Reator.com | Jun 19, 2022

If you’re raring to buy a home, chances are you’ll need a mortgage. But which kind of mortgage should you get?

Home loans aren’t one size fits all, but come in a variety of forms to suit home buyers in different circumstances. One good place to start figuring out your options is a mortgage calculator, where you can plug in various home prices and and have this sum broken down into monthly payments. Still, in addition to a home’s price, you should carefully consider the type of loan you get.

Two of the main types of mortgages home buyers consider getting are a fixed-rate mortgage and an adjustable-rate mortgage, or ARM.

So what’s the difference between these two types of home loans? In a nutshell, a fixed-rate mortgage has an interest rate that stays the same over the life of the loan. An ARM, by contrast, has an interest rate that changes over time.

Before you seek out mortgage pre-approval, let’s break down the pros and cons of each loan so you can decide which one is right for you.

Fixed-rate mortgage

According to Wells Fargo Home Mortgage Area branch manager Chris Jurilla, the majority of homeowners tend to prefer fixed-rate mortgages. And for good reason: A fixed interest rate means your mortgage payments remain steady over the life of your loan.

“Fixed-rate mortgages provide more long-term stability,” Jurilla says. “And with rates still low, borrowers prefer the security of not risking a rate increase or adjustment if the market were to turn.”

If you’re a home buyer with steady employment who wants to put down roots in a community, a fixed-rate mortgage might appeal to you. This kind of loan is also advantageous to people approaching retirement, because the fixed payments make it easier to plan their finances.

The pros of a fixed-rate mortgage:

- Predictability: The interest rate doesn’t change for the life of the loan, giving home buyers peace of mind.

- Fixed costs: You can budget more easily as the rate and payments remain constant.

- Straightforward numbers: The math involved with figuring out your loan is way easier than for an ARM.

- Stability: This predictable loan is more appealing for the risk-averse.

And the cons:

- You’re locked in: You won’t be able to take advantage of falling interest rates without refinancing.

- Your borrowing has a ceiling: You may not qualify for as much house as you would like, because those mortgage payments are typically higher.

Adjustable-rate mortgage

An ARM starts out at a fixed, predetermined interest rate, likely lower than what you would get with a comparable fixed-rate mortgage. However, the rate adjusts after a specified initial period—usually three, five, seven, or 10 years—based on market indexes. If those indexes go up, your payment will go up, too (sometimes way up).

If you’re a more mobile or first-time home buyer who wants to keep your long-term options open, an ARM’s low introductory interest rate is certainly tempting. As long as you’re ready to move on before the introductory period ends, you’ll benefit from the advantage of making lower payments while you’re living in the home. And because your lender will be qualifying you based on a lower monthly payment, you could qualify for a more expensive house than you would with a fixed-rate mortgage.

“ARMs are best suited for investors or home buyers who have short-term ownership goals in mind,” says Jurilla. “Most opt for an ARM if they don’t foresee themselves staying in the home for an extended period of time. There are some who use it as a stepping-stone loan, a short-term solution with a lower monthly payment.”

The pros of an ARM:

- Low initial rate: There are lower rates and payments early in the loan term than in a traditional fixed-rate mortgage.

- You can borrow more: You have a chance of being approved for a more expensive house because your lender will look at the lower payment when qualifying you for the loan.

- Falling rates: Some ARMs allow you to automatically take advantage of lower rates without the hassle and expense of refinancing.

And the cons:

- Unpredictable rates: After the introductory term, payments and rates can rise substantially. However, if market indexes go down, that doesn’t necessarily mean your mortgage payments will, too. Be sure to read the fine print on your mortgage.

- Complicated mortgage agreements: You’ll need to understand the complex terms of your agreement, such as margins, caps, and adjustment indexes.

- Math and more math: You have to put in significantly more work to figure out the math of an ARM and how it could potentially affect your budget.

- Prepayment penalty: You can’t pay off your loan for the number of years specified in your agreement. So if interest rates jump while you still have a prepayment penalty in place, you can’t refinance or sell your home without incurring a huge cost.

