do it for you.

Solar panels don’t require any special cleaning equipment and can be cleaned with basic tools you probably already have at home like a garden hose, rag, and dish soap.

Your solar panels need to be exposed to sunlight to produce power. If they get dirty or build up layers of grime and dust over time, those pollutants and particles will prevent your panels from absorbing as much sunlight as possible, which is known as soiling. In certain areas of the U.S., the energy lost from soiling each year is as high as 7%, according to the National Renewable Energy Laboratory (NREL).

But there’s good news, too. Solar panel cleaning is often unnecessary unless you live somewhere with high amounts of smog, dust, dirt, grime, or sand blowing around. In most areas of the country, occasional rain is typically enough to naturally and safely keep your solar panels clean and free of debris that could lower their energy production.

But a good clean every once in a while can always help maximize your panel’s photovoltaic (PV) production no matter where you live. So if you need or want to clean your solar panels, here are the smartest and most efficient ways to get your panels washed off and producing the maximum amount of energy possible.

Just like washing your car, you can DIY solar panel upkeep, but there are also professional solar panel cleaners to make it easier. For a small fee, your original solar installer may even do it for you. If you have a rooftop system, enlisting a cleaning service might be a good idea, if only for safety precautions, as professionals will have more experience using high ladders to reach your roof, for example.

A professional solar panel cleaning company may not necessarily do a significantly better job than you can, but they’re likely better equipped to clean and maintain rooftop units safely and already have all of the necessary equipment. Plus, professional solar panel cleaning will usually only cost you around $150-$300, or $15-$30 per panel.

Professional cleaning may not be worth the cost for ground mount units, because you can safely and effectively clean your panels with a water hose, some dish soap, and a soft rag without having to climb onto your roof.

Types of professional cleaning

Various types of professional cleaning companies can help you. For example, robotics companies use semi-autonomous machines to clean without as much direct personal work involved. Some maintenance companies also use soapless brushes and sponges to clean panels to avoid potentially harmful residues. Other high-tech cleaning processes are currently being developed, including waterless vibration and nanoparticle coatings.

Does your solar lease cover panel maintenance?

Solar lease agreements will often include a maintenance clause, but keep in mind that it can sometimes be hard to wrangle the company to come perform any maintenance once they’ve installed your system.

If you own your solar panels, some companies will perform regular maintenance on their panels, including washing services, while others will repair damages the customer reports. You’ll need to read the print of your agreement to figure out whether cleaning services are included. It’s important to remember that solar panels generally require little maintenance, and spraying them down with a hose occasionally can usually take care of most of the dust and debris.

Here’s our EnergySage step-by-step guide on the best ways to clean your solar panels:

Shut off your solar panel system – this ensures your safety and that your equipment won’t get damaged.

Use a soft brush to clean the surface of your dirty solar panels to remove debris like dirt and dust. Never use a rough or coarse brush as it could damage your panels.

When cleaning your panels with water, use a standard garden hose and soapy water. You don’t need to purchase any particular cleaning solution to clean your panels; regular dish soap will work perfectly. Avoid any strong cleaning agents like bleach that could damage your panels. You should also avoid using any type of high-pressure hose that you might use for things like power washing your house, as they can create cracks or otherwise damage your system.

Use lukewarm water when cleaning your panels as very hot or cold water could also damage your panels.

After you’ve finished the cleaning process, check your panels’ energy output so you can see how much more efficient they are after cleaning.

What should you use to clean your solar panels?

When cleaning your solar panels, the most important consideration to remember is that scratching or damaging the glass in any way will reduce a panel’s energy production – much more than any removable soot or dust build up will. The smartest way to clean your solar panels is to approach the process the same way you would clean your car. Dish soap and clean water applied with a soft sponge or cloth is the safest and easiest cleaning method. It may also be helpful to use a squeegee to remove dirty water. Remember: Avoid damaging or scratching the glass at all costs.

On rare occasions, oily stains can appear on your panels. You might find these if you live near a common truck route or an airport, and they can be tackled with a bit of isopropyl alcohol and a rag. You may be tempted to use strong cleaning detergents like bleach as a fix, but they can leave streaks, damage the glass, and impact the efficiency of the panel, so avoid using them.

How often should you clean your solar panels?

You should clean your solar panels about every six months. Of course, the frequency of solar panel cleaning depends primarily on where you live. For example, if you live somewhere where it rains a lot, you may need to clean your panels less often than if you live somewhere dry and dusty where debris builds up more quickly.

