This event is one of the best of its kind with a focus on STEAM education. For one weekend only participate in activities, watch demonstrations and let the kids immerse themselves in the wonderful world of STEAM

Race On The Base, Sat, Apr 13 @raceonthebase

The ever-popular UWS Race on the Base Reverse Sprint Triathlon and 5K Walk/Run is here!

GardenFest Sat, Apr 13

San Clemente’s Biggest, Best Plant Sale and Garden/Household Goods Flea Market. Waterwise Plants, California Native Plants, Succulents, Cactus, Perennials, Annuals, Herbs, as well as an assortment of other types of plants. 8am-2pm at the San Clemente Community Center.

Sake Festival, Sun, Apr 14 @gokumius

More than 40 craft sakes available for tasting and izakaya style appetizer buffets at Gokumi Ramen & Yakitori with 2 time frames available. 1-3pm or 5-8pm. Tickets are $50/ Each. Must be 21+ to attend.

Paws In The Park, Sat, Apr 13

There will be plenty to bark about at this event featuring pet-related vendors, rescue groups, DJ and games, crafts, activities and more. 10am-12:30pm On The Town Green In Ladera Ranch.

Springtime in Paris Boutique, Sat, Apr 13

Immerse yourself in the allure of Parisian charm as you peruse hand-sculpted treasures crafted by our talented local artisans and crafters. Featuring over 50+ vendors, our boutique offers an array of quirky and irresistible gifts. 8am-4pm at the Norman P Murray Community Center in Mission Viejo

Are you thinking about making a move? If so, now may be the perfect time to start the process. That’s because experts say the best week to list your house is just around the corner.

A recent Realtor.comstudy looked at housing market trends over the past several years (with the exception of 2020, since it was an unusual year), and found the best week to put your house on the market this year is April 14-20:

“Every year, one week stands out from the rest as that perfect stretch of time when it’s great to be a home seller. This year, the week of April 14–20 is the best time to sell—that is, if sellers want to see lots of interest in their homes, sell quickly, and pocket some extra cash, according to Realtor.com® data.”

Here’s why this matters for you. While the spring market is a great time to sell no matter the week, this may be the peak sweet spot. And if you’ve been putting your plans on the back burner and waiting for the right time to act, this could be the nudge you need to make your move happen. As Hannah Jones, Senior Economic Research Analyst at Realtor.comexplains:

“The third week of April brings the best combination of housing market factors for sellers. The best week offers higher buyer demand, lower competition [from other sellers], and fewer price reductions than the typical week of the year.”

But, if you want to get in on the action, you’ll need to move quickly and lean on the pros. Your local real estate agent is the perfect go-to when it comes to figuring out a plan to prep your house and get it on the market.

They’ll be able to offer advice to balance your target listing date with what you need to do from a repair and renovation standpoint. And they can walk you through exactly how to prioritize your list so you know what to tackle first.

For example, if your house is already in good shape, you’ll be able to really focus in on the smaller things that are easy to do and make a big impact. As an article from Investopediasays:

“You won’t have time for any major renovations, so focus on quick repairs to address things that could deter potential buyers.”

Here are some specific examples from that article:

Just remember, even if you’re not ready to list within the next couple of weeks, that’s okay. The window of opportunity doesn’t close when this week ends. Spring is the peak homebuying season and it’s still a seller’s market, so you’ll be in the driver’s seat all season long.

Bottom Line

Ready to get the ball rolling? Connect with a real estate agent to schedule a time to go over your next steps.

Buying a home this spring? You’re probably navigating today’s affordability challenges and dealing with the limited number of homes for sale. But, what if there was a solution that could help with both?

If you’re having a hard time finding a home you love, and mortgage rates are putting pressure on your budget, it may be time to look at newly built homes. Here’s why.

