Hidden Costs of iBuying

Think of them as digital house flippers who scour mountains of data for typically off-market homes.

iBuying Explained

Known as iBuyers, these platforms buy houses for cash online. If the algorithms align well, homeowners who’ve submitted an online form will receive instant offers from interested iBuyers. The entire process usually takes place with no person-to-person contact. After buying the house sight-unseen (except for photos), iBuyers quickly resell, usually to other investors.

Transaction Fees

While iBuying may sound convenient, it has financial downsides. Industry experts say transaction fees can be significantly higher than in traditional home sales. Expect fee rates of around 7% of the home price, but be prepared for fee rates as high as 13%. Additionally, iBuyers most often make offers below market value.

Trust an Expert

You may think iBuyers can save you time and money. But an experienced real estate professional will work to get the best offer for your property and will be there to help find your next home.

Print This Article

When Is Buying More Affordable Than Renting?

Realtor.com® nailed it when they said the U.S. housing market was in for another whirlwind year. Its 2022 housing forecast predicted continued increases in housing prices, rent and mortgage rates in “a mixed bag of housing affordability challenges and opportunities.”

We’ve heard a lot about rising housing prices over the past few years, but rents are projected to increase at a pace of 7.1% compared to 6.6% for home sale prices. The report even goes so far as to say that buying a starter home would be cheaper than renting in some of the country’s largest metropolitan areas.

Choosing whether to rent or buy is a huge decision in any market. Fear of making “the wrong decision” intensifies as the market tightens. Still, you may be surprised to find that you can afford to buy after looking at your financial picture.

Consider these advantages of buying over renting.

Homeownership Is an Investment

At the end of a lease, you’ll walk away with nothing. At the end of a mortgage, you’ll own property with equity.

Stable Payments

Rent payments can rise with every new lease you sign. A fixed-rate mortgage offers stability.

Creative Freedom

A rental property is not yours to change as you please. But when you buy a house, you have the freedom to turn it into your dream home.

When deciding to buy or rent, carefully examine your budget, and think about your lifestyle and goals. If you’re considering buying but are apprehensive about the current market, a real estate professional can help you understand what’s happening in your community.

Print This Article

Supply Chain Issues Affect Housing Market

It’s no secret real estate values increased during the pandemic, with an unprecedented number of homes selling in bidding wars. Due to material shortages, delivery delays and cost increases, new home construction has struggled to keep up with the demand for housing. Lumber prices tripled from pre-pandemic levels, and these costs are often passed along to home buyers.

Although single-family housing starts have decreased, the number of homes under construction is actually up because houses aren’t getting finished. Besides a shortage of building materials, construction – like other industries – has experienced major labor shortages, a considerable hurdle to completing projects.

Despite current construction woes, experts predict home builders will overcome supply shortages this year, enabling them to speed up construction to meet ongoing demands for new housing. More inventory should help keep prices in check and curb last year’s sizable increases in home values.

Analysts are hoping that a gradual tapering down in housing starts may provide some relief, allowing builders to catch up with the backlog of demand.

Print This Article

6 Home Maintenance Tips for Sellers

Routine maintenance can be just as important after you’ve accepted an offer as it is before listing your home. To keep your house well-maintained throughout the transition, Realtor.com® recommends tending to these six areas.

- Carefully maintain the yard and walkways. Clean out flower beds and keep the yard tidy and free from leaves and downed tree limbs.

- Keep your gutters cleared to prevent water damage. Check the roof before the inspection.

- Service your HVAC system. Check your furnace, clean out ductwork and replace filters.

- Keep critters out by covering any holes and vents.

- Wash your windows no matter what time of year it is.

- Keep up with the current season. Decorations for long-passed holidays and other telltale signs that nobody’s home can be a nuisance to your neighbors.

Print This Article

Home Seller Tips for the Closing Process

OK, squint a little. See that? That’s the finish line, just ahead of you! After all the anxiety, hard work and waiting, you’ve almost made it to closing day. Don’t end up disappointed about a deal gone wrong because you skipped a few steps.