Choose the loan that’s best for you

The 30-year fixed-rate mortgage is the most popular in America, but that doesn’t mean it’s perfect for you. An adjustable-rate mortgage can work well for many young or financially savvy homeowners. Still, many borrowers would rather deal with the stability of a fixed rate than the fluctuating payments of an ARM.

So, who wins? Either mortgage can—it all depends on your individual circumstances. Talk to a mortgage lender or mortgage broker to learn more about which one is right for you. And be sure you understand each loan’s terms, and always compare rates before signing onto a mortgage.

ListReports | Aug 4, 2022

“Depreciation” and “Deceleration” are two similar but different terms that you may be seeing in headlines right now.

If you follow the news you may be reading headlines right now that give the impression that home prices are going to take a dive. The reality is that this isn’t completely accurate, and headlines don’t provide a full picture into what’s going on. If you have questions about the market and current trends I’m here to help shed some light.

Leave us a comment or call us and let’s start the conversation!

📞 Call us today!

👩 Christine Almarines @christine_almarines

Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

👩 Michelle Kim @michellejeankim_homes

Realtor DRE # 01885912

714-253-7531 | michelle@carealestategroup.com

linktr.ee/carealestategroup

Some Highlights:

- It’s worth considering the many benefits of homeownership before you make the decision to rent or buy a home.

- When you buy, you can stabilize your housing costs, own a tangible asset, and grow your net worth as you gain equity. When you rent, you face rising housing costs, won’t see a return on your investment, and limit your ability to save.

- If you want to learn more about the benefits of homeownership, let’s connect today.

Christine Almarines @christine_almarines

Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

Michelle Kim @michellejeankim_homes

Realtor DRE # 01885912

714-253-7531 | michelle@carealestategroup.com

Enjoy these helpful real estate tips and advice in this month’s edition of Insights in Real Estate:

1️⃣ Buyers Consider ARMs as Interest Rates Rise

2️⃣ Making an Offer on a House That’s Contingent

3️⃣ Which Amenities Are Buyers Seeking?

4️⃣ Tapping Home Equity

5️⃣ Don’t Skimp on Home Inspections

Find more helpful real estate insights, homeownership updates, and money talk newsletters in our archive.

