Keeping Current Matters | Mar 7, 2025

Some Highlights

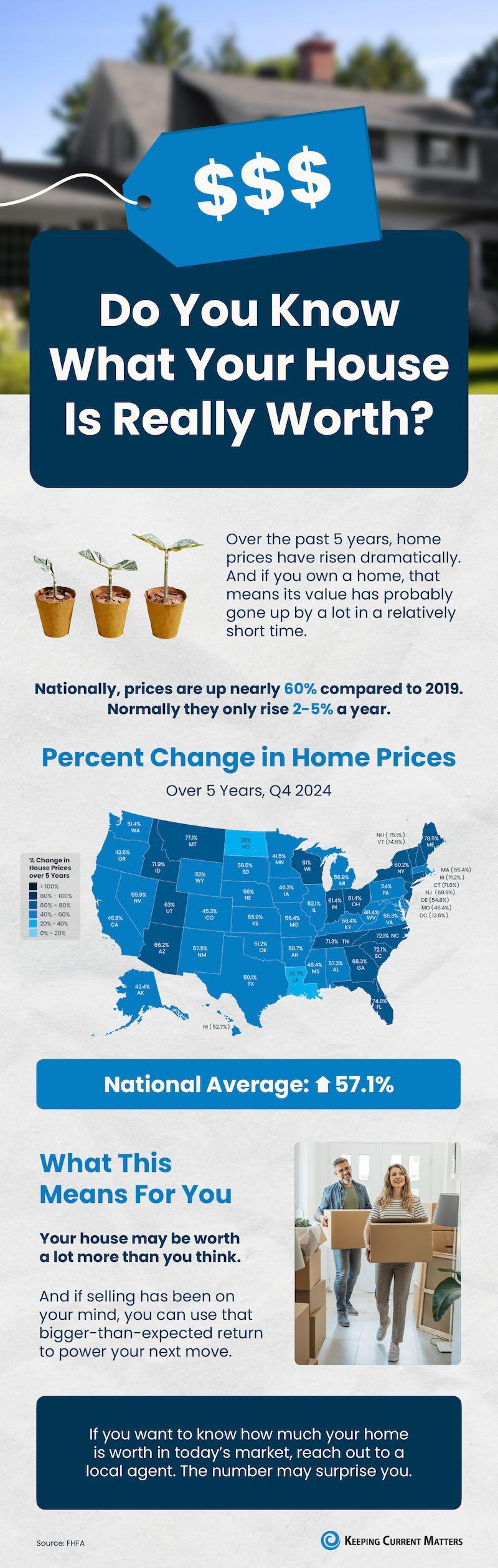

- Over the past 5 years, home prices have risen dramatically. If you own a home, that means your house may be worth a lot more than you think.

- Nationally, prices are up nearly 60% since 2019. And, if selling has been on your mind, you can use that bigger-than-expected return to power your next move.

- If you want to know how much your home is worth in today’s market, reach out to CA Real Estate Group. The number may surprise you.

Let’s connect and plan your next steps. Find out if we’re the right real estate team for you!

CA Real Estate Group | Caliber RE Group

Christine Almarines @christine_almarines

Realtor DRE# 01412944 | (714) 476-4637

Anaid Bautista @wealthwithanaid

Realtor DRE# 02179675 | (949) 391-8266

Letty Luna @lettylunarealestate

Realtor DRE# 02174000 | (562) 879-4181

PT Nguyen @sellsocalbuypt

Realtor DRE# 02223919 | (714) 756-0240

Keeping Current Matters | Mar 4, 2025

For the past few years, it’s been mostly a seller’s market. But dynamics are shifting as the number of homes for sale grows. And that means that the market is balancing out a bit. As a result, some sellers are finding they need to be more flexible to close a deal. One strategy that can help? Offering concessions.

As the National Association of Realtors (NAR) explains:

“As home inventory begins to grow and buyers regain some advantage in the market, sellers may consider offering more in negotiations to make the deal more attractive and get to the closing table.”

