In today’s fast-paced world, many families opt to enjoy meals around a kitchen table or breakfast bar, often leaving the formal dining room empty and unused. Here are a few ways you can revamp your formal dining room into a fun or functional space.

Make a Work Area

Boost your productivity by designating a separate space that prevents work and homework from overtaking the rest of your home. Furnish the room with a desk, a supportive chair and a small worktable for projects. Be sure to include baskets or other storage bins to organize supplies.

Set Up a Game Room

Score big on family bonding with a game room that brings everyone together in a fun, modern way — much like the dining room table once did. Consider a ping-pong or pool table with an add-on tabletop feature and surround it with comfortable chairs. Include cabinetry to store board games.

Start an Indoor Garden

Show off your green thumb with a variety of plants in their very own garden room. Use colorful planters and vases to bring character to the space, but make sure you place planters on waterproof surfaces.

Build a Library

Line the walls with shelves and fill them with your favorite books. For something unusual, consider creating a music library with your favorite vinyl albums or a small movie room to house your favorite films. Don’t forget to include some plush seating to enjoy your media collection.

Create a Sitting Room

Ditch the TV and create an inviting conversation space with comfortable furnishings arranged to encourage family connection. Add soft lighting and an electric fireplace for added warmth.

Organize a Decor Swap

Transform your space without spending a dime by trading trinkets for newfound treasures at a decor swap.

Plan the Perfect Swap

Send invitations to friends and family. Include instructions detailing how many pieces to bring, what items are acceptable and what to leave at home. You might even try a themed swap, like “seasonal splendor” or “vintage vibes.”

Host With Style

Create an inviting atmosphere with light background music and refreshments. Arrange tables to display the featured pieces and allow everyone to browse, then have your guests make selections. Keep the process simple by drawing two or three names at a time and setting a time limit for choosing items. Allow extra time for any additional swapping between guests.

Any unclaimed items remaining after the decor swap is over can be donated to a local nonprofit or posted online in a Buy Nothing group.

Lighting Hacks

Proper lighting can make or break a room’s look and feel. Every room is different, so it’s important to tailor lighting to the function of the space.

Soft lighting works well in rooms where you want to relax, such as bedrooms and living rooms. Skip the overhead lights and opt for table lamps or wall sconces to create a sense of coziness.

Practical lighting is essential in areas where you want to be productive, such as an office or workout room. In these spaces, the right overhead lighting and functional fixtures can add brightness and boost productivity.

Versatile lighting is key in the areas of your home where you can be both productive and relaxed, such as the kitchen or primary bedroom suite. Install dimmer switches for overhead lighting to adjust the mood as needed. Add lamps or battery-operated LED candles to create a warm, inviting atmosphere during relaxation time, and consider under-cabinet lighting for practical tasks. Layering your lighting options allows you to easily transition the space from bright and functional to soft and soothing.

The Dirty Truth About Kitchen Towels

Keeping your kitchen sparkling clean isn’t just about scrubbing surfaces and washing fruits and veggies. One often overlooked culprit for bacteria buildup is the kitchen towel.

While cloth towels are an economical and environmentally friendly alternative to paper, they’re breeding grounds for bacteria. Even after rinsing towels in the sink, salmonella can still grow quickly overnight. Towels used to wipe down counters and clean up spills should be laundered in a washing machine with hot water after one day’s use. If towels are used only to dry hands, they should be laundered after three or four days. Experts also recommend replacing kitchen towels every year or two.

Recipe: Penne With Smoked Sausage

Ingredients

1 Tbsp. olive oil

1 lb. smoked sausage

½ cup diced onion

1 Tbsp. minced garlic

½ tsp. salt

½ tsp. pepper

2 cups chicken broth

1 (10 oz.) can diced tomatoes

½ cup milk

2 cups dry penne pasta

Crushed red pepper

Shredded Parmesan cheese

Basil leaves

Arugula leaves

Directions

Heat olive oil in a large pan over medium heat. Slice sausage into bite-sized pieces. Brown sausage and onion in olive oil. Add garlic, salt and pepper. Continue cooking for about 30 seconds.

Add chicken broth, tomatoes, milk, and dry pasta to the pan and bring to a boil. Reduce heat to low and cover. Simmer for 15 minutes. Remove from heat and top with crushed red pepper and Parmesan cheese. Garnish with basil and arugula leaves.

August 17, 2024 marks a seismic shift in the real estate industry.

It’s a day that will reshape how buyers and sellers interact, and most importantly, it will redefine the relationship between buyers and their agents.

For those of us who have been in real estate for decades, this change feels almost revolutionary. But the seeds of this transformation were planted back in the 1990s when buyers first began advocating for buyer’s agents to be true fiduciaries, safeguarding their interests above all else. This movement was driven by a desire for transparency, accountability, and a partnership that ensured buyers were fully represented in one of the most significant financial decisions of their lives.

The Shift in Commissions

Traditionally, buyer agents were compensated through the MLS, with commissions often baked into the sale price of a home. Come August 17th, however, this practice will no longer be the default. Commissions for buyer agents will be removed from the MLS, meaning buyers and agents alike will be in the dark about whether compensation is available. This is a significant departure from the status quo, where both parties had clear expectations going into a transaction.