In desert climates, including the U.S. Southwest, more regular cleaning is needed due to the large amount of dust and sand that can affect a solar energy system’s output.

Areas near highways, factories, and airports tend to be more polluted, so solar panels should be cleaned more frequently to avoid residue buildup from pollutants that could result from heavy traffic and machinery nearby.

Solar panels should be frequently cleaned in heavily wooded areas to prevent obstructions like overgrown vegetation and bird droppings.

Should you remove snow from your solar panels?

In the winter, snow on solar panels generally doesn’t need to be removed – it will typically slide off on its own. Most panel installations are tilted at an angle, and snow will naturally slide off as it melts. If snow persists on your panels, you can invest in tools like a solar panel snow rake, which makes it easy for homeowners to remove snow covering on solar panels safely.

But it’s important to keep in mind that you shouldn’t use a standard broom, shovel, or any other non-specialized tool to remove snow from panels; they can scratch the panel glass which will lower your solar power production.

Keeping Current Matters | Mar 4, 2025

More people are taking steps to buy a home. And, if you’ve been waiting for the right time to move, this may be the sign you’ve been looking for.

For the past few years, a lot of would-be homebuyers hit pause on their plans. With rising mortgage rates and affordability challenges, buying just didn’t seem doable. But now, more of them are getting back out there. That’s because they’re getting used to the fact that this may be the new normal for the market – especially as forecasts show mortgage rates may be starting to stabilize. According to the National Association of Realtors (NAR):

“Home buyers seem to be getting over the shock of mortgage rates in the mid- to upper-6% range.”

And that’s good for you and your plans to sell. While there isn’t going to be a big rush of buyers flooding the market all at once, this does mean motivated buyers are re-starting their searches. And here’s the data to prove it.

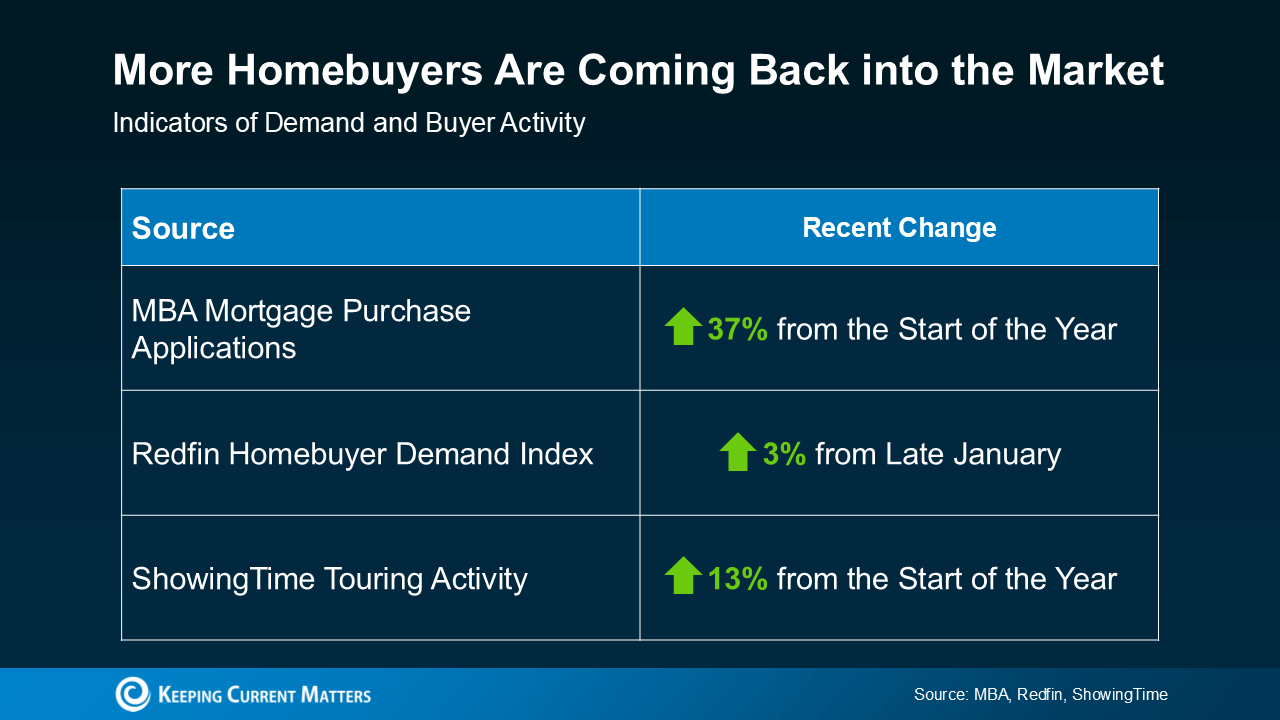

3 Signs Buyers Are Ready To Make Their Move

1. Mortgage Applications Are on the Rise: According to the Mortgage Bankers Association (MBA), mortgage applications are up 37% since the start of the year. That’s a big jump and a clear sign more buyers are more active lately. Don’t miss out on that. Serious buyers who are getting their finances in order are great potential buyers for your house.