As annoying as it is, complete all promised repairs. No, you won’t be able to enjoy them, but they can make or break your sale. Plan to have everything finished and in working order at least one week before closing. This will allow time for any last-minute adjustments. Save receipts and invoices, and take before-and-after photos of repaired or improved items.

When flying through those closing documents, slow down when you get to the settlement statement. Check all of these numbers carefully to make sure they match what you were expecting to receive from the sale.

Print This Article

©2022 The Personal Marketing Company. All rights reserved. Reproductions in any form, in part or in whole, are prohibited without written permission. If your property is currently listed for sale or lease, this is not intended as a solicitation of that listing. The material in this publication is for your information only and not intended to be used in lieu of seeking additional consumer or professional advice. All trademarked names or quotations are registered trademarks of their respective owners. ©2022 The Personal Marketing Company. All rights reserved. Reproductions in any form, in part or in whole, are prohibited without written permission. If your property is currently listed for sale or lease, this is not intended as a solicitation of that listing. The material in this publication is for your information only and not intended to be used in lieu of seeking additional consumer or professional advice. All trademarked names or quotations are registered trademarks of their respective owners.

The Personal Marketing Company

11511 W. 83rd Terrace

Lenexa, KS 66214 |

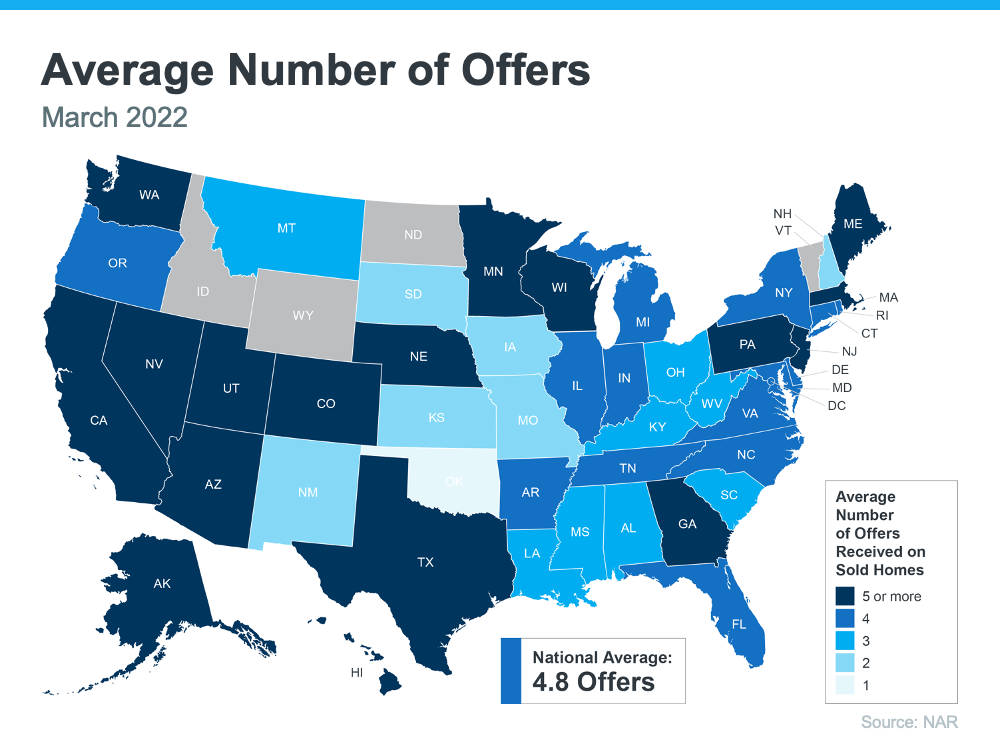

With a limited number of homes for sale today and so many buyers looking to make a purchase before mortgage rates rise further, bidding wars are common. According to the latest report from the National Association of Realtors (NAR), nationwide, homes are getting an average of 4.8 offers per sale. Here’s a look at how that breaks down state-by-state (see map below):

The same report from NAR shows the average buyer made two offers before getting their third offer accepted. In this type of competitive housing market, it’s important to know what levers you can pull to help you beat the competition. While a real estate professional is your ultimate guide to presenting a strong offer, here are a few things you could consider.