New Requirements for Buyers

Another key change is the introduction of mandatory signed agreements before buyers can even tour a property privately with an agent. These agreements come in various forms:

Exclusive Buyer Agency Contract: A commitment that binds the buyer to an agent for a specified period, often requiring compensation upfront for their services.

Single Property Tour Form: A more flexible agreement for buyers who want to tour a specific property without long-term commitment.

Non-Exclusive Buyer Agency Contract: Ideal for investors, this agreement allows buyers to work with multiple agents simultaneously, offering flexibility in their search.

The introduction of these forms signals a new era where the choice of representation matters more than ever. Buyers must be more strategic in selecting their agents, ensuring they align with their needs and goals.

Historical Context: The Evolution of Buyer Representation

In the 1990s, the concept of a buyer’s agent being a fiduciary was a radical idea. Before that, most agents worked primarily for the seller, even if they were showing homes to buyers. The introduction of buyer agency contracts changed the game, giving buyers their own advocates in the transaction process. Today’s changes build on that legacy, pushing the industry toward even greater transparency and fairness.

What Buyers Need to Do Now

As we navigate this new landscape, it’s crucial for buyers to understand their options and the implications of these changes:

Educate Yourself: Understanding the different types of agreements and how they affect your buying power is more important than ever.

Choose Wisely: The agent you work with will significantly impact your experience and outcome. Make sure they are fully informed and able to articulate their value proposition.

Plan Ahead: The days of casually touring homes without a plan are over. Buyers must now be more deliberate in their approach, ensuring they have the right representation in place from the start.

Questions to Consider

Are you prepared for the new requirements in the home-buying process starting August 17th?

How will the removal of buyer agent commissions from the MLS affect your home search strategy?

What should you look for in a buyer’s agent in this new era of real estate?

Conclusion

The real estate market is on the cusp of a significant change, but with the right preparation and understanding, buyers and sellers can navigate these new waters successfully. Who you work with matters more than ever, and having the right representation can make all the difference in achieving your real estate goals. That’s why you can call any of our CA Real Estate Group agents to help you navigate your next real estate purchase or sale.

Is your home looking less exciting these days? Are you sick of staring at the same four walls but don’t have a huge budget for renovations? Just because you don’t have a lot to spend doesn’t mean you can’t refresh your home. You just need to know what to do and how to pay as little as possible for it. Here are seven microbudget ways to upgrade a home.

Repaint Any Room

“Paint is a decorator’s miracle,” says interior designer Kate Dawson. “Nothing can transform a space as quickly or dramatically—without renovating—as a new coat of paint. It can change the vibe and energy even if it’s only used on one wall.”

The best thing about paint is it’s not only inexpensive (the price of dining out for lunch can get you a fairly cheap can of paint)—but you can also do it yourself and save on labor. The cost of rollers and brushes also won’t break the bank.

Swap Out Pillows

Whether they’re in your living room or your bedroom, old pillows can really make a room look dated, but new pillows can surprisingly transform. “I see decorative pillows as the home’s version of earrings, shoes, and scarves,” Dawson says. “When we’re going out, we always accessorize because it adds individuality, style, and pops of color. A room is the same way. Pillows pull the room together and give the space cohesion and a new energy.”

There are many places to buy pillows inexpensively, such as HomeGoods or Target. Amazon also has curated sets, so you don’t have to spend extra time and money mixing and matching. Another way to save a few bucks is to replace the pillow case but keep the insert.

Add Greenery

There isn’t one room that wouldn’t benefit from bringing a little nature in. That’s why Dawson is so passionate about plants. However, real ones can be expensive, so she recommends going the faux route to achieve the same design impact for less money. “Plants are a fantastic way to play with scale, levels, and volume,” the designer says. “They come in so many shapes and sizes and are the perfect thing to tuck into little places that just need a little pop of color, or for large spaces such as a big empty corner of a room. Get a nice faux six-inch fiddle leaf plant for any area that feels like a gap in the flow of the space.”

Wallpaper A Powder Room

We often neglect powder rooms but these spaces are a great way to go big on design. While replacing a toilet and sink can be expensive, installing wallpaper is a great way to get some wow factor without overspending. To save more money, consider peel-and-stick wallpaper over the traditional pasted kind because it can be self-installed and generally costs less.

Swap Out Hardware in the Kitchen and Bathroom

Old hardware can really date a room. While you can definitely splurge on hardware, you don’t need to. Look for hardware multipacks, which can get the cost of a handle or knob down to a few dollars each—a major bang for your buck.

Add A Peel And Stick Backsplash To Your Kitchen

Is your kitchen backsplash looking dated? While you might not have the budget to replace it permanently, you can use peel and stick tile over it. From faux marble subway tiles to ceramic penny styles, there are a lot of options out there. Best of all, no one will know the difference between that and the real thing.

Add Artwork in Any Room

Dawson recommends upgrading your plain walls with artwork. “Adding colorful artwork instantly tells a story about the homeowner,” she says. “It always makes great conversation, and aesthetically, it always adds depth, texture, and dimension to the room.”