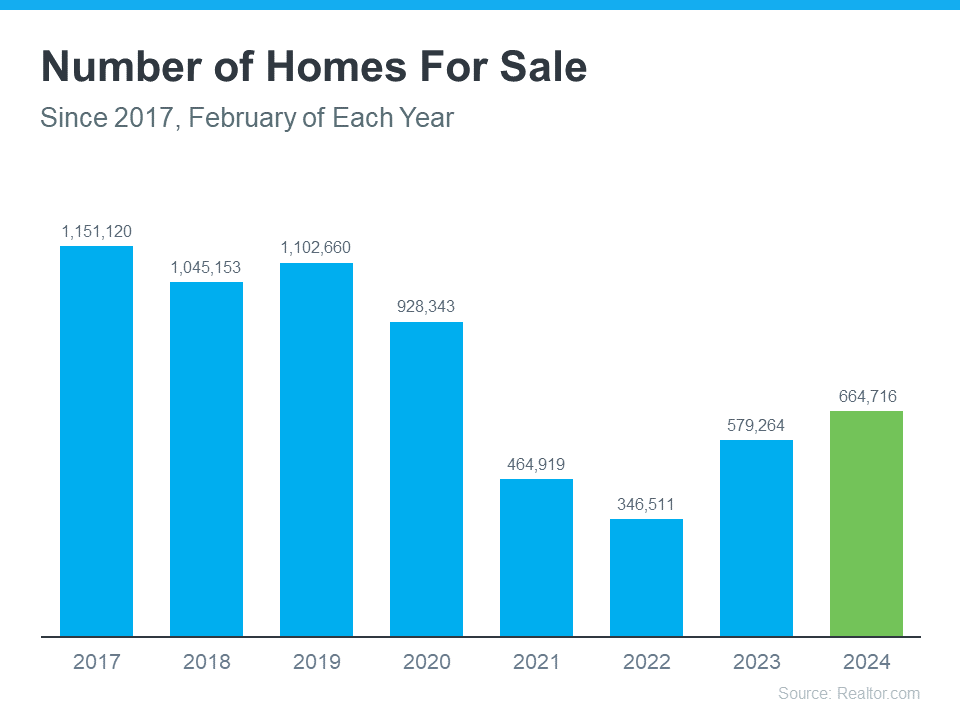

New Home Construction Is an Inventory Bright Spot

When looking for a home, you can choose between existing homes (those that are already built and previously owned) and newly constructed ones. While the number of existing homes for sale has increased this year, there are still fewer available than there were in more typical years in the housing market, like back in 2018 or 2019.

So, if you’re looking to expand your pool of options even more, turning to newly built homes can help. As Danielle Hale, Chief Economist at Realtor.com, explains:

“The shortage of existing homes For Sale has opened up the possibility of new-home construction to more buyers who may not have once considered it.”

And the good news is, there are more newly built homes to pick from right now. The graphs below use data from the Census to show how new home construction is ramping up in two key areas (see most recent spike in green):

Starts, or homes where builders just broke ground, have seen a big increase lately. And completions, homes that builders just finished, are also up significantly. So, if you want a new, move-in ready home or you want to get in early and customize your build along the way, you have more options right now.

Builders Are Offering Incentives To Help with Affordability

And to sweeten the pot, builders are offering things like mortgage rate buy-downs and other perks for homebuyers right now. This can help offset today’s affordability challenges while also getting you into your dream home. Mark Fleming, Chief Economist at First American,explains why you may find builders have more wiggle room to offer more for you than the typical homeowner:

“Builders aren’t rate locked-in. They would love to sell you the home because they’re not living in it. It costs money not to sell the home. And many of the public home builders have said in their earnings calls that they are not going to be pulling back on incentives, especially the mortgage rate buydown, so that will help the new-home market continue to perform well in the spring home-buying season.”

An article from HousingWire also says this about what builders are offering right now:

“. . . the use of sales incentives still shows some momentum as 60% of respondents reported using them, up from 58% in February. “

Just remember, buying from a builder is different from buying from a home seller, so it’s important to partner with a local real estate agent. Builder contracts can be complex. A trusted agent will be your advocate throughout the process.

They’ll be your go-to resource for advice on construction quality and builder reputation, reviewing and negotiating contracts to get you the best deal, helping you decide on which customizations and upgrades are most worthwhile, and a whole lot more.

Bottom Line

If you’re struggling to find a home to buy, or with today’s affordability challenges, connect with CA Real Estate Group to see if newly built homes could be the solution you’re looking for.

This report specifically benefits our Single Women Home Buyers to provide insight into the demographics, financial profiles, home buying motivations & lending experiences of women who purchase homes on their own.

We’d be happy to walk through this report with you.

Let’s connect and plan your next steps and find out if we’re the right real estate team for you!

While it may be easy to track down smells coming from your garbage can or garbage disposal, other smells require a keener nose.