What Are Seller Concessions?

Concessions are homebuying costs that a seller agrees to cover as a way to get their house sold. And based on data from the National Association of Realtors (NAR), nearly 1 out of every 4 sellers (24%) offered a concession in 2024. Here are a few of the most common types of concessions:

- Covering Closing Costs: The seller pays for part (or all) of the buyer’s closing costs, like appraisal fees, title insurance, or loan fees.

- Price Adjustments: Instead of making repairs, a seller might lower the purchase price to make up for updates the buyer will need to tackle.

- Adding a Home Warranty: A seller may throw in a home warranty, giving the buyer peace of mind key repairs will be covered in the first year.

And don’t worry. This doesn’t mean you have to come up with more cash to make it happen. These are things that get subtracted from your profits at closing – not more funds you have to bring to the table. And not all concessions are about money.

There are other extras you could throw in. Like, if your buyer is coming from an apartment and has never had a yard before, they may ask if you’d be willing to leave your lawn mower behind. That’s another lever you could pull to keep them happy.

How Concessions Help Sellers

Offering concessions can be a smart strategy for sellers to get a deal done.As Dennis Shirshikov, Professor of Finance and Economics, City University of New York/Queens College told The Mortgage Reports:

“Pricing homes realistically and being willing to offer concessions, such as covering a portion of closing costs or including upgrades, will be key to closing deals . . . in a less frenzied market.”

For example, let’s say you accepted an offer from a buyer, but after their inspection, you found out there are some repairs they want you to tackle before you hand over the keys.

Rather than starting at square one and searching for a new buyer, you could offer a concession. One option is you can take on the repairs and cover the costs yourself. But, if you really don’t want the hassle of dealing with contractors, you could reduce your price by however much repairs would cost. Alternatively, you could offer to pay a portion of your buyer’s closing expenses with the idea they’d use the money they saved at closing toward doing the repairs themselves.

Either way, a concession can be a great way to meet in the middle. However, it’s important to have an agent on your side to help with these negotiations.

A good real estate agent can help you decide when and how to offer concessions, so you don’t give away too much while still ensuring your house gets sold. It’s all about finding the right balance.

Bottom Line

With the market becoming more balanced, seller concessions are coming back into play in some areas. The key is having an agent to help guide you through the process, so things work out in your favor.

What’s a concession you’d consider to move things along?

Let’s connect and plan your next steps. Find out if we’re the right real estate team for you!

CA Real Estate Group | Caliber RE Group

Christine Almarines @christine_almarines

Realtor DRE# 01412944 | (714) 476-4637

Anaid Bautista @wealthwithanaid

Realtor DRE# 02179675 | (949) 391-8266

Letty Luna @lettylunarealestate

Realtor DRE# 02174000 | (562) 879-4181

PT Nguyen @sellsocalbuypt

Realtor DRE# 02223919 | (714) 756-0240

Wondering what’s in store for the housing market this year? And more specifically, what it all means for you if you plan to buy or sell a home? The best way to get that information is to lean on the pros.

Experts are constantly updating and revising their forecasts, so here’s the latest on two of the biggest factors expected to shape the year ahead: mortgage rates and home prices.