Alternatively, you can use photos. Try shopping from your own camera roll for maximum savings. That beautiful shot you have of a sunset on vacation can be made into a canvas fairly inexpensively.

Are you on the fence about whether to sell your house now or hold off? It’s a common dilemma, but here’s a key point to consider: your lifestyle might be the biggest factor in your decision. While financial aspects are important, sometimes the personal motivations for moving are reason enough to make the leap sooner rather than later.

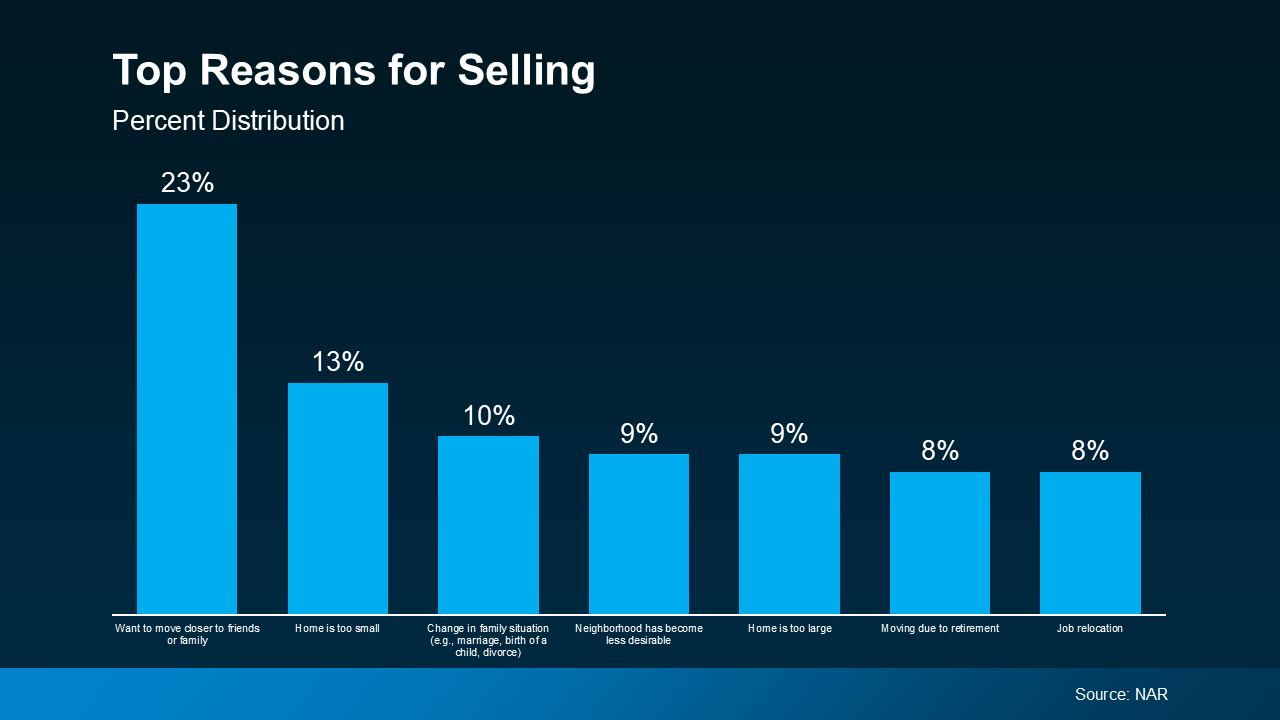

An annual report from the National Association of Realtors (NAR) offers insight into why homeowners like you chose to sell. All of the top reasons are related to life changes. As the graph below highlights:

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

If you, like the homeowners in this report, find yourself needing features, space, or amenities your current home just can’t provide, it may be time to consider talking to a real estate agent about selling your house. Your needs matter. That agent will walk you through your options and what you can expect from today’s market, so you can make a confident decision based on what matters most to you and your loved ones.

Your agent will also be able to help you understand how much equity you have and how it can make moving to meet your changing needs that much easier. As Danielle Hale, Chief Economist at Realtor.com, explains:

“A consideration today’s homeowners should review is what their home equity picture looks like. With the typical home listing price up 40% from just five years ago, many home sellers are sitting on a healthy equity cushion. This means they are likely to walk away from a home sale with proceeds that they can use to offset the amount of borrowing needed for their next home purchase.”

Bottom Line

Your lifestyle needs may be enough to motivate you to make a change. If you want help weighing the pros and cons of selling your house, connect with CA Real Estate Group today.

When you’re thinking about buying a home, your credit score is one of the biggest pieces of the puzzle. Think of it like your financial report card that lenders look at when trying to figure out if you qualify, and which home loan will work best for you. As the Mortgage Report says:

“Good credit scores communicate to lenders that you have a track record for properly managing your debts. For this reason, the higher your score, the better your chances of qualifying for a mortgage.”

The trouble is most buyers overestimate the minimum credit score they need to buy a home. According to a report from Fannie Mae, only 32% of consumers have a good idea of what lenders require. That means nearly 2 out of every 3 people don’t.

