This infographic shows that the spring housing market could be a sweet spot for sellers. Main points:

The biggest challenge in the housing market is how few houses there are for sale compared to the number of people who want to buy.

The number of homes for sale is up from last year but below pre-pandemic numbers, and that means we’re still in a sellers’ market.

The housing market needs more homes for sale to meet the demand of today’s buyers. If you’ve thought about selling, now’s the time to connect with a local expert.

💭 DM us @carealestategroup and let’s chat about the best options for you!

💡 For more home maintenance tips, real estate advice, and fun family ideas, follow us at @carealestategroup — we are more than just real estate!

Stock prices and mergers often take center stage in business news reports, while small businesses are treated more like the ensemble cast. But maybe it should be the other way around. Small businesses account for a staggering 99.9% of American companies, according to the U.S. Small Business Administration Office of Advocacy.

And when they say small, they mean small. The majority of small businesses have one owner and no staff, and many have fewer than 20 employees. Still, nearly half of all jobs come from small businesses. In the past 25 years, small businesses have accounted for more than two-thirds of U.S. jobs.

With so much focus on tech giants and mega-corporations, sometimes the more subtle trends and new ideas coming from small businesses aren’t as apparent. Meaningful analysis of the U.S. economy should examine what’s happening in businesses of all sizes.

During 2022, the most profitable small businesses showed many entrepreneurs using their skills and interests to help other companies grow. Others focused on providing value by making everyday life more convenient or pleasant. Both online and in-person services have displayed solid growth and earning potential.

According to NerdWallet.com, these were last year’s most profitable types of small businesses.

Food trucks

Car wash services

Auto repair

Personal trainers

Newborn and post-pregnancy services

Enrichment activities for children

Mobile apps and entertainment for children

Shared accessories and attire

Shared home improvement equipment

Vacation rentals

Electronics repair

Academics courses

Language courses

Business or marketing courses

Personal wellness

Courses in hobbies or interests

Bookkeeping and accounting

Consulting

IT support

Graphic design

Social media management

Marketing copywriter

Virtual assistant services

Raising Money-Smart Kids

“Money doesn’t grow on trees!” Parents have said this to their children for generations, but the key is to back it up with information that shows how money does grow. Experts say teaching children the value of saving money is crucial to future financial stability. Saving also helps develop other good habits like discipline, goal setting, planning, and delayed gratification.

Start with a simple piggy bank (or any type of container) that enables young savers to see how coins and dollars add up in real time.

Check out money-saving apps that use graphics and gamification to teach kids about earning and saving money.

Establish guidelines for how much children should save from earned income and monetary gifts.

Encourage saving by creating opportunities to earn money doing household chores.

Educate children on comparison shopping, saving and using credit wisely.

Overall, it’s wise to discuss age-appropriate money matters with your family to foster healthy, lifelong relationships with household finances.

How To Get Compensated for Flight Issues

Do airlines have to compensate you if they delay or cancel your flight? Are you entitled to hotel or meal vouchers? Answers can vary, so be sure you understand your rights before you fly.

Find out what to do if your luggage is lost or you get bumped because of overbooking, mechanical problems or weather delays. You can find up-to-date information on the Department of Transportation’s new Airline Customer Service Dashboard at Transportation.gov.

Consider buying your tickets with a credit card that covers flight cancellations and service interruptions. Be aware of airline policies before purchasing tickets so you know what to expect in the event of a problem.

Pro Tip: Invest in a luggage tag with GPS tracking.

Tips To Lower Your Monthly Bills

Finding ways to reduce expenses isn’t always easy. But with some planning and creativity, you may discover surprising ways to revise your budget and lower your monthly costs. Try tracking your spending for several weeks, then prioritize needs and wants. Use this information and these tips to save on major expenditures.

Mortgage

If your mortgage payment is too high, think about moving to a more affordable home. You can also explore additional options, such as raising the deductible on your homeowner’s insurance policy or bundling your home and auto insurance.

Utilities

Ask your cable, internet and cellphone providers for their best promotions. Research other utility options and switch to low-cost alternatives whenever available.

Transportation

If it’s practical, consider using public transportation. Refinance or trade in your car for a less expensive model. Look for a better deal on car insurance, and be sure to request all available discounts.

Food

Shop weekly grocery promotions, and buy only as much produce as you can use before it spoils. Cook at home more often and prepare enough food to save for leftovers.

Entertainment

Audit your streaming, subscriptions and other memberships for redundancies or little-used entertainment services.

4 Ways To Be More Productive on Your Phone

Instead of scrolling through social media when you have time to kill, why not get something done? Try these tips and tricks to boost your productivity no matter what kind of smartphone you have.