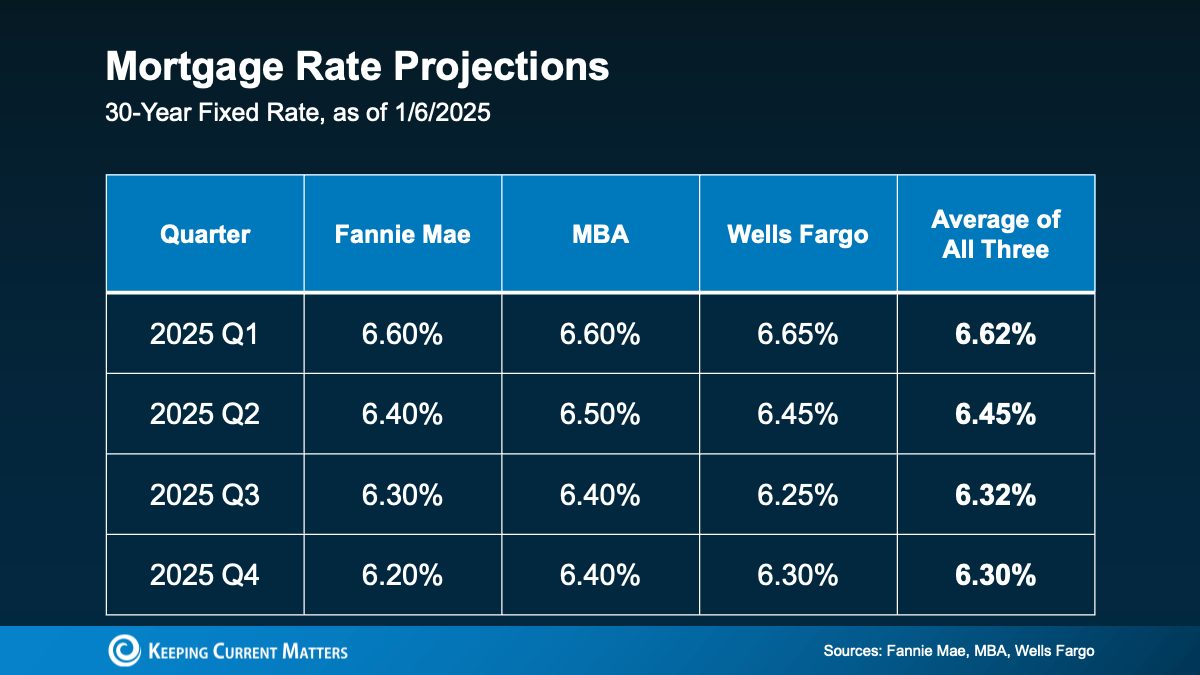

Will Mortgage Rates Come Down?

Everyone’s keeping an eye on mortgage rates and waiting for them to come down. So, the question is really: how far and how fast? The good news is they’re projected to ease a bit in 2025. But that doesn’t mean you should expect to see a return of 3-4% mortgage rates. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Are we going to go back to 4%? Per my forecast, unfortunately, we will not. It’s more likely that we’ll go back to 6%.”

And the other experts agree. They’re forecasting rates could settle in the mid-to-low 6% range by the end of the year (see chart below):

But you should remember, this will continue to change as new information becomes available. Expert forecasts are based on what they know right now. And since everything from inflation to economic drivers have an impact on where rates go from here, some ups and downs are still very likely. So, don’t get caught up in the exact numbers here and try to time the market. Instead, focus on the overall trend and on what you can actually control.

But you should remember, this will continue to change as new information becomes available. Expert forecasts are based on what they know right now. And since everything from inflation to economic drivers have an impact on where rates go from here, some ups and downs are still very likely. So, don’t get caught up in the exact numbers here and try to time the market. Instead, focus on the overall trend and on what you can actually control.

A trusted lender and an agent partner will make sure you’ve always got the latest data and the context on what it really means for you and your bottom line. With their help, you’ll see even a small decline can help bring down your future mortgage payment.