So, here’s a general ballpark to give you a rough idea. Experian says:

“The minimum credit score needed to buy a house can range from 500 to 700, but will ultimately depend on the type of mortgage loan you’re applying for and your lender. Most lenders require a minimum credit score of 620 to buy a house with a conventional mortgage.”

Basically, it varies. So, even if your credit isn’t perfect, there are still options out there. FICO explains:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders, and there are many additional factors that lenders may use . . .”

And if your credit score needs a little TLC, don’t worry—Experian says there are some easy steps you can take to give it a boost, including:

1. Pay Your Bills on Time

Lenders want to see that you can reliably pay your bills on time. This includes everything from credit cards to utilities and cell phone bills. Consistent, on-time payments show you’re a responsible borrower.

2. Pay Off Outstanding Debt

Paying down what you owe can help lower your overall debt and make you less of a risk to lenders. Plus, it improves your credit utilization ratio (how much credit you’re using compared to your total limit). A lower ratio means you’re more reliable to lenders.

3. Don’t Apply for Too Much Credit

While it might be tempting to open more credit cards to build your score, it’s best to hold off. Too many new credit applications can lead to hard inquiries on your report, which can temporarily lower your score.

Bottom Line

Your credit score is crucial when buying a home. Even if your score isn’t perfect, there are still pathways to homeownership. Let’s connect if you want to go over your options with an expert.

Let’s connect and plan your next steps. Find out if we’re the right real estate team for you!

For many families, the kitchen is the social hub of the home, so it’s important that you clean often. Some areas of your kitchen will require consistent attention, such as the counters. Others, like larger appliances such as the refrigerator or oven, can be addressed on a weekly or perhaps monthly basis.

Below, you’ll find daily, weekly, monthly, and seasonal kitchen cleaning checklists to simplify your routine. These detailed guides will help you create and maintain a tidy kitchen space.

Supplies You’ll Need

The Spruce / Sanja Kostic

Before you get started, make sure you have the proper tools and cleaning solutions on hand. The following is a comprehensive list, detailing all of the supplies you need for the four kitchen cleaning checklists in this guide.

For your daily kitchen cleaning checklist, focus your attention on the counters and floors. Keeping these high-use areas clean will help you cultivate a more hygienic environment.

Remove any decor, appliances, or clutter from the countertops.

Wipe down the counters with a clean, damp cloth and an all-purpose cleaner or warm, soapy water. You can also use a DIY all-purpose cleaner, made of diluted vinegar. Consider wiping down high-use areas at this time as well, such as the drawer and cabinet pulls and the handle on your microwave.

Sweep the floors.

Return the items you moved to their proper homes on the countertop or elsewhere.

Unload your dishwasher and tackle any dirty dishes by handwashing or loading the dishwasher.

Wipe down the faucet and inside of your sink with an all-purpose cleaner. Pay close attention to any corners and crevices that may be collecting grime.

Take out the trash and recycling.

Put any cleaning rags or kitchen towels in the laundry and replace them with clean ones.

Weekly Kitchen Cleaning Checklist

The Spruce / Jenelle Botts

In addition to your daily cleaning regimen, your weekly routine should include frequently used appliances like your microwave and refrigerator. Start your weekly cleaning routine with the steps below, then finish with your daily kitchen cleaning checklist above.

Clean the interior and exterior of your countertop kitchen appliances, including your toaster, coffee maker, and microwave.

Next, it’s time to clean the refrigerator. You’ll need to rearrange or remove items as you clean, so you’re able to wipe down all of the shelf and drawer space. As you go, check for expired goods and toss them. Remember to wipe down the face and handles of your refrigerator too. (Save the freezer for your monthly kitchen cleaning checklist.)

Wipe down your stovetop with a store-bought or DIY all-purpose cleaner. Don’t forget to wipe down the face of your oven too.

Next, wipe down additional high-use areas, such as light switches, drawer pulls, cabinet handles, and door knobs.

Turn off (at the breaker box) and clean your garbage disposal, using distilled white vinegar and baking soda.

Finally, you can move on to the daily cleaning checklist and finish your weekly routine by mopping your kitchen floors.

Tip

During your weekly kitchen cleaning routine, take a look at your supplies and see if any cleaning solutions or tools need to be replaced or replenished. Take this opportunity to add those items to your grocery list.

Monthly Kitchen Cleaning Checklist

The Spruce / Sanja Kostic

Your monthly kitchen cleaning checklist provides an opportunity to tidy and disinfect areas that are not frequently used, but still collect dust and grime over time. This includes cabinet and drawer faces, windows, and even the inside of your garbage can. Start with your daily kitchen cleaning checklist, then move onto the tasks below.

Remove the contents of your cabinets and drawers to prepare for cleaning and organizing (we recommend following steps three and four for one cabinet or drawer at a time). This includes your pantry.

Wipe out the inside of your drawer or cabinet with an all-purpose cleaning solution, then move onto the cabinet or drawer face.