2. Buyer Demand Is Picking Up: The Homebuyer Demand Index from Redfin shows demand is up 3% since late January. While that’s not a huge spike, momentum is building.

3. More Home Showings:ShowingTimedata says home showings are up 13% since the beginning of the year. This added foot traffic is exactly what you want to see if you’re about to sell your house. It signals more serious interest in buying. More buyers out there looking means more potential eyes on your house. And more eyes could translate to more offers.

And chances are, this activity is only going to pick up from here. We’re headed into the busiest season of the year for housing. Spring is when more people choose to buy or sell than any other time of year. So, now is a great time to list and get in on the action.

Bottom Line

As buyers re-enter the market, you have the chance to do the same thing. And the increase in buyer activity is definitely something you’ll want to take advantage of. To make sure your house gets in front of these motivated buyers, connect with a local agent.

If the right buyer walked through your door tomorrow, would you be ready to sell?

Let’s connect and plan your next steps. Find out if we’re the right real estate team for you!

For the past few years, it’s been mostly a seller’s market. But dynamics are shifting as the number of homes for sale grows. And that means that the market is balancing out a bit. As a result, some sellers are finding they need to be more flexible to close a deal. One strategy that can help? Offering concessions.

As the National Association of Realtors (NAR) explains:

“As home inventory begins to grow and buyers regain some advantage in the market, sellers may consider offering more in negotiations to make the deal more attractive and get to the closing table.”

What Are Seller Concessions?

Concessions are homebuying costs that a seller agrees to cover as a way to get their house sold. And based on data from the National Association of Realtors (NAR), nearly 1 out of every 4 sellers (24%) offered a concession in 2024. Here are a few of the most common types of concessions:

Covering Closing Costs: The seller pays for part (or all) of the buyer’s closing costs, like appraisal fees, title insurance, or loan fees.

Price Adjustments: Instead of making repairs, a seller might lower the purchase price to make up for updates the buyer will need to tackle.

Adding a Home Warranty: A seller may throw in a home warranty, giving the buyer peace of mind key repairs will be covered in the first year.

And don’t worry. This doesn’t mean you have to come up with more cash to make it happen. These are things that get subtracted from your profits at closing – not more funds you have to bring to the table. And not all concessions are about money.

There are other extras you could throw in. Like, if your buyer is coming from an apartment and has never had a yard before, they may ask if you’d be willing to leave your lawn mower behind. That’s another lever you could pull to keep them happy.

How Concessions Help Sellers

Offering concessions can be a smart strategy for sellers to get a deal done.As Dennis Shirshikov, Professor of Finance and Economics, City University of New York/Queens College told The Mortgage Reports:

“Pricing homes realistically and being willing to offer concessions, such as covering a portion of closing costs or including upgrades, will be key to closing deals . . . in a less frenzied market.”

For example, let’s say you accepted an offer from a buyer, but after their inspection, you found out there are some repairs they want you to tackle before you hand over the keys.

Rather than starting at square one and searching for a new buyer, you could offer a concession. One option is you can take on the repairs and cover the costs yourself. But, if you really don’t want the hassle of dealing with contractors, you could reduce your price by however much repairs would cost. Alternatively, you could offer to pay a portion of your buyer’s closing expenses with the idea they’d use the money they saved at closing toward doing the repairs themselves.

Either way, a concession can be a great way to meet in the middle. However, it’s important to have an agent on your side to help with these negotiations.

A good real estate agent can help you decide when and how to offer concessions, so you don’t give away too much while still ensuring your house gets sold. It’s all about finding the right balance.

Bottom Line

With the market becoming more balanced, seller concessions are coming back into play in some areas. The key is having an agent to help guide you through the process, so things work out in your favor.

What’s a concession you’d consider to move things along?

Let’s connect and plan your next steps. Find out if we’re the right real estate team for you!

These maintenance steps will prevent most refrigerator breakdowns.