Put thoughts, ideas and drawings in a simple journal or notes app. Keeping all stray bits of information in one place is a productivity game-changer.

Dictate thoughts, ideas and reminders using your phone’s built-in microphone.

Purge, consolidate and organize things such as notes, emails, contacts, apps, texts, files, and photos. You may be surprised by how much unnecessary data you’ve accumulated.

Add shortcuts for frequent tasks on your home screen so they’re easily accessible.

Many of today’s homeowners bought or refinanced their homes during the pandemic when mortgage rates were at history-making lows. Since rates doubled in 2022, some of those homeowners put their plans to move on hold, not wanting to lose the low mortgage rate they have on their current house. And while today’s rates have started coming down from last year’s peak, they’re still higher than they were a couple of years ago.

Today, 93% of outstanding mortgages have a rate at or below 6%. That means a strong majority of homeowners with mortgages have a rate below what they’d get if they moved right now. But if you’re a homeowner in that position, remember that mortgage rates aren’t the only thing to consider when making a move. Your mortgage rate is important, but there are plenty of reasons you may still need or want to move. RealTrends explains:

“Sellers who don’t have to move won’t be moving. The most common sellers will be: Homeowners downsizing . . . people moving to get more space, [households] looking for better schools…etc.”

Top Reasons

So, if you’re on the fence about selling your house, consider the other reasons homeowners are choosing to make a move. A recent report from the National Association of Realtors (NAR) breaks down why homeowners have decided to sell over the past year:

As the visual shows, the most commonly cited reasons for selling were the desire to move closer to loved ones, followed by moving due to retirement, and their neighborhood becoming less desirable. Additionally, the need for more space factored in, as did a change in household structure.

If you also find yourself wanting a change in location or needing space your current house just can’t provide, it may be time to sell.

What you want and need in a home can be reason enough to move. To find out what’s right for you, work with a trusted real estate professional who will offer advice and expert guidance throughout the process. They’ll be able to lay out all your options – giving you what you need to make a confident decision.

Bottom Line

When deciding whether or not to move, you have a lot to consider. There are plenty of non-financial reasons to factor in. Connect with a local real estate professional who can help you weigh the benefits of selling your house.

It doesn’t matter if you’re someone who closely follows the economy or not, chances are you’ve heard whispers of an upcoming recession. Economic conditions are determined by a broad range of factors, so rather than explaining them each in depth, let’s lean on the experts and what history tells us to see what could lie ahead. As Greg McBride, Chief Financial Analyst at Bankrate, says:

“Two-in-three economists are forecasting a recession in 2023 . . .”

As talk about a potential recession grows, you may be wondering what a recession could mean for the housing market. Here’s a look at the historical data to show what happened in real estate during previous recessions to help prove why you shouldn’t be afraid of what a recession could mean for the housing market today.