Offering over Asking Price

When you think of sweetening the deal for sellers, the first thought you likely have is around the price of the home. In today’s housing market, it’s true more homes are selling for over asking price because there are more buyers than there are homes for sale. You just want to make sure your offer is still within your budget and realistic for the market value in your area – that’s where a local real estate professional can help you through the process. Bankrate says:

“Simply put, being willing to pay more money than other buyers is one of the best ways to get your offer accepted. You may not have to increase it by a lot — it’ll depend on the area and other factors — so look to your real estate agent for guidance.”

Putting Down a Bigger Earnest Money Deposit

You could also consider putting down a larger deposit up front. An earnest money deposit is a check you write to go along with your offer. If your offer is accepted, this deposit is credited toward your home purchase. NerdWallet explains how it works:

“A typical earnest money deposit is 1% to 2% of the home’s purchase price, but the amount varies by location. A higher earnest money deposit may catch a seller’s attention in a hot housing market.”

That’s because it shows the seller you’re seriously interested in their house and have already set aside money that you’re ready to put toward the purchase. Talk to a professional to see if this is something you can do in your area.

Making a Higher Down Payment

Another option is increasing how much of a down payment you’re going to make. The benefit of a higher down payment is you won’t have to finance as much. This helps the seller feel like there’s less risk of the deal or the financing falling through. And if other buyers put less down, it could be what helps your offer stand out from the crowd.

Non-Financial Options To Make a Strong Offer

Realtor.com points out that while increasing these financial portions of the deal can help, they’re not your only options:

“. . . Price is not the only factor sellers weigh when they look at offers. The buyer’s terms and contingencies are also taken into account, as well as pre-approval letters, appraisal requirements, and the closing time the buyer is asking for.”

When it’s time to make an offer, partner with a trusted professional. They have insight into what sellers are looking for in your local market and can give you expert advice on what levers you may or may not want to pull when it’s time to write an offer.

From a non-financial perspective, this can include things like flexible move-in dates or minimal contingencies (conditions you set that the seller must meet for the purchase to be finalized). For example, you could make an offer that’s not contingent on the sale of your current home. Just remember, there are certain contingencies you don’t want to forego, like your home inspection. Ultimately, the options you have can vary state-to-state, so it’s best to lean on an expert real estate professional for guidance.

Bottom Line

In today’s hot housing market, you need a partner who can serve as your guide, especially when it comes to making a strong offer. Let’s connect so you have a trusted resource and coach on how to make the strongest offer possible for your specific situation.

💡 Find out if we’re the right Realtor Team for you! We’re active in our community…check out @carealestategroup

👩 Christine Almarines @christine_almarines

Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

👩 Michelle Kim @michellejeankim_homes

Realtor DRE # 01885912

714-253-7531 | michelle@carealestategroup.com

CA Real Estate Group is powered by Keller Williams Realty

The information contained, and the opinions expressed, in this article are not intended to be construed as investment advice. Keeping Current Matters, Inc. does not guarantee or warrant the accuracy or completeness of the information or opinions contained herein. Nothing herein should be construed as investment advice. You should always conduct your own research and due diligence and obtain professional advice before making any investment decision. Keeping Current Matters, Inc. will not be liable for any loss or damage caused by your reliance on the information or opinions contained herein.

Realtor.com | Jul 16, 2021

With the rocky year we’ve all had, it’s important to have a sanctuary in your own home where you can relax, unwind, and have a “Calgon, take me away” kind of experience. Establishing that personal space can do a lot of good for your mental health and well-being. But did you know it can also help increase your home’s value?