💡 Find out if we’re the right Realtor Team for you! Check out @carealestategroup

👩 Christine Almarines @christine_almarines

Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

👩 Michelle Kim @michellejeankim_homes

Realtor DRE # 01885912

714-253-7531 | michelle@carealestategroup.com

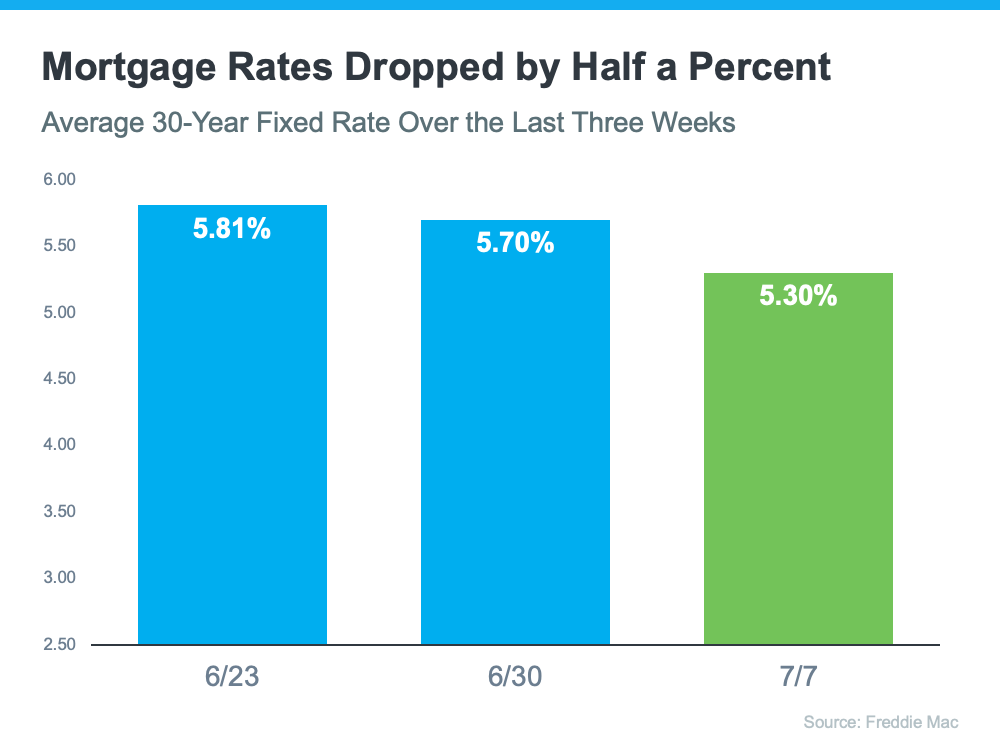

Over the past few weeks, the average 30-year fixed mortgage rate from Freddie Mac fell by half a percent. The drop happened over concerns about a potential recession. And since mortgage rates have risen dramatically this year, homebuyers across the country should see this decline as welcome news.

Freddie Mac reports that the average 30-year rate was down to 5.30% from 5.81% two weeks prior (see graph below):

But why is this recent dip such good news for homebuyers? As Nadia Evangelou, Senior Economist and Director of Forecasting at the National Association of Realtors (NAR), explains:

“According to Freddie Mac, the 30-year fixed mortgage rate dropped sharply by 40 basis points to 5.3 percent. . . . As a result, home buying is about 5 percent more affordable than a week ago. This translates to about $100 less every month on a mortgage payment.”

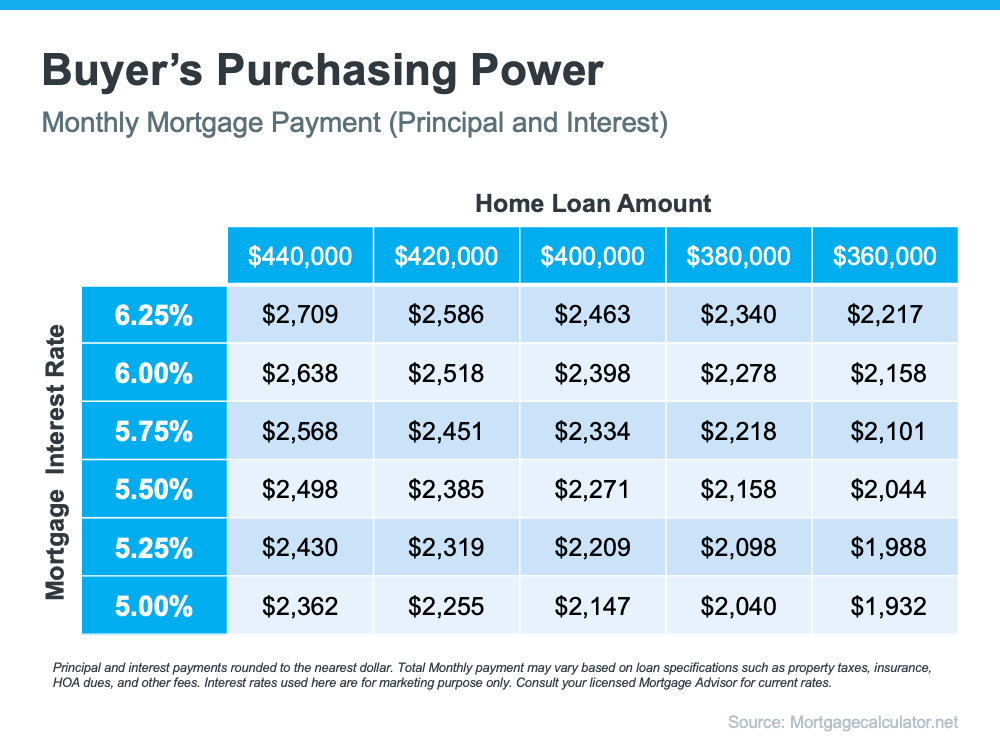

That’s because when rates go up (as they have for the majority of this year), they impact how much you’ll pay in your monthly mortgage payment, which directly affects how much you can comfortably afford. The inverse is also true. A decrease in mortgage rates means an increase in your purchasing power.