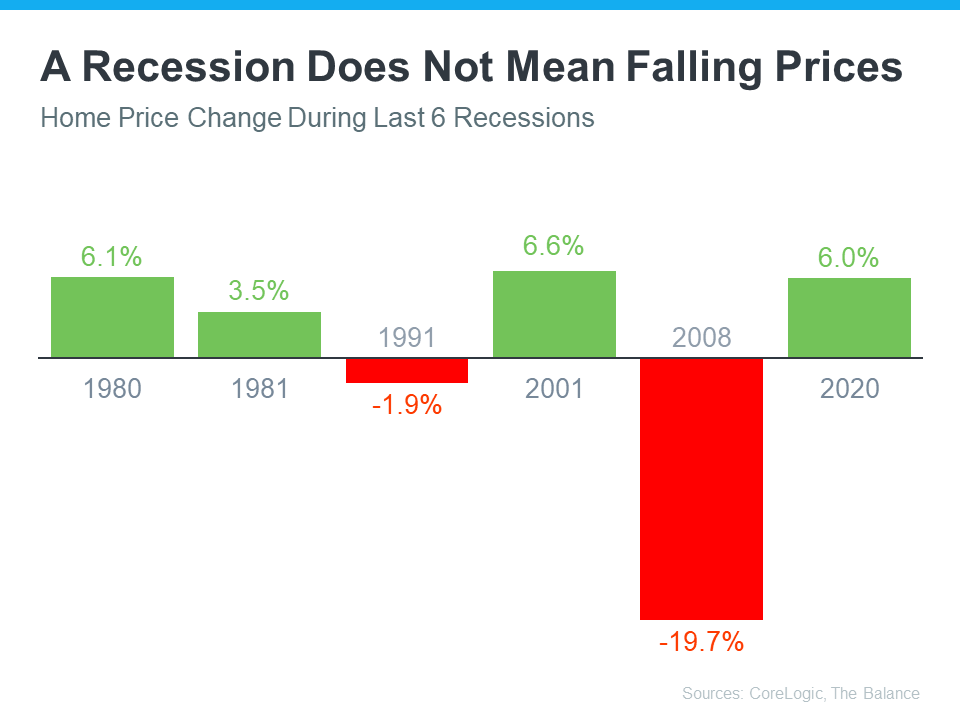

A Recession Doesn’t Mean Falling Home Prices

To show that home prices don’t fall every time there’s a recession, it helps to turn to historical data. As the graph below illustrates, looking at recessions going all the way back to 1980, home prices appreciated in four of the last six of them. So historically, when the economy slows down, it doesn’t mean home values will always fall.

Most people remember the housing crisis in 2008 (the larger of the two red bars in the graph above) and think another recession would be a repeat of what happened to housing then. But today’s housing market isn’t about to crash because the fundamentals of the market are different than they were in 2008. According to experts, home prices will vary by market and may go up or down depending on the local area. But the average of their 2023 forecasts shows prices will net neutral nationwide, not fall drastically like they did in 2008.

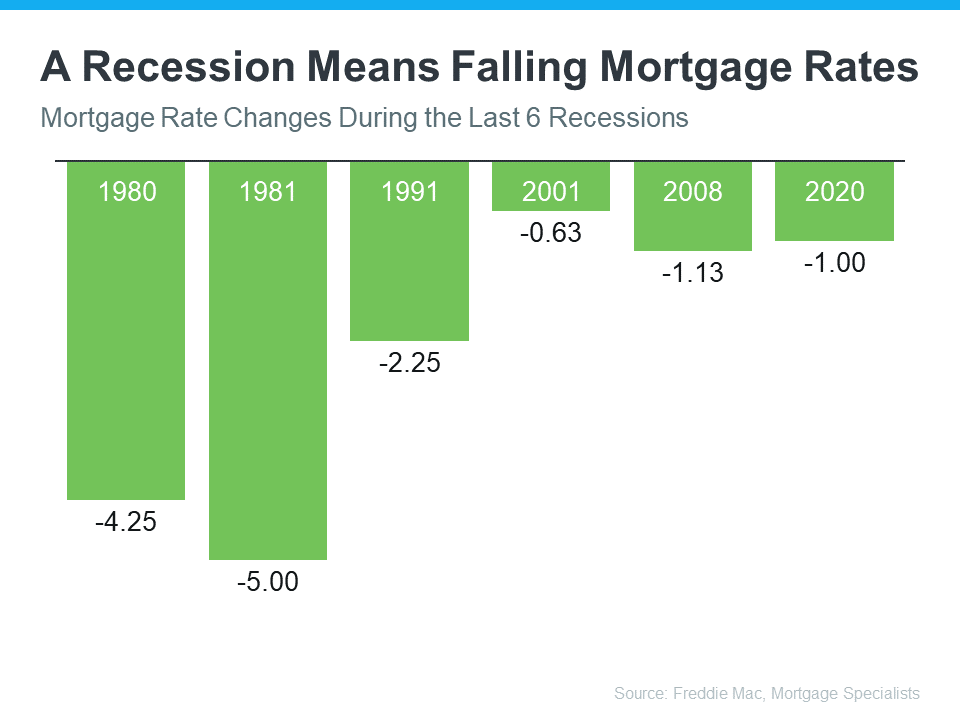

A Recession Means Falling Mortgage Rates

Research also helps paint the picture of how a recession could impact the cost of financing a home. As the graph below shows, historically, each time the economy slowed down, mortgage rates decreased.

Fortuneexplains mortgage rates typically fall during an economic slowdown:

“Over the past five recessions, mortgage rates have fallen an average of 1.8 percentage points from the peak seen during the recession to the trough. And in many cases, they continued to fall after the fact as it takes some time to turn things around even when the recession is technically over.”

In 2023, market experts say mortgage rates will likely stabilize below the peak we saw last year. That’s because mortgage rates tend to respond to inflation. And early signs show inflation is starting to cool. If inflation continues to ease, rates may fall a bit more, but the days of 3% are likely behind us.

The big takeaway is you don’t need to fear the word recession when it comes to housing. In fact, experts say a recession would be mild and housing would play a key role in a quick economic rebound. As the 2022 CEO Outlook from KPMG, says:

“Global CEOs see a ‘mild and short’ recession, yet optimistic about global economy over 3-year horizon . . .