In order to help you find all of the bad smells in your home, here are some common smells and where you can find the source:

Rotten Eggs

The smell of sulfur or rotten eggs is never a good sign. You either have some old eggs sitting around from a couple Easters ago, or you have a serious gas leak or electrical problem.

The two most common sources for rotten egg smell in the home are electrical components (inside of outlets for example) or a natural gas leak.

Natural gas manufacturers are required to add a chemical, called mercaptan, to their gas in order to make it easier to detect a leak. Without this additive, you wouldn’t be able to see, smell, or taste natural gas (much like carbon monoxide).

If you smell rotten eggs in the home, call the gas company to make sure you don’t have a gas leak.

If there is no gas leak in the home, you may have a problem with your electrical system. If you smell the rotten egg smell near an outlet, that’s probably where it is coming from. When the plastic components behind your outlet plate burn, it can smell like rotten eggs. This smell indicates that there is a dangerous arcing situation happening within the interior of your outlet that could cause a home fire.

We recommend turning off power at the circuit breaker to cut off electricity to the room with the smelling outlet.

One other possible cause of a rotten egg smell in your home is when you run the hot water. You may experience a rotten egg smell when the hot water is running due to an old anode rod.

Anode rods in hot water heaters should be replaced every 5 years or so. Replacing your anode rod will reduce corrosion in your water heater and may even be able to double its lifespan.

Call your local plumber to find out which kind of anode you should replace your old one with.

Sewage Smell

If you smell raw sewage in your home, you may have a dried out P-trap. The P-trap is the little curved section of piping that helps create a seal from the sewer gas that lurks behind it. The only problem is that the curved “P” section needs to be filled with water in order to create the necessary blockage.

If you haven’t used one or more of your sinks in a while the water that normally creates a seal in the “P” section has evaporated and dried out.

In order to prevent sewer gases from rising up through your pipes and into your home, it’s important to run water in all of your drains periodically. If you have a sink in your garage or another part of the home that rarely gets use, make sure you run the water in those sinks at least once a month to refresh the water in the P-trap.

If running water in your sinks doesn’t solve the problems, you may have a more serious plumbing problem. Speak with a professional plumber to discuss your options.

Fish Smell

Something smells fishy… and it’s not fish. Well, likely not. If you smell fish with no fish in sight, you could have an overheating electrical component somewhere.

Sometimes, burning plastic, wiring, and other electrical components smell like rotten eggs or sulfur to some people. Other people notice a distinctive fishy smell. Whether you get a whiff of fish or rotten eggs, it’s important to investigate the situation. You may have a dangerous arcing situation behind one of your outlets or switches that can cause a house fire.

Again, if you can locate the electrical source of the smell and It seems to be coming from one of your outlets or switches, turn off power at the breaker box and call an electrician right away!

Stale Air

If you frequently pick up a stale smell in your home, it may be because of air leaks around the home. Recessed lights that are often connected to the attic are notoriously leaky. If you notice the stale air smell around any of your recessed lights, you will have to go into the attic to seal the air leak.

Read our Attic Insulation Guide for tips on sealing your recessed lights, flue, and other common leaky areas in your attic.

If you detect any of these odors in your home, make sure it isn’t a serious electrical or natural gas problem. Sulfur, “rotten egg” smells are a big warning sign. For help dealing with odors in your home, contact experts in plumbing, heating, cooling and/or electrical.

CA Real Estate Group works with trusted experts in all fields. Contact one of our agents for a referral anytime!

Daily beginning March 11, 2024: Mon-Fri at 9:30am, 11am, 1pm, & 2:30pm | Sat & Sun every 30 minutes between 9:30am and 2:30pm

Tanaka Farms is famous for their delicious, sweet, and juicy strawberries! Take a wagon ride around the farm. Learn about the farming methods and history of the farm from your friendly tour guide. You will see how fruits and vegetables grow! Make one stop to pick a seasonal vegetable*, and then the last stop on this tour is in the strawberry patch where you can pick and eat strawberries! Everyone will take home a one-pound basket of strawberries! After the tour, visit the Barnyard Educational Exhibit where you can meet and interact with their barnyard friends.

Debt-to-income ratio shows how your debt stacks up against your income. Lenders use DTI to assess your ability to repay a loan.

Nerdy takeaways

Debt-to-income ratio represents the percentage of your monthly income that goes to debt payments.