Bathroom renovations remain one of the most valuable home improvements. In fact, a midrange bathroom remodel can return up to 60% of your investment at the time of resale, according to Remodeling magazine’s Cost vs. Value report.

“We believe that a well-designed bathroom can make you a better person, which may seem like a bold statement,” says Joseph A. Tsedaka, principal at Nomi, which specializes in luxury bathroom remodels. “For some, that means including spalike features so you can unwind after a stressful day.”

Creating a luxurious bathroom space that you never want to leave can be done with a few simple tricks. Here’s what the design experts have to say.

Spa additions

If you’re trying to emulate luxury spas and saunas, providing the right shower experience is everything.

“Double showers are a must. We often recommend double showers with rain heads, hand-held features, and multiple faucets to create a truly relaxing experience,” says Tsedaka. He recommends adding a body sprayer, which can be customized to a homeowner’s height.

Other deluxe features to consider include built-in speakers and heated floors, to avoid that nasty shock of stepping onto cold tile with your bare feet.

Tsedaka says another popular addition is a smart home feature that allows everything (including lights, audio, and even the shower) to be controlled from the homeowner’s phone or an iPad on the wall.

Choose high-quality materials

“Even a neutral-tone bathroom can be elevated with finishes and hardware,” says Marlaina Teich of Marlaina Teich Designs in New York. “Choose unique tile for the shower, or consider marble chair rail molding around the bathroom for a classy, timeless look.”

Tsedaka says spa bathrooms tend to have more earthy materials like wood floors or natural stone in the shower.

“We love to use ipe wood, a naturally treated wood from Brazil that reacts excellently to water and moisture,” he says. “Teakwood also has a similar effect.”

Mel Bean of Mel Bean Interiors in Tulsa, OK, says thoughtfully curated mirrors can add to the look of your posh bathroom. Consider a classic rectangular mirror with a brass frame (CB2, $229) or something more geometric that’ll bring unique visual interest.

Layout

From toiletries to towels, the layout of your spa bathroom can add to the pleasing appearance.

“If you have the space, I would recommend installing a double vanity so each person has their own space, storage, and some privacy,” says Tsedaka.

He says it’s important to consider how you live, too. Do you actually take baths, or are you just including a bath for aesthetic reasons?

“We recommend coming from a place of functionality when considering the layout,” says Tsedaka.

For example, he says he prefers to have a drop-down tub if used frequently instead of a free-standing tub, which limits space.

“If you do have a free-standing tub, however, I always like to put it next to a window or a place where you can add a shelf to hold shampoo, soap, etc.,” says Tsedaka.

Lighting

Lighting, whether it’s natural or added, gives your bathroom a calming ambiance and a sense of sophistication.

When working with natural light, you’ll want to pick the right type of shades.

“To let in light when you want it, while also allowing for a darker, relaxing atmosphere, consider transitional or roller shades in the bathroom,” says James Brewer, a design consultant from Stoneside Blinds and Shades.

As for electrical light, Tsedaka recommends three different types of lighting: normal can lights, mood lighting using a dimmer, and chromotherapy lighting for inside the shower. “This is LED lighting that can change to any color you want,” he says.

For mood lighting he suggests using 4 inches for can lights on dimmers instead of the traditional 6-inch can light. He also says under-cabinet lighting or step light can be great for middle-of-the-night use when you don’t want to have direct light.

🏠 Are you a first time homebuyer? We can help customize a realistic plan that’ll help prepare you to buy your first home. The first step is to call us today!

💡 Find out if we’re the right Realtor Team for you! We’re active in our community…check out @carealestategroup

👩 Christine Almarines @christine_almarines

Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

👩 Michelle Kim @michellejeankim_homes

Realtor DRE # 01885912

714-253-7531 | michelle@carealestategroup.com

CA Real Estate Group is powered by Keller Williams Realty

Homelight | Jan 28, 2021

We’re continuing in our Weekly Series of “The 7 Most Painfully Expensive Home Repairs to Avoid.”