More than 8 out of 10 anticipate a recession over the next 12 months, with more than half expecting it to be mild and short.”

Bottom Line

While history doesn’t always repeat itself, we can learn from the past. According to historical data, in most recessions, home values have appreciated and mortgage rates have declined.

If you’re thinking about buying or selling a home this year, let’s connect so you have expert advice on what’s happening in the housing market and what that means for your homeownership goals.

A new year brings with it the opportunity for new experiences. If that resonates with you because you’re considering making a move, you’re likely juggling a mix of excitement over your next home and a sense of attachment to your current one.

A great way to ease some of those emotions and ensure you’re feeling confident in your decision is to keep these three best practices in mind.

1. Price Your Home Right

The housing market shifted in 2022 as mortgage rates rose, buyer demand eased, and the number of homes for sale grew. As a seller, you’ll want to recognize things are different now and price your house appropriately based on where the market is today. Greg McBride, Chief Financial Analyst at Bankrate, explains:

“Price your home realistically. This isn’t the housing market of April or May, so buyer traffic will be substantially slower, but appropriately priced homes are still selling quickly.”

If you price your house too high, you run the risk of deterring buyers. And if you go too low, you’re leaving money on the table. An experienced real estate agent can help determine what your ideal asking price should be.

2. Keep Your Emotions in Check

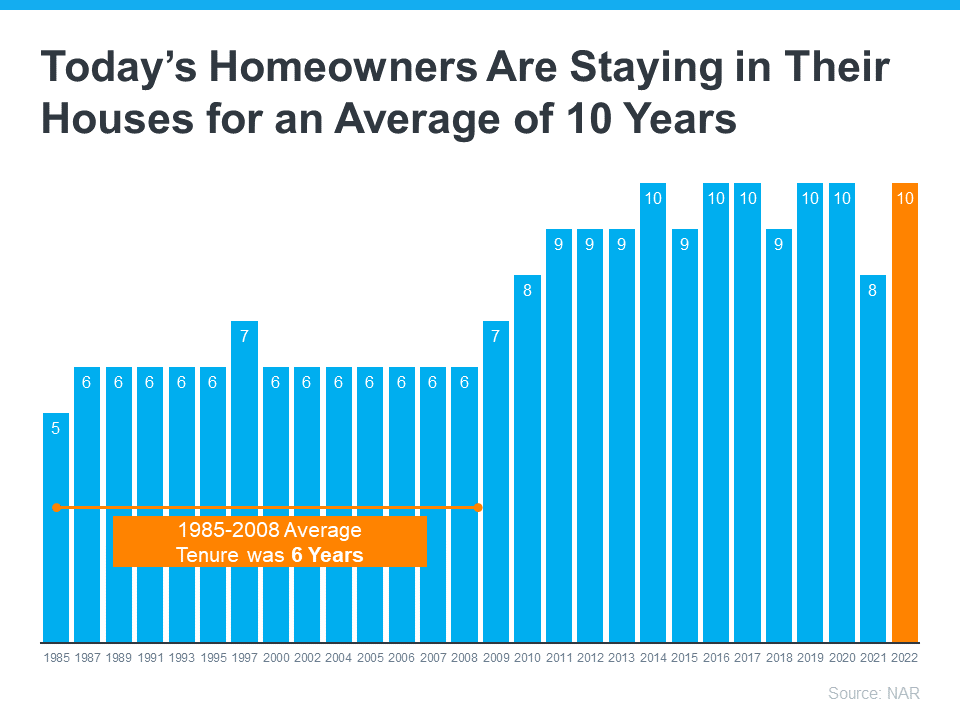

Today, homeowners are living in their houses longer. According to the National Association of Realtors (NAR), since 1985, the average time a homeowner has owned their home has increased from 5 to 10 years (see graph below):

This is several years longer than what used to be the historical norm. The side effect, however, is when you stay in one place for so long, you may get even more emotionally attached to your space. If it’s the first home you bought or the house where your loved ones grew up, it very likely means something extra special to you. Every room has memories, and it’s hard to detach from the sentimental value.

For some homeowners, that makes it even harder to negotiate and separate the emotional value of the house from fair market price. That’s why you need a real estate professional to help you with the negotiations along the way.

3. Stage Your Home Properly

While you may love your decor and how you’ve customized your home over the years, not all buyers will feel the same way about your design. That’s why it’s so important to make sure you focus on your home’s first impression so it appeals to as many buyers as possible. As NAR says:

“Staging is the art of preparing a home to appeal to the greatest number of potential buyers in your market. The right arrangements can move you into a higher price-point and help buyers fall in love the moment they walk through the door.”