Return the contents of your cabinet or drawer, organizing as you go. Move onto the next drawer or cabinet and repeat steps three and four until you’ve tackled all of the storage space.

Wipe down any tiles and grout, such as a kitchen backsplash, with your all-purpose cleaner.

Next, wipe down areas that may be collecting dust, such as the tops of cabinets and light fixtures.

Clean the inside of your dishwasher with a soft abrasive brush or sponge, distilled white vinegar, and baking soda. Be sure to wipe down the face of your dishwasher with an all-purpose cleaner when you’re finished.

Seasonal Kitchen Cleaning Checklist

The Spruce / Ana Cadena

While the checklists above will help you maintain a clean and sanitary kitchen, there are a few leftover tasks you should complete every few months.

Set your oven to the self-clean setting. Keep in mind this process requires some prep (such as removing the racks and turning on the oven vent) and can take a couple of hours.

Using a microfiber cloth and all-purpose cleaning solution, wipe down the ceiling and walls in your kitchen. When you complete this step, pay close attention to areas that may have gathered grease or steam, such as the wall behind your kitchen faucet and the ceiling area above your vent hood.

When you empty and deep clean the cabinets and drawers in your kitchen (during the monthly kitchen cleaning checklist), search for any kitchen tools and utensils you can donate or toss. For cabinets or drawers with food (as well as the pantry), see if there are any items that need to be replaced or replenished, such as expired goods or spices running low.

Unplug your refrigerator and pull it away from the wall. Clean the top of your fridge, the floor underneath it, and even the coils behind it. Use a microfiber cloth and all-purpose cleaner for the top of your refrigerator and the coils, then a broom, dustpan, and mop for the floor. Plug the refrigerator back into the outlet, then return it back to it’s proper home.

Tips for Sticking to Your Kitchen Cleaning Schedule

Following the kitchen cleaning checklists above will take time and discipline, but there are several tips you can use to help you keep up with the chores.

Schedule kitchen cleaning days in your calendar. This is especially important for your monthly and seasonal kitchen cleaning checklists.

Keep your kitchen organized.Maintaining an organized kitchen will help prevent clutter, optimize your food storage, and notice and address any grease, spills, and other debris quickly.

Store your cleaning supplies in bins. Keeping the supplies needed for each checklist in labeled plastic bins can help you grab what you need quickly when it’s time to complete a cleaning checklist.

Declutter often. Instead of waiting until it’s time to complete your kitchen cleaning checklist, make sure you are frequently looking for and removing any expired products or tools/utensils that aren’t being used.

The high mortgage rates that have paralyzed America’s housing market are falling—and could nosedive further by the end of the year.

Rates for a 30-year fixed mortgage plunged to 6.47%—the lowest in over a year—for the week ending Aug. 8, according to Freddie Mac.

And with inflation losing steam and the economy cooling, expectations are high that the Federal Reserve could make not just one, but two rate cuts by the end of this year.

As a result, Realtor.com® senior economist Ralph McLaughlin expects mortgage rates to drop further in September and December, which is “encouraging news for potential homebuyers who have been waiting to participate in the market.”

This is also encouraging news for homeowners who might be thinking of selling. Is it time to finally list their property on the market? And if they do, what should they expect?

To help shed some light on what’s coming down the pike for home sellers, here’s what real estate experts predict will happen to the housing market once rates take the plunge.

The ‘lock-in effect’ will ease—and homeowners will start selling

A recent Realtor.com analysis found that 86% of homeowners have mortgage rates below 6%. Understandably, many feel “locked in,” unwilling to trade in their low rate for today’s higher ones if they sell and buy again.

“Home sellers have been sitting on the sidelines, not wanting to give up their COVID-era interest rates,” says Tan Tunador, vice president and senior loan officer with Atlantic Coast Mortgage.

But once rates drop further, that could change.

“The faster rates drop, the less homeowners will be held in place and we could see both new inventory and more sales,” says Danielle Hale, chief economist of Realtor.com.

“There are a significant number of sellers that couldn’t stomach—right or wrong—going from a 4% rate to a 7.5% rate,” says Mason Whitehead, a Dallas-based branch manager for Churchill Mortgage. “But they can stomach going from 4% to something in the 5% to 6% range.”

More homebuyers will enter the market

In the same vein that sellers have felt frozen in place, buyers have felt iced out of the market. But if mortgage rates continue to decline, then experts predict more buyers who’ve been on the sidelines finally jump into the market.

“When rates drop, I think you will see pent-up demand hit the market again,” says Whitehead.

Some buyers, like sellers, shelved their house hunt because they felt the payment was too high, but a lower rate makes home shopping more affordable.

“For some that didn’t qualify at 7.5%, they will qualify at 6%,” says Whitehead. “So you have more people able to buy as well.”

In other words, once rates fall, the market will see both more sellers willing to sell, and buyers willing and able to buy.

Sales will come on fast and strong

Any seller thinking of listing would be wise to start prepping right now.

“Mortgage rates have been improving, and they are bringing potential buyers out early, many of whom gave up on buying, either because of the low housing inventory or the higher rate environment the past few years,” says Tunador. “For sellers, listing their house early may give them the opportunity to sell before their competition hits the market.”