Lenders use DTI — along with credit history and other factors — to evaluate if a borrower can repay a loan.

Lenders have different DTI requirements. Personal loan companies may allow higher DTIs than mortgage lenders.

Debt-to-income ratio divides your total monthly debt payments by your gross monthly income, giving you a percentage. Here’s what to know about DTI and how to calculate it.

How to calculate your debt-to-income ratio

To manually calculate DTI, divide your total monthly debt payments by your monthly income before taxes and deductions are taken out. Multiply that number by 100 to get your DTI expressed as a percentage.

Here’s an example: A borrower with rent of $1,200, a car payment of $400, a minimum credit card payment of $200, and a gross monthly income of $6,000 has a debt-to-income ratio of 30%. In this example, $1,800 is the sum of all debt payments. When you divide $1,800 by $6,000 and then multiply that answer by 100, you get 30.

To get the most accurate DTI ratio, make sure to include all your debt payments and income sources.

Debt payments can include:

Rent or mortgage payments.

Auto loan payments.

Student loan payments.

Minimum credit card payments.

Personal loan payments.

Other debt payments, such as the minimum payment on a home equity line of credit.

Child support, alimony, or other court-ordered payments.

Don’t include other monthly expenses, such as:

Groceries.

Gas.

Utility payments.

Phone bills.

Health insurance.

Auto insurance.

Child care payments.

Recreational spending.

Include all sources of income, such as:

Salary from full-time work.

Part-time wages.

Freelance income.

Bonuses.

Child support or alimony received.

Social security benefits.

Rental property income.

How lenders view your DTI ratio

Lenders look at debt-to-income ratios because research shows borrowers with high DTIs have more trouble making consistent payments.

Each lender sets its own DTI requirement, but not all creditors publish them. Generally, a personal loan can have a higher allowable maximum DTI than a mortgage.

You may find personal loan companies willing to lend money to consumers with debt-to-income ratios of 50% or more, and some exclude mortgage debt from the DTI calculation. That’s because one of the most common uses of personal loans is to consolidate credit card debt, which can help you pay off debt faster and lower your DTI.

Does your DTI affect your credit score?

Your debt-to-income ratio does not affect your credit scores; credit-reporting agencies may know your income, but they don’t include it in their calculations.

Credit utilization, or the amount of credit you’re using compared with your credit limits, does affect your credit scores. Credit reporting agencies know your available credit limits, both on individual loan accounts and in total. Most experts advise keeping the balances on your cards no higher than 30% of your credit limit, and lower is better.

How to understand DTI ratio

DTI can help you determine how to handle your debt and whether you have too much debt.

Here’s a general breakdown:

DTI is less than 36%: Your debt is likely manageable, relative to your income. You shouldn’t have trouble accessing new lines of credit.

DTI is 36% to 42%: This level of debt could cause lenders concern, and you may have trouble borrowing money. Consider paying down what you owe. You can probably take a do-it-yourself approach; two common methods are debt avalanche and debt snowball.

DTI is 43% to 50%: Paying off this level of debt may be difficult, and some creditors may decline applications for more credit. If you have primarily credit card debt, consider a credit card consolidation loan. You may also want to look into a debt management plan from a nonprofit credit counseling agency. Such agencies typically offer free consultations and will help you understand all of your debt relief options.

DTI is over 50%: Paying down this level of debt will be difficult, and your borrowing options will be limited. Weigh different debt relief options, including bankruptcy, which may be the fastest and least damaging option.

Ways to lower your DTI ratio

Reduce your debt-to-income ratio to improve your chances of qualifying for future credit.

Increase your income. Make more money by selling items online or starting a side gig, even for a short period, like babysitting or dog walking.

Reduce your debt. Paying down your credit card balance can reduce your minimum monthly payments. Your DTI will also go down if you pay off installment loans, like student loans or a car loan.

Refinance or consolidate debt. Refinancing or consolidating debt at a lower interest rate could lower your monthly payments and therefore reduce your DTI. Negotiating a longer repayment term could also lower your monthly debt payments, though you may wind up paying more interest over time.

Avoid taking on additional debt. Try not to add to your credit card balance or take out additional loans if you want to lower your DTI.