Buyers want to envision themselves in the space so it truly feels like it could be their own. They need to see themselves inside with their furniture and keepsakes – not your pictures and decorations. A real estate professional can help you with tips to get your house ready to sell.

Bottom Line

If you’re considering selling your house, let’s connect so you have the help you need to navigate through the process while prioritizing these best practices.

If you’re thinking about buying or selling a home, you probably want to know what’s really happening with home prices, mortgage rates, housing supply, and more. That’s not an easy task considering how sensationalized headlines are today. Jay Thompson, Real Estate Industry Consultant, explains:

“Housing market headlines are everywhere. Many are quite sensational, ending with exclamation points or predicting impending doom for the industry. Clickbait, the sensationalizing of headlines and content, has been an issue since the dawn of the internet, and housing news is not immune to it.”

Unfortunately, when information in the media isn’t clear, it can generate a lot of fear and uncertainty in the market. As Jason Lewris, Cofounder and Chief Data Officer at Parcl, says:

“In the absence of trustworthy, up-to-date information, real estate decisions are increasingly being driven by fear, uncertainty, and doubt.”

But it doesn’t have to be that way. Buying or selling a home is a big decision, and it should be one you feel confident making. To help you separate fact from fiction and get the answers you need, lean on a local real estate advisor.

A trusted expert is your best resource to understand what’s happening at the national and local levels. They’ll be able to debunk the headlines using data you can trust. And using their in-depth knowledge of the industry, they’ll provide context so you know how current trends compare to the normal ebbs and flows in the industry, historical data and more.

Then, to make sure you have the full picture, they’ll tell you if your local area is following the national trend or if they’re seeing something different in your market. Together, you’ll use all of that information to make the best possible decision for you.

After all, making a move is a potentially life-changing milestone. It should be something you feel ready for and excited about. And that’s where an agent comes in.

Bottom Line

If you have questions about the headlines or what’s happening in the housing market today, let’s connect so you have expert insights and advice on your side.

Are you prepping to buy your first home? If so, one of the steps you should take early on is making sure you’re financially ready for your purchase. Here are just a few of the financial fundamentals you’ll need to focus on as you set out to buy a home.

Build Your Credit

Your credit is one element that helps determine which home loan you’ll qualify for. It also impacts your mortgage interest rate. While there are many factors that go into your mortgage application, a higher credit score could lead to a lower monthly payment in the long run.

So how do you make sure your credit is in the best shape possible when it’s time to buy? A recent article from NerdWallet lists a few tips you can use as you work to build and strengthen your credit. They include:

Tracking your credit and disputing any errors that show up on your reports.

Paying your bills on time. This includes making loan payments and paying down any open lines of credit.

Keeping your credit card balances low. Paying more than your minimum monthly balance when you’re able can help.

Automate Your Savings for Your House Fund

You might also be wondering how you can achieve your down payment savings goals. Bankrate provides buyers with a number of tips to help you save, including searching for down payment assistance programs and ways you can save more, faster. As the article says:

“One of the best ways to save for anything — including a down payment —is to set it and forget it. If you receive a regular paycheck, ask your employer to direct a portion of that payment into a savings account. If you’re a freelance worker or independent contractor, set up a recurring transfer from a checking account to a savings account to establish the routine.”

Get Pre-Approved

As you prepare for your purchase, you’ll also need to have a good grasp on your budget and how much you’ll be able to borrow for your home loan. That’s where the pre-approval process comes in.

Pre-approval from a lender lets you know how much money you can borrow for your home loan. And having that knowledge, plus an understanding of your savings, can help you decide on your target price range for a house.

From there, you can start browsing for houses online and see what’s available in your area in that general price point. This can help you really understand your options so you can start to picture your future home.

For Customized Advice, Build a Team of Professionals

Finally, the best way to make you’re prepared for your purchase is to connect with trusted real estate professionals. Having expert advisors in the industry will help you make strong decisions throughout the homebuying process based on your specific goals, finances, and situation. They know the market and can guide you toward the home of your dreams.

Bottom Line

If you’re ready to get the homebuying process started, connect with CA Real Estate Group to begin building your team of professionals today.

Homes Priced Correctly Sell Faster

Listing your property with a real estate professional will save you time, money and frustration. As you discuss the asking price, be aware of these common pitfalls.

Overpricing

By following recent home sales in your area, you can avoid unrealistic expectations stemming from runaway price growth over the past few years. Each day an overpriced house sits on the market is another day the sellers miss the opportunity to attract the right buyers. Price your property close to what you’d actually accept.