Today, we’re covering “Termite Damage.”

The average homeowner spent a total of $4,832 on routine and emergency home repairs in 2019. However, some of the most expensive home repairs have the ability to wipe out your entire yearly maintenance savings and then some.

On top of being pricey, major problems like pest infections and structural instability can make your home difficult to market and sell, not to mention tank your property value. With this guide, real estate experts identify the worst home repairs for your wallet and offer expert insights into preventive maintenance and early detection.

Termite damage ($3,000)

If they can find it, termites love to eat the wood in a house. Often, homeowners only discover signs of termite damage after these destructive little pests have weakened the wood in their home to a significant extent. Mitigating this damage can cost a lot of money, so catching termite activity early is key.

Estimated cost to repair:

According to pest control specialist Orkin, $3,000 is the average amount people spend to mitigate termite damage.

Warning signs:

These signs of termite damage should be on your radar:

- Wood that makes a hollow sound when tapped

- Crumbling wood

- Mud tubes on the side of your home’s foundation

- Peeling paint

- Mold or mildew smell

- Wings, termite bodies, or termite droppings

Key prevention tactics: If you have the ability to avoid contact between wooden parts of your home and the ground, you can reduce your termite risk. Special layers and meshes exist to make it hard for termites to access the home. Moving mulch away from your foundation is also a good idea — you don’t want to create a “red carpet” for termites to waltz into your abode so easily.

Who to call for help:

Who to call for help: Call CA Real Estate Group at (714) 476-4637 for our preferred termite and pest control experts to evaluate the situation. Sites with reviews like HomeAdvisor have information on your local pest control specialists; you can usually get a termite inspection from the company with the best reputation and then use their services for mitigation if needed.

Keeping Current Matters | Feb 3, 2022

If your needs are changing, you may be thinking about sharing a home with additional loved ones, such as grandparents, adult children, or other extended family members. Whether it’s for financial or health-related circumstances, or simply because you’ve reached a new phase of life, you might be wondering if living with multiple generations under the same roof is a good move for you. Many people have found themselves in a similar situation and they’ve already made the choice to live in a multigenerational home.

What Is a Multigenerational Home?

The Pew Research Center defines a multigenerational household as a home with two or more adult generations. They include households with grandparents and grandchildren under the age of 25. As you weigh your options and decide if multigenerational living is right for you, here’s some helpful information highlighted by other homeowners living with additional loved ones.