Other experts agree: There are definitely signs homebuying activity is beginning to bounce off the mat.

“Mortgage applications have perked up, and refinancing activity also looks to be picking up as rates go lower and owners carrying elevated mortgage rates seek to reduce their monthly payments,” says Charlie Dougherty, director and senior economist at Wells Fargo.

“All told, mortgage applications remain low, but the recent upturn is a promising sign that buying activity is starting to heat up and defrost a housing market frozen by higher interest rates,” adds Dougherty.

And if mortgage rates continue to shift south, things might get even toastier.

“When mortgage rates [stay in] a sub-6.5% average, we will really see the housing inventory increase and sales activity boom,” says Tunador.

Home prices will likely remain high

The good news for sellers is that even as the market gets moving, home prices are expected to remain high, or dip only slightly.

“Sellers will continue to be in a historically strong position, as the U.S. housing market is still short millions of homes,” says Dan Hnatkovskyy, co-founder and CEO of NewHomesMate. “Assuming there isn’t a severe recession, we will likely see only modest price decreases in most markets in 2024.”

However, Hnatkovskyy says that formerly hot markets like Denver, Austin, TX, and Phoenix may see a more significant drop in housing prices as smaller investor money sits on the sidelines for most of 2024. But in general, experts don’t see home prices taking a major dive as interest rates start to descend.

Even so, it will be smart for sellers not to get too cocky with their home pricing.

“Sellers may benefit from realistic pricing and encouraging buyer competition,” says Cassandra Happe, an analyst for WalletHub. “Working with a real estate agent to price strategically and enhancing online presence with 3D tours can maximize the chances of a quick and profitable sale.”

In other words, sellers shouldn’t set their hopes price too high lest they price themselves out of the market.

“Housing affordability will likely remain strained given still-high mortgage rates and the rapid run-up in home prices over the past three years,” says Dougherty. A shaky economy could “keep the pace of home sales relatively tepid.”

Multiple offers may make a comeback

The increase in competition among buyers might mean that sellers once again find themselves in the enviable position of being able to choose from several offers for their homes.

“Sellers will be in luck when mortgage rates start to drop: They’ll have multiple offers to consider and have some extra leverage when negotiating,” predicts Bryson Taggart, senior agent partnership manager for Opendoor. “For example, sellers receiving multiple offers can drive up the price of their home or waive contingencies for an easier close and a more convenient timeline.”

Still, sellers need to remember that the highest offer isn’t always the best offer.

“I advise sellers to evaluate offer terms holistically and select the one that aligns best with their wants and needs,” says Taggart.

For some, that could be an offer from a more qualified buyer or a cash buyer, which provides less of a risk for fall-throughs. If a seller is planning to also purchase a home, they should pick a buyer with favorable terms for an efficient close.

Enjoy these helpful tips and advice in this month’s edition of “Insights on Real Estate”:

1️⃣ Updated Rules for Selling a House;

2️⃣ Enchant Buyers With Stunning Fall Curb Appeal;

3️⃣ Understanding Down Payment Assistance Programs;

4️⃣ The Difference Between a CMA and an Appraisal; and

Let’s connect and plan your next steps. Find out if we’re the right real estate team for you!

CA Real Estate Group | Caliber Real Estate Group

👩🏻 Christine Almarines @christine_almarines

Realtor DRE# 01412944 | 714-476-4637

👩🏻 Anaid Bautista @wealthwithanaid

Realtor DRE# 02179675 | 949-391-8266

Spanish speaking

🏡 15216 Maidstone Ave, Norwalk 90650

🏡 3 bd | 1.75 ba | 1,241 sq ft | 5,000 sq ft lot | $825,000

———– OPEN HOUSE SCHEDULE:

🚩 THU, AUG 15, 3:00-6:30 PM

🚩 FRI, AUG 16, 3:00-6:30 PM

🚩 SAT, AUG 17, 1:00-4:00 PM

🚩 SUN, AUG 18, 1:00-4:00 PM

🍹 Come enjoy our iced tea and iced coffee bar!

———–

🌴 YOU CAN HAVE IT ALL…. Experience the best of modern living with this beautifully remodeled home, complete with a $20,000 NO-REPAYMENT GRANT. Use the grant for a rate buy-down, closing costs, down payment, or a combination of all three.

🌴 This home features 3 bedrooms, 2 bathrooms, and a 2-car garage, plus a convenient in-home laundry room.

🌴 Enjoy a primary bedroom with an en-suite bathroom and a versatile private space that can serve as a gym, office, dressing room, or a possible rental unit.

🌴 Additional highlights include oak wood-like floors, an upgraded kitchen with newer appliances, renovated bathrooms, split AC and a fully finished garage with its own AC and vaulted ceiling.

🌴 Located within walking distance to parks, schools, and stores, this home offers easy access to major freeways (91, 605, 5, 105, 710) and the Norwalk Green Line Station.

🌴 Come see this exceptional property for yourself!