Underpricing

On the other hand, some sellers underprice their homes in hopes of starting a bidding war or making a quick sale. When your listing price is too low, you risk turning off prospective buyers who might suspect there’s something wrong with the house. You could also be leaving money on the table when would-be buyers present a lowball offer on your underpriced property.

Glossing Over the Comps

Your agent will find the best comparable sales of homes similar to yours in features, location and size. Their comparative market analysis can help you nail the asking price. You may not agree with everything in the comps, but try to be open to the information presented.

Overvaluing Upgrades and Improvements

As frustrating as it is, you’re not likely to get back 100% of what you paid for upgrades to your property. Check the comps to see what impact various improvements have made on the selling price of other homes.

Emotional Attachment

Getting too emotional when selling your house can complicate what is essentially a business transaction. Try to think of your property as a large asset you can put toward the purchase of your new home.

Checklist for Choosing a Mortgage Lender

A mortgage is a financial commitment that can affect your lifestyle for many years. Take your time selecting a mortgage banker or lender that best fits your needs and financial situation.

Whether you work with a traditional bank, credit union or specialized lender, follow these tips to find your best match.

Don’t assume you’ll be eligible for the advertised lending rates. Get a personalized quote from each lender.

Find someone you connect with. It helps if you agree on the best mode of communication, whether that’s email, texts or phone calls.

Make sure the lender offers the specific services you need, such as pre-approval. Ask about prepayment penalties or online-payment fees.

Check reviews for feedback about customer service and ease of making monthly payments.

Contact each lender and review your questions. Follow your instincts about whether this is a company you can trust.

Texture Enhances All the Senses

Texture is trending in home decor. Your artful attention to the often-overlooked sense of touch can make a huge difference in your home’s first impression. This is especially important whether you’re hosting a party or staging your home for an open house.

Let your imagination run wild when creating a cozy, inviting home. Multi-textured surroundings can dramatically warm a room, making you and your guests want to linger longer.

Pillows and accessories are great, but don’t stop there. You can add dimension and interest in many other ways.

Enhance walls with brick or stone veneer, textured wallpaper or decorative wood trim and molding. Look for affordable solutions such as removable stick-on wood panels or peel-and-stick wallpaper.

Add a woven rug to define your floor space. Shag carpet is an option for the truly daring.

Make your staging pop with cane or rattan furniture, tufted sofas or boucle-upholstered chairs. Balance colors and textures with neutrals and smooth fabrics. Pair a fuzzy throw with a leather loveseat. Draw subtle attention to unexpected spots with a vase, basket or small lamp.

Security Systems Offer Financial Savings

A home security system can provide peace of mind for you and your family and may help you save money. Consider these three benefits, according to industry analysts.

Increase Your Property Value

Buyers want a safe place to live and will likely pay more for a secure home. Reinforced exterior doors, strong locks and outdoor motion sensors also enhance the appeal of your property.

Decrease Your Insurance Costs

Some insurance companies offer a discount of up to 20% off your monthly premium if you have a professionally monitored security system.

Prevent Costly Burglaries

The average loss due to a home break-in is close to $3,000.

Why You Need an Agent With New Construction

New construction can be a challenging situation in home buying. While you get to select your favorite colors and finishes, the path from slick brochure to move-in day can be tricky. Here are some ways an experienced real estate agent can smooth that path, according to Realtor.com®.

Most agents are familiar with the construction process and can negotiate extras.

Agents have long-term, solid relationships with trusted lenders. Include (but don’t limit yourself to) their recommended lenders in your comparison shopping. The same goes for the builder’s preferred lender.

A real estate professional can oversee home inspections, following up on any remaining punch list items.

Pro Tip: Ask your agent to join you on your first site visit so the builder is aware you won’t be using their representative.

Here’s everything you need to know about what’s happening in the Real Estate Market.