The Benefits of Multigenerational Living

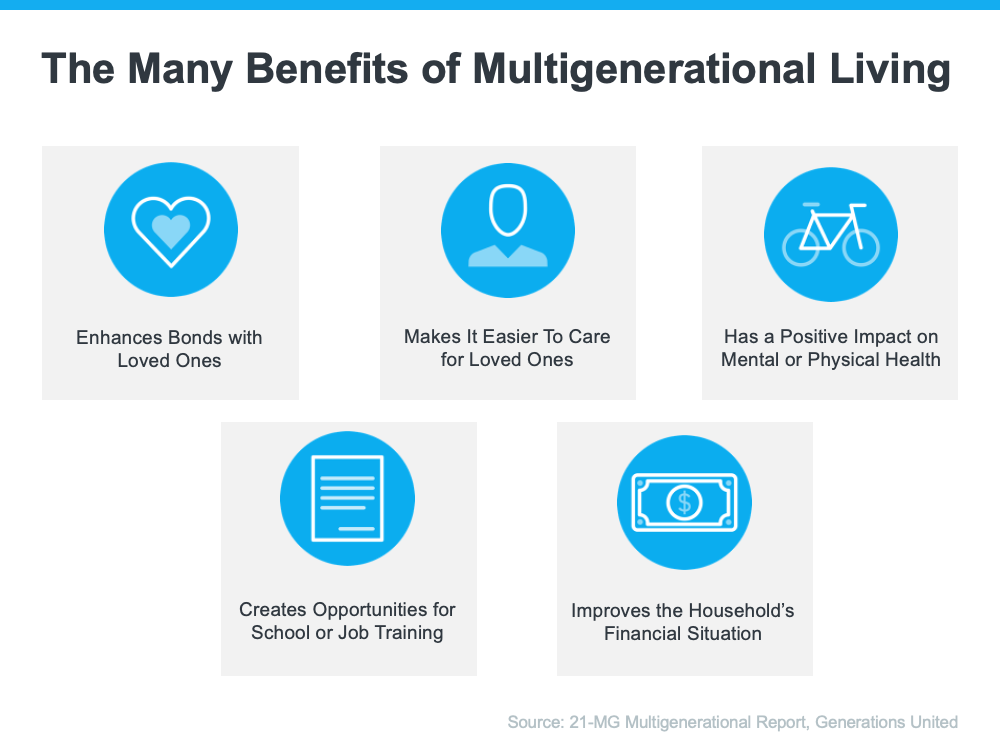

A recent report from Generations United surveyed individuals living in a multigenerational setting and asked them about the key benefits of this housing arrangement. It says:

“Nearly all Americans who live in a multigenerational household (98%) feel their household functions successfully, citing various aspects of home design, family relationships and interactions, and supports and services influencing their success.”

The study identifies some of the top benefits of this lifestyle as an improved financial situation, better mental and physical health, strengthened bonds with loved ones, and more (see chart below):

Those are just some of the reasons why most people who decide to live in this situation find it worthwhile. As Donna Butts, Executive Director at Generations United, says:

“Families may come together from need, but they are staying together by choice. Indeed, more than 7 in 10 (72 percent) of those currently living in a multigenerational household plan to continue doing so long-term.”

With More Adults Living Under One Roof, You May Need More Space

If you decide to look for a multigenerational home, it’s important to understand what everyone will need to make the arrangement work to its fullest. Something that often makes the top of the list for homeowners living with multiple generations is additional space for privacy. This could mean more bedrooms and bathrooms or features like an in-law suite or a basement.

If you’re realizing your current house doesn’t provide the room you need for multigenerational living, an expert real estate advisor can help you navigate the process to find the right home that works for you and your loved ones.

Bottom Line

Living in a multigenerational household has real and impactful benefits. If you’re interested in learning more about these options in our local area, let’s connect so you can find a home that fits your changing needs.

Homelight | Jan 28, 2021

We’re continuing in our Weekly Series of “The 7 Most Painfully Expensive Home Repairs to Avoid.”

Today, we’re covering “Electrical Rewiring.”

The average homeowner spent a total of $4,832 on routine and emergency home repairs in 2019. However, some of the most expensive home repairs have the ability to wipe out your entire yearly maintenance savings and then some.

On top of being pricey, major problems like pest infections and structural instability can make your home difficult to market and sell, not to mention tank your property value. With this guide, real estate experts identify the worst home repairs for your wallet and offer expert insights into preventive maintenance and early detection.

Electrical rewiring ($4,000-$12,000)

An older home’s electrical system easily can become overtaxed, causing fires and injury. In some cases a partial retrofit will suffice to make a house safe to live in. However, a number of old homes still have knob and tube wiring or aluminum wiring, both of which are fire hazards. If your house needs a full rewiring, the cost will be substantially higher.

Estimated cost to repair:

- 1,000-1,500 square foot home: $1,000-$6,000

- 2,000-2,500 square foot home: $4,000-$10,000

- 3,000 square foot home: $6,000-$12,000

(Source: Thumbtack, which tracks estimates from the millions of homeowners who use the site)

Warning signs:

If your breakers blow frequently, you see any visible damage to your wires, or notice a burning scent in the home, call an electrician to investigate the problem. An electrical inspection can determine whether old, outdated modes of wiring the house have put you in danger.