1/8

Family Handyman

Clean the Refrigerator Condenser Coils

Cleaning the condensor coils is a very common refrigerator repair. Condenser coils are located on the back of the fridge or across the bottom. These coils cool and condense the refrigerant. When the coils are clogged with dirt and dust, they can’t efficiently release heat. The result is your compressor works harder and longer than it was designed to, using more energy and shortening the life of your fridge.

Clean the coils with a coil cleaning brush and vacuum. A coil cleaning brush does a thorough job and will easily pay for itself. The refrigerator coil brush is bendable to fit in tight areas. They can be used for cleaning your dehumidifier and air conditioner coils too.

You can eliminate more than 70 percent of refrigerator repair and service calls with this simple cleaning step.Do it twice a year or more often if you have shedding pets. Their fur clogs up the coils fast.

Unsnap the grille at the bottom of the refrigerator to access the coils. If your coils are located on the back, you’ll have to roll the fridge out to get at them.

Clean the coils with a special refrigerator coil cleaning brush to loosen the dirt and dust. Vacuum the coils as you brush. Be careful not to bend the fan blades. A gentle brushing will do the job.

Some refrigerators have the coils on the back of the unit. Brush and vacuum these coils in the same manner as coils found under a refrigerator.

CAUTION:

Always unplug your fridge before working on it!

2/8

Family Handyman

Clean the Refrigerator Condenser Fan

If the coils are located on the bottom of the fridge like ours, clean the condenser fan and the area around it. Fridges with coils on the back don’t have a fan. The fan circulates air across the coils to help cool them. At times, paper, dirt, dust and even mice can get sucked into the fan and bring it to a complete stop.

Yours could be in a different area, but it’s always next to the compressor. Most refrigerators will have a diagram on the back or folded up under the front grille showing the location of the major parts. While you’re under there, wipe out the drip pan, a flat pan that collects water from the defrost cycle and allows it to evaporate.

Remove the lower back cover

Access the condenser fan by rolling the fridge away from the wall and removing the lower back cover with a screwdriver. Replace the cover when you’re finished. It’s essential for good air circulation.

Brush and vacuum the fan

Clean the fan blades with the brush and vacuum so air can move freely across them. Also clean the shaft by vacuuming the crease where the blade meets the motor. Don’t lubricate the shaft; oil will attract dirt and cause problems.

3/8

Wipe Down the Refrigerator Door Gasket

Prevent an expensive refrigerator gasket repair bill and cut down air leaks by keeping your door gasket clean. Syrup, jelly or any other sticky stuff dripping down the front sides of your refrigerator can dry and glue the gasket to the frame. The next time you open the door, your gasket can tear. Keep it clean and you’ll get a nice, tight seal, keeping the cool air where it belongs, in the fridge.

To prevent wear, lubricate the door handle side of the gasket by sprinkling baby powder on a cloth and wiping it down once a month.

Clean the door gasket

Wipe the door gasket regularly with warm water and a sponge. Don’t use detergent—it can damage the gasket.

4/8

Clear the Freezer Vents

These little vents on frost-free fridges allow air to circulate in the freezer. Don’t block them or let crumbs or twist ties get sucked in around the evaporator fan or clog the drain tube. To help save energy, keep your freezer about three-quarters full to retain cold air. But don’t pack it any fuller because the air needs to circulate.

Keep the freezer vents unobstructed

Clear food packages away from the vent openings and clean the air return so crumbs and twist ties don’t clog them.

5/8

Set the Fridge Temperature Controls to the Middle Settings

This step won’t necessarily prevent a refrigerator repair, but it’ll extend the life of your fridge by allowing it to run more efficiently, which reduces your electric bill. Your fridge has at least two temperature controls (except on manual defrost types, which have one).

The one for the food compartment is a thermostat that turns the compressor on and off. The second, for the freezer, is just an air baffle. The baffle lets cold air from the freezer sink into the food compartment. Closing the baffle makes the freezer colder.

Adjust the temperature controls

Set the temperature controls to the middle settings. Make any adjustments according to a refrigerator thermometer. The optimum setting for your fridge is between 38 and 42 degrees F; the freezer, between 0 and 10 degrees.

6/8

Claire Krieger/Family Handyman

Three Ways to Get the Smell Out

Charcoal briquettes absorb the odor just like a filter in a range hood.

Crumpled newspaper. The ink absorbs the odor.

Baking soda is the old standby. Leave an open box in the fridge and replace it every three months for continuous deodorizing.