Real Estate News in Brief

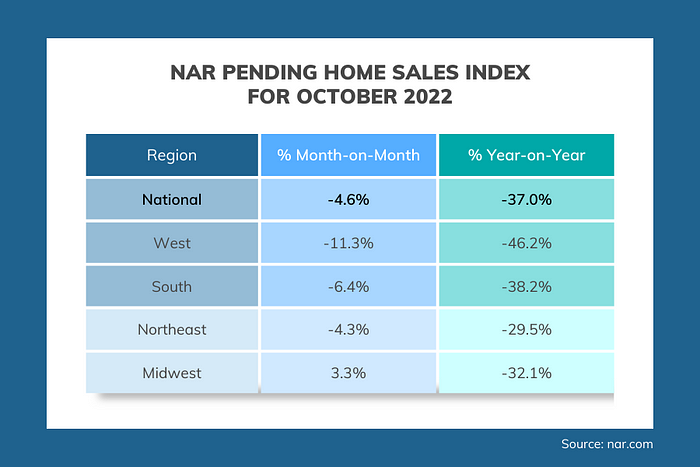

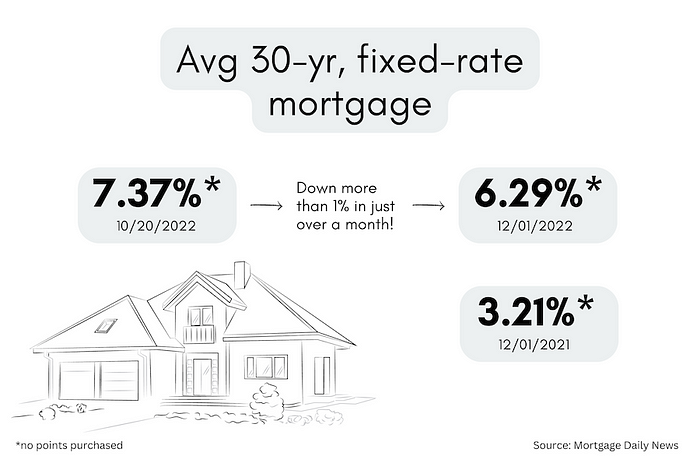

The NAR’s Pending Sales Index for October fell 4.6% in a month and 37% compared to October 2021. Pending sales in the West region were down 46%. [Source: NAR] Keep in mind that 30-yr mortgage rates were >7% for the entire month of October. They’re now around 6.3%.

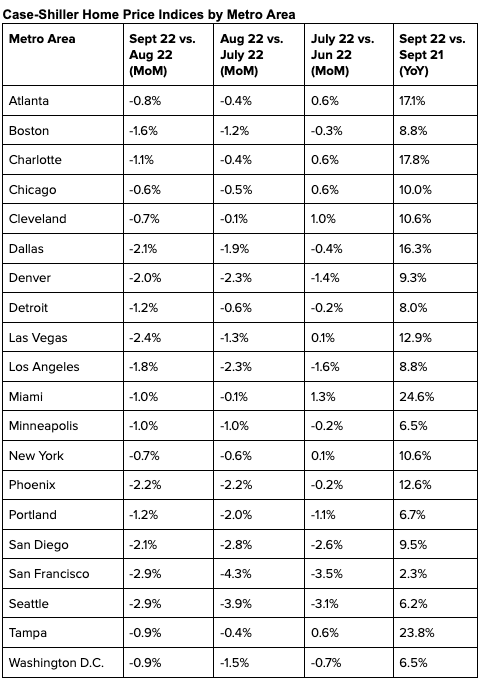

The Case-Shiller Home Price Index for September fell 1% in a month. From their peak in June, national home prices have slid ~2.5%, while prices in SFO & SEA are now down more than 10%. [Source: CoreLogic]

Fed Chair Jerome Powell said that “the time for moderating the pace of rate increases may come as soon as the December meeting” during a speech at the Brookings Institution. In other words, no more +75 bps.

The day after Powell’s comments, the PCE inflation figure for October came in at an annualized rate of 6%, better (that is to say, lower) than expectations and a further deceleration from 6.3% in September and the peak of 7% in June. [Source: BEA]

Companies added only 127k jobs in November, vs. +239k in October. This was well below Street expectations. Job losses in manufacturing & biz services dragged the total lower. [Source: ADP]

The NAHB’s Chief Economist expects a mild recession from 4Q 2022–2Q 2023, but sees mortgage rates at or below 6% by end-2023/early 2024, either because the Fed has ‘beaten’ inflation, or because the recession turns out to be bigger than expected. [Source: NAHB]

Pending Sales for October

With 30-year mortgage rates above 7% for the entire month, we knew that October pending sales would be bad — and they were. The NAR’s Pending Home Sales Index (PHSI) dropped 4.6% in a month. That’s the 5th-straight monthly decline in the PHSI. Compared to October 2021, the PHSI was down 37% YoY.

The contraction was significantly worse in the West, with October pending sales dropping 11% MoM and down 46.2% YoY. That’s right, pending sales nearly halved in the West.

Pending sales are a forward indicator of existing home sales (leading by 1–2 months). So prepare yourself for some nasty November and December existing home sales figures.