Keeping Current Matters | Feb 26, 2024

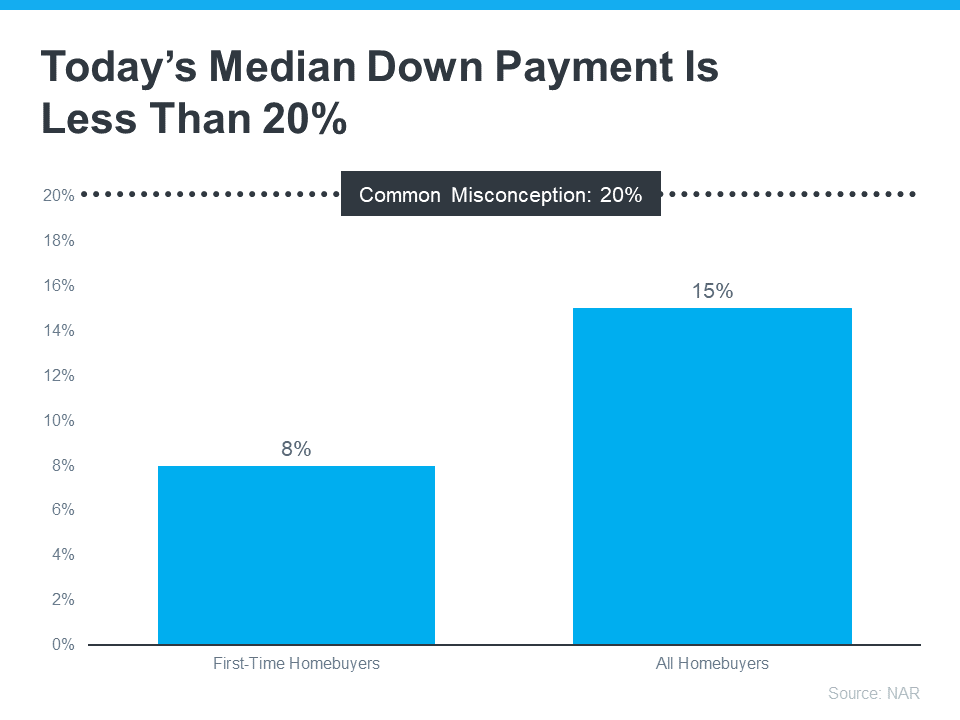

If you’re planning to buy your first home, saving up for all the costs involved can feel daunting, especially when it comes to the down payment. That might be because you’ve heard you need to save 20% of the home’s price to put down. Well, that isn’t necessarily the case.

Unless specified by your loan type or lender, it’s typically not required to put 20% down. That means you could be closer to your homebuying dream than you realize.

“Although putting down 20% to avoid mortgage insurance is wise if affordable, it’s a myth that this is always necessary. In fact, most people opt for a much lower down payment.”

According to the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. In fact, for all homebuyers today it’s only 15%. And it’s even lower for first-time homebuyers at just 8% (see graph below):

The big takeaway? You may not need to save as much as you originally thought.

Learn About Resources That Can Help You Toward Your Goal

According to Down Payment Resource, there are also over 2,000 homebuyer assistance programs in the U.S., and many of them are intended to help with down payments.

Plus, there are loan options that can help too. For example, FHA loans offer down payments as low as 3.5%, while VA and USDA loans have no down payment requirements for qualified applicants.

With so many resources available to help with your down payment, the best way to find what you qualify for is by consulting with your loan officer or broker. They know about local grants and loan programs that may help you out.

Don’t let the misconception that you have to have 20% saved up hold you back. If you’re ready to become a homeowner, lean on the professionals to find resources that can help you make your dreams a reality. If you put your plans on hold until you’ve saved up 20%, it may actually cost you in the long run. According to U.S. Bank:

“. . . there are plenty of reasons why it might not be possible. For some, waiting to save up 20% for a down payment may “cost” too much time. While you’re saving for your down payment and paying rent, the price of your future home may go up.”

Home prices are expected to keep appreciating over the next 5 years – meaning your future home will likely go up in price the longer you wait. If you’re able to use these resources to buy now, that future price growth will help you build equity, rather than cost you more.

Bottom Line

Keep in mind that you don’t always need a 20% down payment to buy a home. If you’re looking to make a move this year, reach out to a trusted real estate professional to start the conversation about your homebuying goals.

A Florida man has become a TikTok star after amassing million of followers who watch his home repair videos.