The chart below shows how a half-point, or even a quarter-point, change in mortgage rates can impact your monthly payment:

Bottom Line

If your home doesn’t meet your needs, this may be the opportunity you’ve been waiting for. Let’s connect to see how you can benefit from the current drop in mortgage rates.

This myth can stop potential homebuyers cold. The median listing price in the U.S. is $385,000 [$1.1 million in Orange County]. You would have to have $77,000 [$220,000 in Orange County] readily available if you wanted to make a 20% down payment, an amount that can be daunting for a lot of people.

“It’s one of the biggest myths out there,” says John Mallett, founder of mortgage broker MainStreet Mortgage. “It stops more people from entering the market or even seeing if they can qualify.”

In reality, 20% down is more of a guideline than a hard and fast rule. In fact, the average down payment equals 12%. For first-time buyers it goes down to 7%.

Government-backed options, such as FHA loans and USDA loans, can be secured with as little as 3.5% down. If you are a member of the armed forces or a veteran and you qualify for a VA loan, you can buy a home with 0% down.

Conventional loans also don’t require a 20% down payment, but with less money down you will generally need to pay for private mortgage insurance. PMI costs 0.5% to 1% of your loan amount per year and is paid in monthly installments. So, if you have the money to pay 20% down, however, it can make sense to do it. Having more equity also protects you if home values fall.

You can also apply for a number of different grants and homebuyer assistance programs that can provide money for a down payment. These programs can include grants, forgivable loans and second mortgages that can provide partial or full down payment help. (Brokerage Redfin has put together a list of down payment assistance programs available nationwide and by state.)

CA Real Estate Group can find solutions for you and connect you with our preferred mortgage experts. Call us today!

Christine Almarines @christine_almarines

Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

Michelle Kim @michellejeankim_homes

Realtor DRE # 01885912

714-253-7531 | michelle@carealestategroup.com

Source: https://money.com/housing-myths-debunked-home-buying/

Keeping Current Matters | Jun 24, 2022

![Why an Agent Is Essential When Pricing Your House [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/06/23153223/20220624-MEM-1046x2115.png)

Some Highlights

- When it comes to pricing your house, there’s a lot to consider. The only way to ensure you price it right is by partnering with a local real estate professional.

- To find the best price, your agent balances current market demand, the values of homes in your neighborhood, where prices are headed, and your home’s condition.

- Don’t pick just any price for your house. If you’re ready to sell, let’s connect to find the perfect price for your house.

💡 Find out if we’re the right Realtor Team for you! Check out @carealestategroup

👩 Christine Almarines @christine_almarines

Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

👩 Michelle Kim @michellejeankim_homes

Realtor DRE # 01885912

714-253-7531 | michelle@carealestategroup.com

Keeping Current Matters | May 26, 2022

You may be someone who looks forward to summer each year because it gives you an opportunity to rest, unwind, and enjoy more quality time with your loved ones. Now that summer is just around the corner, it’s worthwhile to start thinking about your plans and where you want to spend your vacations this year. Here are a few reasons a vacation home could be right for you.

Why You May Want To Consider a Vacation Home Today

Over the past two years, a lot has changed. You may be one of many people who now work from home and have added flexibility in where you live. You may also be someone who delayed trips for personal or health reasons. If either is true for you, there could be a unique opportunity to use the flexibility that comes with remote work or the money saved while not traveling to invest in your future by buying a vacation home.

Bankrate explains why a second home, or a vacation home, may be something worth considering:

“For those who are able, buying a second home is suddenly more appealing, as remote working became the norm for many professionals during the pandemic. Why not work from the place where you like to vacation — the place where you want to live?

If you don’t work remotely, a vacation home could still be at the top of your wish list if you have a favorite getaway spot that you visit often. It beats staying in a tiny hotel room or worrying about rental rates each time you want to take a trip.”

How a Professional Can Help You Find the Right One

So, if you’re looking for an oasis, you may be able to make it a second home rather than just the destination for a trip. If you could see yourself soaking up the sun in a vacation home, you may want to start your search. Summer is a popular time to buy vacation homes. By beginning the process now, you could get ahead of the competition.