Key prevention tactics:

“In older homes, we’re finding that we need to have an electrician come out to cover lines to the water heater, so it isn’t a bare wire going from the water heater to the wall,” Harrison shares. While this won’t solve all the issues with old wiring, covering bare wires is key to reducing your fire risk, and a more thorough electrical inspection can help you find other concerning areas.

You should also install GFCI (ground fault circuit interrupter) outlets in the bathroom, kitchen, and anywhere outlets may come in contact with liquid. GFCI outlets interrupt an abnormal current flow to reduce the chance of electric shock.

Who to call for help: Call CA Real Estate Group at (714) 476-4637 for our preferred electricians to evaluate the situation, or check out Better Business Bureau’s Electricians Near Me portal helps you identify local electricians with proper credentials and positive ratings from past clients.

Keeping Current Matters | Feb 18, 2022

![What’s Driving Today’s High Buyer Demand? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/02/16141917/20220218-MEM-1046x1947.png)

Some Highlights

🏃 There’s an influx of buyers looking for homes today, and that means your house is in high demand. Here are a few reasons why so many people are looking to buy a home.

🏃 Buyers are motivated to beat rising mortgage rates, and many want to escape rising rents. There’s also additional demand from millennials who are reaching peak homebuying age.

🏃 If you’re thinking about selling your house, today’s demand is great news. Let’s connect to begin the process of listing your house while buyers are ready to purchase.

👩 Christine Almarines @christine_almarines

Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

👩 Michelle Kim @michellejeankim_homes

Realtor DRE # 01885912

714-253-7531 | michelle@carealestategroup.com

CA Real Estate Group @carealestategroup is powered by Keller Williams Realty

Homelight | Jan 28, 2021

We’re continuing in our Weekly Series of “The 7 Most Painfully Expensive Home Repairs to Avoid.”

Today, we’re covering “HVAC Replacement.”

The average homeowner spent a total of $4,832 on routine and emergency home repairs in 2019. However, some of the most expensive home repairs have the ability to wipe out your entire yearly maintenance savings and then some.

On top of being pricey, major problems like pest infections and structural instability can make your home difficult to market and sell, not to mention tank your property value. With this guide, real estate experts identify the worst home repairs for your wallet and offer expert insights into preventive maintenance and early detection.

HVAC replacement ($7,000-$10,000)

An HVAC performs the essential function of keeping your home a comfortable temperature year-round. While an HVAC has a typical life expectancy of about 15 years, it can fail much sooner than that if you don’t properly maintain the unit. As a complex piece of machinery, it has also earned a reputation for being one of the most expensive items to replace or repair in a house.

Estimated cost to repair:

- Average: $7,000

- High: $10,000

- Low: $5,000

(Source: HomeAdvisor heating and cooling cost estimate guide)

Warning signs:

If your system is having trouble turning on and off or fails to keep the home at the comfortable temperature that you’re accustomed to, you’ll want to get the HVAC serviced. Checking for problems before your system stops can be the difference between a reasonably priced repair and an expensive replacement.

Key prevention tactics:

Yearly maintenance by professionals can help you catch concerns early. In addition, replacing the air filter every couple of months will help prevent wear and tear.

Who to call for help: Call CA Real Estate Group at (714) 476-4637 for our preferred HVAC specialists to evaluate the situation, or check out BBB’s listings of HVAC Companies. Then check reviews on Google as well as around the web before selecting your top options for an HVAC company.

![How Remote Work Impacts Your Home Search [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/02/03134442/20220204-MEM-1046x2435.png)

Some Highlights

- If your workplace is delaying its return to office plans or is allowing permanent work from home options, that may open up new possibilities for your home search.

- Ongoing remote work could give you the chance for a change in scenery, a move to an area with a lower cost of living, or finding a home with more home office space.

- If you want to learn more about how remote work can give you more options, let’s connect to discuss your situation and priorities for your home search.