———–

Stop by during our Open House or call and make an appointment for a private showing any day after Aug 15! See more photos of this gorgeous property here: https://marshalladamsmedia.hd.pics/15216-Maidstone-Ave

———–

👩🏻 Christine Almarines @carealestategroup

Buyers Agent Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

CA Real Estate Group | Caliber RE Group

———–

(Listed By Christine Almarines and Caliber Real Estate Group)

🏡 15303 Jersey Ave, Norwalk, CA 90650

🏡 3 bd | 2 ba | 1,434 sq ft | 5,002 sq ft lot | $699,000

———– OPEN HOUSE SCHEDULE:

🚩 SAT, AUG 17, 1:00-4:00 PM

🚩 SUN, AUG 18, 1:00-4:00 PM

———–

🌴 Spacious living room with laminate flooring opens to the dining room with a built-in cabinet.

🌴 The kitchen has new linoleum, maple cabinets, a Kitchen Aid oven and microwave combo, and a 4-burner cooktop.

🌴 Plenty of cabinet and counter space with a breakfast nook and laundry just off the kitchen area.

🌴 To service the three bedrooms is the hall bath with tile flooring and a tub/shower combo, sink with a solid Corian-like counter. The other bath also has a shower.

🌴 Double-pane windows, fresh paint both inside and out, and new carpet in all bedrooms.

🌴 The addition family room houses a fireplace, built-in bookshelves, and ¾ bathroom.

🌴 Possible workshop space in the 2- car garage with a newer garage door.

🌴 Amply shaded backyard is mostly brick for ease of care.

———–

Stop by during our Open House or call and make an appointment for a private showing! Take a virtual tour & more see more photos of this gorgeous property here: https://carealestategroup.com/15303-jersey-ave-norwalk/

———–

👩🏻 Anaid Bautista @wealthwithanaid

Buyers Agent Realtor DRE # 02179675

(949) 391-8266 | anaid@carealestategroup.com

CA Real Estate Group | Caliber RE Group

———–

(Listing by Edie Israel [DRE#01399225] and Keller Williams Realty)

Drying your laundry correctly doesn’t have to be complicated. Lean on this guide to simplify your drying routine.

Should you tumble dry low or normal dry? Is it better to dry towels and sheets together or separately? Knowing these laundry best practices can make your clothes last longer, save you energy, and reduce your monthly utility bill. Modern dryers boast an overload of advanced setting combos, from sanitization to activewear and even static-reducing options—which is why getting familiar with your model can help you get the most out of your dryer.

With the help of laundry and appliance experts, we’ve compiled all the do’s and don’ts of drying your clothes at home, whether you have a front- or top-loading dryer. And in case you are traveling (or shopping for a new dryer), this guide will also outline the common dryer settings found in today’s drying machines. The best part: You’ll be able to open your dryer with confidence, knowing your favorite tee hasn’t shrunk two sizes.

Prep Your Laundry Before You Dry

To maximize your laundry success, prevent wrinkles, and reduce your drying time, there are a few steps you can take before starting the dryer. First, sort your laundry before zapping it into your dryer (this step is especially important if you’re using an all-in-one washer-dryer), advises Zachary Pozniak, co-author of the upcoming The Laundry Book. “You should dry items of similar color and weight together,” he says. For example, “Do not dry dark jeans with lightweight white tee shirts. The tee shirt will be dry well before the jeans which will cause the shirt to be heavily wrinkled and covered in dark lint,” he adds.

Second, shake and untangle each piece right before tossing it into your dryer, and always follow your item’s care labels to protect your fabrics. Always be careful not to overload the dryer: Give your pieces some wiggle room to tumble freely inside your machine.

Lint clogged in your lint trap or ductwork can cause hot air from your dryer to spark a flame. Prevent this by keeping your dryer from working overtime—since clogged lint makes it harder for your machine to remove damp air from inside your dryer, resulting in greater energy expenditure and a more costly monthly bill—and clean it regularly.

Basic Dryer Settings

Normal, Regular Dry or Automatic

The hottest temperature a dryer can provide, this setting will tackle heavier items like towels, sheets, and sheets more efficiently, Pozniak says. But depending on your dryer model, this setting will either be labeled normal, regular, or automatic. Each of these cycles typically uses a moisture sensor to determine when clothes are dry, but you can also set a timer based on your preferences, Pozniak explains. He suggests reserving this setting for your most durable items like towels, bedding, sweats, and jeans while avoiding using this cycle on delicate items.

Note that ‘normal’ and ‘timed dry’ are the most popular cycles, according to David Wilson, senior commercial director for clothes care at GE Appliance. Each of these cycles represents around a quarter of all dryer cycles, based on GE’s data of more than 300 million cycles.

Delicate or Gentle

On the other hand, delicate settings use the lowest amount of heat and tumbling action, explains Pozniak. This cycle is best for fragile fabrics or laundry pieces that may start to melt, fray, stretch, or fade in high-heat conditions. Some examples can include activewear, spandex, underwear, lingerie, and sateen sheet sets.