The first step is working with a local real estate advisor who can help you find a home in your desired location. A professional has the knowledge and resources to help you understand the market, what homes are available and at what price points, and more. They can also walk you through all the perks of owning a second home and how it can benefit you.

A recent article from the National Association of Realtors (NAR), mentions some of the top reasons buyers today are looking into purchasing a second, or a vacation, home:

“According to Google’s data, the top reasons that homeowners cited for purchasing a second home were to diversify their investments, earn money renting, and use as a vacation home.”

If any of the reasons covered here resonate with you, connect with a real estate professional to learn more. They can give you expert advice based on what you need, your goals, and what you’re hoping to get out of your second home.

Bottom Line

Owning a vacation home is an investment in your future and your lifestyle. If this is one of your goals this year, you still have time to buy and enjoy spending the summer in your vacation home. When you’re ready to get started, let’s connect.

![Bright Days Are Ahead When You Move Up This Summer INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/05/26132018/20220527-MEM-1046x1913.png)

Some Highlights

- Warmer weather and longer days mean summer is almost here. Celebrate by upgrading to the home of your dreams so you can enjoy all the season has to offer.

- When you list your house, you can capitalize on today’s sellers’ market to fuel your upgrade. Then, you can move to a home with the features you want, like space to entertain or rooms for work and play.

- If you’re ready to upgrade to a home that matches your changing needs, let’s connect.

💡 Find out if we’re the right Realtor Team for you! Check out @carealestategroup

👩 Christine Almarines @christine_almarines

Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

👩 Michelle Kim @michellejeankim_homes

Realtor DRE # 01885912

714-253-7531 | michelle@carealestategroup.com

If you’re a first-time buyer looking to break into the housing market but struggling to find a home to buy, condominiums (or condos) could be a great alternative for you.

Here are a few reasons condos may be something you’ll want to consider.

Exploring Condos Could Add Options That Fit Your Budget

Supply challenges are a reality across the board in today’s housing market. Broadening your home search to include condos could increase your overall pool of options. Just keep in mind, condos generally differ from single-family homes in average space and floorplans.

In a recent article, Bankrate covers some of these differences:

“Condos are generally more affordable because they come with less space — you likely won’t have your own backyard, for example, and the interior tends to be smaller than the square footage of a single-family home.”

But if the size of a condominium meets your needs, they could match your budget as well. Data from the National Association of Realtors (NAR) shows the difference in the median price for both housing types. For single-family homes, the median price is $363,800. And for condominiums, the median price is lower at $305,400.

So, if budget is top of mind for you, a condominium could be a great fit within your target price range.

Not to mention, buying a condo is a great way to break into the market and start building equity that can help power a future move up. The condo you purchase today may not be your forever home, but it can be a great stairstep that can help you buy your dream home later on.

Find Out if Condo Living Is Right for You

In addition, owning and living in a condo is also a lifestyle choice. While it’s true they may be smaller than single-family homes, the amenities condos provide could be a draw for many buyers. Less space in your home might mean minimal upkeep, lower maintenance, and more time for you to spend doing the things you enjoy.

To understand if condo life is for you, Bankrate recommends asking yourself a few simple questions:

“Hate to mow the lawn and trim the hedges? What about pressure washing your driveway? Are your finances such that having to lay out $5,000 or more for a new roof will be a burden? . . . Condos tend to work best for those comfortable with most of the aspects of apartment living, minus the built-in maintenance.”

Ultimately, talking with an expert real estate advisor is the best first step to determining if condo living might work for you.

Bottom Line

Condominiums are a great option for many buyers, especially those looking to buy their first home. If you’re willing to consider condos in your search, you could find something that’s in line with your target numbers and your needs. To learn more, let’s connect so you have an expert in the condo-buying process on your side.

💡 Find out if we’re the right Realtor Team for you! Check out @carealestategroup

👩 Christine Almarines @christine_almarines

Realtor DRE # 01412944

714-476-4637 | christine@carealestategroup.com

👩 Michelle Kim @michellejeankim_homes

Realtor DRE # 01885912

714-253-7531 | michelle@carealestategroup.com

![Should I Rent or Should I Buy? [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/07/14124050/20220715-MEM-1046x2129.png)