But there’s a silver lining: mortgage rates are already 90–100bps (a full percentage point) lower. As NAR’s Chief Economist Lawrence Yun wrote, “October was a difficult month for buyers as they faced 20-year-high mortgage rates…[but] The upcoming months should see a return of buyers as mortgage rates appear to have already peaked and have been coming down since mid-November.”

In fact, there are signs that a recovery in activity (thanks to lower rates) is already happening. The MBA (Mortgage Bankers Association) tracks new purchase loan applications on a weekly basis. This is the fourth week in a row that applications have risen week-on-week.

Case-Shiller for September

For the third consecutive month, home prices declined on a month-over-month basis. The national index was down 1.0% MoM, but the 20-city index was down 1.5% MoM. Don’t be fooled by the small numbers; these are big decreases. If this happened every month, prices would be down 12–18% in a year.

As in August, prices declined in each of the 20 big cities. However, for the cities experiencing the sharpest price drops (San Francisco, Seattle, Las Vegas etc.), the magnitude of price declines actually slowed a bit in September.

Source: S&P CoreLogic Case-Shiller Index

NAHB Webinar

Here’s how the National Association of Homebuilders’ Chief Economist, Robert Dietz, sees things:

2020–2021: Unsustainable, above-trend growth in home sales

2022–2023: Compensating below-trend growth in home sales

2024+: A return to trend growth in home sales (with >1 million in new home sales annually)

He expects a mild recession for the next three quarters, unemployment rates rising to near 6% (from 3% today) in 2024 and national home prices falling ~10%. At the same time, his message was essentially optimistic — lower inflation, interest rates and home prices will bring buyers (and builders) back relatively quickly.

A few anecdotes I found interesting:

~50% of the webinar attendees (most of whom were builders) said that they were responding to slowing demand with either price cuts OR enhanced incentives

The construction industry needs ~750,000 new workers every year to keep pace with demand and replace retirees

Right now, two cities in Texas (Houston and Dallas) are adding more new homes than the entire state of California

Note: In any given year, existing home sales are 7–15 times higher than new home sales. This isn’t because builders are lazy. It’s because there are around 145 million existing housing units. Even if builders were able to construct 2 million homes a year (something they’ve never achieved before), that would only raise the total housing stock by 1.3%.

Mortgage Market

After months of extreme volatility, 30-yr mortgage rates had flatlined at 6.6% for several weeks. But with another good (well, improving) inflation figure, and Powell sounding a bit less hawkish, the bond market was in party mode yesterday, rising 70–80 basis points.

Higher mortgage bond prices = lower mortgage bond yields = lower mortgage rates. Yesterday, the 30-yr mortgage rates moved sharply lower to 6.3% — that’s a full percentage point lower than the peak of 7.37% on October 20!

They Said It

“When home prices decline, it’s pretty rare for there to not be a recession.” — NAHB Chief Economist Robert Dietz

“To anyone with a sense of history, the home boom must be a source of wonder. Housing usually leads the economy into a recession. Mortgage rates rise, then housing construction and home sales fall.” — Robert J. Samuelson in a 2002 Newsweek article

Inspiration

There are many different approaches to measure ‘affordability.’ But they all depend on three factors: 1) household income, 2) home prices, and 3) mortgage rates.

Right now, all three factors are moving in buyers’ favor:

Workers are getting paid more

Home prices are starting to slide

Mortgage rates have peaked

Plus, there are more homes available, and less competition than last year, and sellers are more willing to negotiate on things like repairs, covering some closing costs, paying for points etc.

The key is to stay in regular contact with CA Real Estate Group. Your agent will let you know about price cuts, point out stale listings, and will keep you informed about mortgage rates. Also, waiting for the ‘perfect’ moment could be counterproductive. When (if!) conditions look perfect, they’ll look perfect to everybody else too.

Thanks!

Please fill out the form below and we will be contacting you shortly with information about your home.

©2023 The Personal Marketing Company. All rights reserved. Reproductions in any form, in part or in whole, are prohibited without written permission. If your property is currently listed for sale or lease, this is not intended as a solicitation of that listing. The material in this publication is for your information only and not intended to be used in lieu of seeking additional consumer or professional advice. All trademarked names or quotations are registered trademarks of their respective owners.

©2023 The Personal Marketing Company. All rights reserved. Reproductions in any form, in part or in whole, are prohibited without written permission. If your property is currently listed for sale or lease, this is not intended as a solicitation of that listing. The material in this publication is for your information only and not intended to be used in lieu of seeking additional consumer or professional advice. All trademarked names or quotations are registered trademarks of their respective owners.