7/8

Family Handyman

Clear and Clean the Drip Openings

Drip openings allow water that has melted from the defrost cycle to flow down to a pan located by the compressor, where it evaporates. Check your owner’s manual for the location on your fridge. On cycle-defrost fridges, a channel directs the water to a tube in the food compartment.

On frost-free refrigerators, look for a small cap under the crisper drawers that covers a hole, or an opening in the back of the freezer or refrigerator. If the drain opening clogs, water will build up under the crisper drawers and eventually leak out onto the floor.

Locate the drip cup

Find the drip opening on your fridge.

Close up of the drip tube opening

Locate the drip opening and wipe it out, being careful not to press any debris down into the hole. Suck out crumbs with a vacuum.

8/8

Troubleshooting Refrigerator Repair

Service specialists will be the first to admit: A ton of their callers don’t require refrigerator repair service at all. The solutions are so easy they don’t even require a toolbox. Before you pick up the phone, check the following list. It just might save you money and a bit of embarrassment.

Got power?

Check the circuit breaker or fuse box to be sure power’s coming to the outlet.

Is the cord plugged in tight? Wiggle it around a little. A worn receptacle could let the plug fall out just enough for the connection to fail.

Plug a light or any other electrical device into the outlet to see if it works. If it doesn’t, you’ve got an electrical problem, not a refrigerator problem.

Check for a loose, worn or frayed power cord. Rodents often chew through a wire. Sometimes cords loosen when the fridge is moved.

What if you have power but poor cooling?

Make sure the thermostat is turned on and set right. On some models the dial is easily bumped, shutting the fridge down. Or kids could have messed with it.

Your fridge is running all the time but the food’s still warm.

Vacuum the coils. Dirty coils can eventually cause the overload protector on the compressor to shut the fridge down. It’ll automatically come back on when the compressor cools, but by then your food is usually warm.

Is the condenser fan jammed? (This applies only to fridges with the coils on the bottom.) Remove any obstacles and clean it thoroughly. Unplug the fridge and turn it a few times and see if it comes on. If it’s still not working, you’ll have to replace it.

Is the light turning off when the door’s closed? That little light bulb can raise the temperature in the fridge substantially. To check it, close the door and use a butter knife to pull the gasket slightly away from the frame. If light shines out, the switch is bad or slightly out of alignment. Until you fix the switch, loosen the light bulb so it goes out.

Look for ice buildup (frost-free fridges only) bulging on the inside walls or the floor of the freezer. Manually defrost the freezer by unplugging it. It’s only a temporary fix, so call for service.

Hiking in Orange County is popular among locals and visitors. Orange County trails range from easy to difficult and trying to figure out the best one fit for you and your dog can be a challenge. Here are some dog friendly hikes in Orange County to help you decide which is best for your next adventure. As in all hikes watch out for local animals, snakes, coyotes, and the occasional mountain lion. Take a look at these hikes to get you started. Don’t forget to pack some water for your and your fur friend and take care to preserve the OC trails on your hike. Enjoy!

Aliso Summit Trail

Length: 4 Miles Roundtrip

Location: Laguna Niguel. Hiking Trails that run along the Southern ridge of Wood Canyon and Aliso regional parks.

Condition: Unpaved

Highlights Ocean View in the middle of the trail

Dogs must be leashed

Parking: Free on Residential Streets

Level: Moderate

Las Ramblas Trail

Length: 6.3 Mile Loop

Location: San Juan Capistrano

Condition: Unpaved

Highlights: Mountain and costal views. Multiple trails. This trail is one of the most popular hiking trails during the Spring Super Bloom.

Dogs must be leashed

Parking: Free Parking in surrounding areas. Depending on if its open it has a parking lot close by.

Level: Moderate/Difficult

Notes: Look out for Mountain Bikers and Steep hills. The trail can get really muddy.

Ridgeline Trail

Length: 5.7 Miles Out and Back

Location: San Clemente

Condition: Partially Paved

Highlights: Beautiful views

Dogs must be leashed

Parking: Free on Residential Streets

Level: Moderate/Difficult hike

Black Star Canyon

Length: 6.7 Miles Out and Back

Location: Silverado Canyon

Condition: Partially Paved

Highlights: Great views, waterfall

Dogs must be leashed and are allowed off leash in some areas

Parking: Adventure Pass required, gets packed. Go early.

Buyers: This means you have more choices, and you can be more selective.

Buyers: This means you have more choices, and you can be more selective. Buyers: Acting sooner rather than later could be a smart move before your competition heats up even more.

Buyers: Acting sooner rather than later could be a smart move before your competition heats up even more.