Permanent Press or Wrinkle-Resistant

Wrinkle shield settings will help reduce wrinkles and keep shrinkage at bay. Typically using medium-heat settings, “permanent press is best for synthetic clothes like gym clothes,” says Pozniak, adding, “These garments dry very quickly, so the cycle uses lower temperatures, shorter drying times, and less tumbling to avoid wrinkling.”

Steam Setting

You’ll probably only see this setting on modern dryers, but this cycle adds steam to your laundry load to remove wrinkles. “However, it will not dry your garments, so expect them to be a bit damp to the touch (great for wrinkled bedding),” Pozniak says. “This can be used after a ‘proper’ dry cycle and viewed as a touch-up function.” You can also use this setting to de-wrinkle clean clothing without rewashing, as it uses a mixture of water and heat to revive clothing pieces.

No-Heat or Air-Fluff

This setting uses absolutely no heat, so it will not dry your garments like other settings. Pozniak says this cycle is ideal for stuffed items like duvet inserts, comforters, down jackets, and pillows. In addition, this air fluff setting can also help you remove pet hair and dust from your laundry pieces or even restore volume and freshen up the most delicate fabrics like wool or cashmere.

Quick Dry

Just as the name suggests, you can depend on this cycle to dry a small, light load in the nick of time.

Smart Dryer Settings

Smart dryer iterations are flooding the market right now, allowing you to streamline your laundry routine with intuitive features. For example, some dryers include dryer racks for items that require tumble-free drying (like tennis shoes). Others also come with compatible apps, where you can assign family members laundry tasks through customized texts and even cycle-match to get the perfect dry cycle that matches your load’s wash cycle. Some dryer machines can also be voice-activated when using a compatible voice-enabled device. Below, we’ve outlined a few features that you may want to consider when purchasing your next appliance.

ENERGY STAR-certified dryers follow energy efficiency guidelines set by the U.S. Department of Energy, using up to 30% less energy than standard dryers (and many times cost about the same as standard dryers).

Advanced moisture sensing: This setting is designed to adapt drying times to your garments, which helps prevent over-drying. Multiple sensors monitor the moisture and temperature of your clothes, so your drying cycle will end at just the right time.

EcoBoost: Some appliances come with a EcoBoost option that’s designed to use less heat to maximize energy efficiency.

Static-reduce: This setting combines a mist of water with tumbling after your load drys to further reduce static shock.

Sanitize cycle: A sanitizing cycle can eliminate common household bacteria and bugs (lice, bedbugs, moth larvae) thanks to its high heat levels, which can be ideal for sanitizing sheets or soiled clothing items.

Frequently Asked Questions

What happens if you use the wrong dryer setting?

The most common mistakes include over or under-drying your clothing. “Most shrinkage occurs in the washer, so you’ll likely have a very wrinkled garment from overdrying or one that’s still wet from underdrying,” Pozniak says.

Which dryer settings can be damaging?

“Timed dry can be very harmful as this overrides the moisture sensor,” Pozniak says. “Avoid using it if possible.”

Which items should not go in the dryer?

It’s best to hang or line dry synthetic clothes since they dry super fast, and any extended exposure to heat and tumbling will cause hard-to-remove wrinkling. Pozniak adds that this will break down your garments prematurely. He also advises against putting animal or protein-based textiles (such as silk, wool, and cashmere) in a tumble dryer. Instead, lay them flat on a towel to dry.

Thanks!

Please fill out the form below and we will be contacting you shortly with information about your home.

©2024 The Personal Marketing Company. All rights reserved. Reproductions in any form, in part or in whole, are prohibited without written permission. If your property is currently listed for sale or lease, this is not intended as a solicitation of that listing. The material in this publication is for your information only and not intended to be used in lieu of seeking additional consumer or professional advice. All trademarked names or quotations are registered trademarks of their respective owners.

©2024 The Personal Marketing Company. All rights reserved. Reproductions in any form, in part or in whole, are prohibited without written permission. If your property is currently listed for sale or lease, this is not intended as a solicitation of that listing. The material in this publication is for your information only and not intended to be used in lieu of seeking additional consumer or professional advice. All trademarked names or quotations are registered trademarks of their respective owners. As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.

As the visual shows, the biggest motivators were the desire to be closer to friends or family, outgrowing their current house, or experiencing a significant life change like getting married or having a baby. The need to downsize or relocate for work also made the list.:max_bytes(150000):strip_icc():format(webp)/kitchen-cleaning-checklist-6831396_06-12773541c7614c479e8fa0f24feeedeb.jpg)

:max_bytes(150000):strip_icc():format(webp)/kitchen-cleaning-checklist-6831396_22-0c01c2d56c52418b8481a1b2725b6284.jpg)

:max_bytes(150000):strip_icc():format(webp)/baking-soda-in-the-microwave-1900607-04-E-57505de715f549c1ad3737238ac61003.jpg)

:max_bytes(150000):strip_icc():format(webp)/kitchen-cleaning-checklist-6831396_08-0f654827d0424f7a88c15c7eafef9e49.jpg)

:max_bytes(150000):strip_icc():format(webp)/SPR-how-to-deep-cleaning-house-7152794-part-02-step-01-5738dadc88ec442aaa10d433e18cb7d7.jpg)