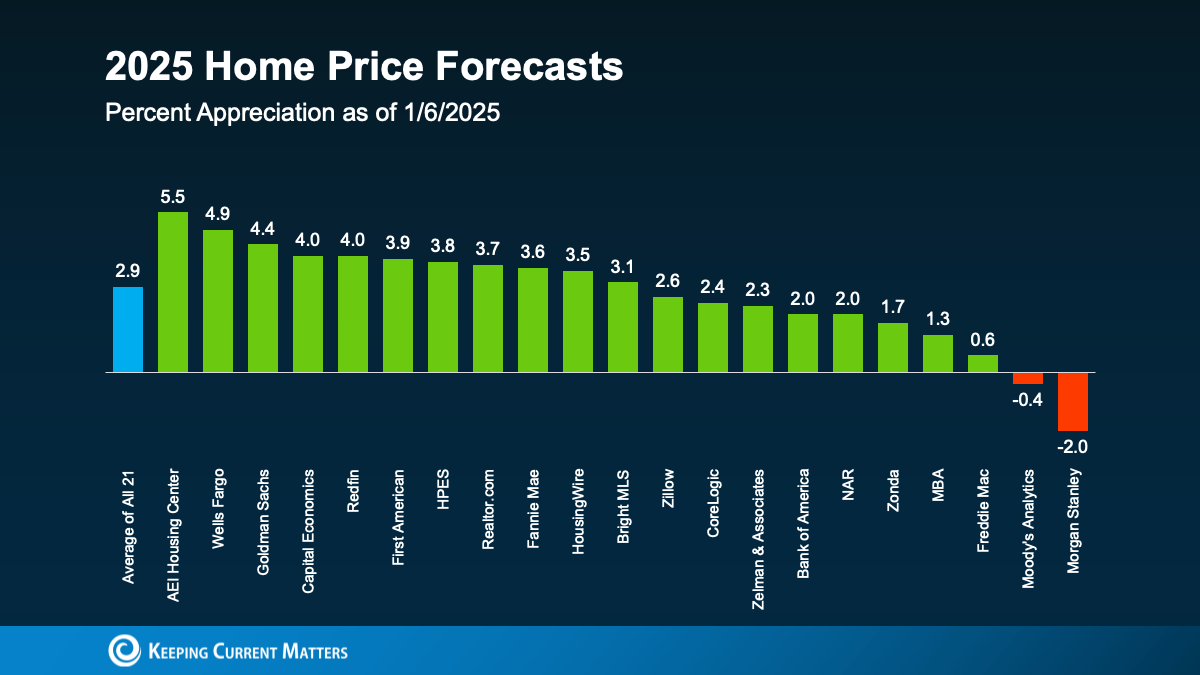

Will Home Prices Fall?

The short answer? Not likely. While mortgage rates are expected to ease, home prices are projected to keep climbing in most areas – just at a slower, more normal pace. If you average the expert forecasts together, you’ll see prices are expected to go up roughly 3% next year, with most of them hitting somewhere in the 3 to 4% range. And that’s a much more typical and sustainable rise in prices (see graph below):

So don’t expect a sudden drop that’ll score you a big deal if you’re thinking of buying this year. While that may sound disappointing if you’re hoping prices will come down, refocus on this. It means you won’t have to deal with the steep increases we saw in recent years, and you’ll also likely see any home you do buy go up in value after you get the keys in hand. And that’s actually a good thing.

So don’t expect a sudden drop that’ll score you a big deal if you’re thinking of buying this year. While that may sound disappointing if you’re hoping prices will come down, refocus on this. It means you won’t have to deal with the steep increases we saw in recent years, and you’ll also likely see any home you do buy go up in value after you get the keys in hand. And that’s actually a good thing.

And if you’re wondering how it’s even possible prices are still rising, here’s your answer. It all comes down to supply and demand. Even though there are more homes for sale now than there were a year ago, it’s still not enough to keep up with all the buyers out there. As Redfin explains:

“Prices will rise at a pace similar to that of the second half of 2024 because we don’t expect there to be enough new inventory to meet demand.”

Keep in mind, though, the housing market is hyper-local. So, this will vary by area. Some markets will see even higher prices. And some may see prices level off or even dip a little if inventory is up in that area. In most places though, prices will continue to rise (as they usually do).

If you want to find out what’s happening where you live, you need to lean on an agent who can explain the latest trends and what they mean for your plans.

Bottom Line

The housing market is always shifting, and 2025 will be no different. With rates likely to ease a bit and prices rising at a more normal and sustainable pace, it’s all about staying informed and making a plan that works for you.

Reach out to a local real estate pro to get the scoop on what’s happening in your area and advice on how to make your next move a smart one.

Keeping Current Matters | Dec 24, 2024

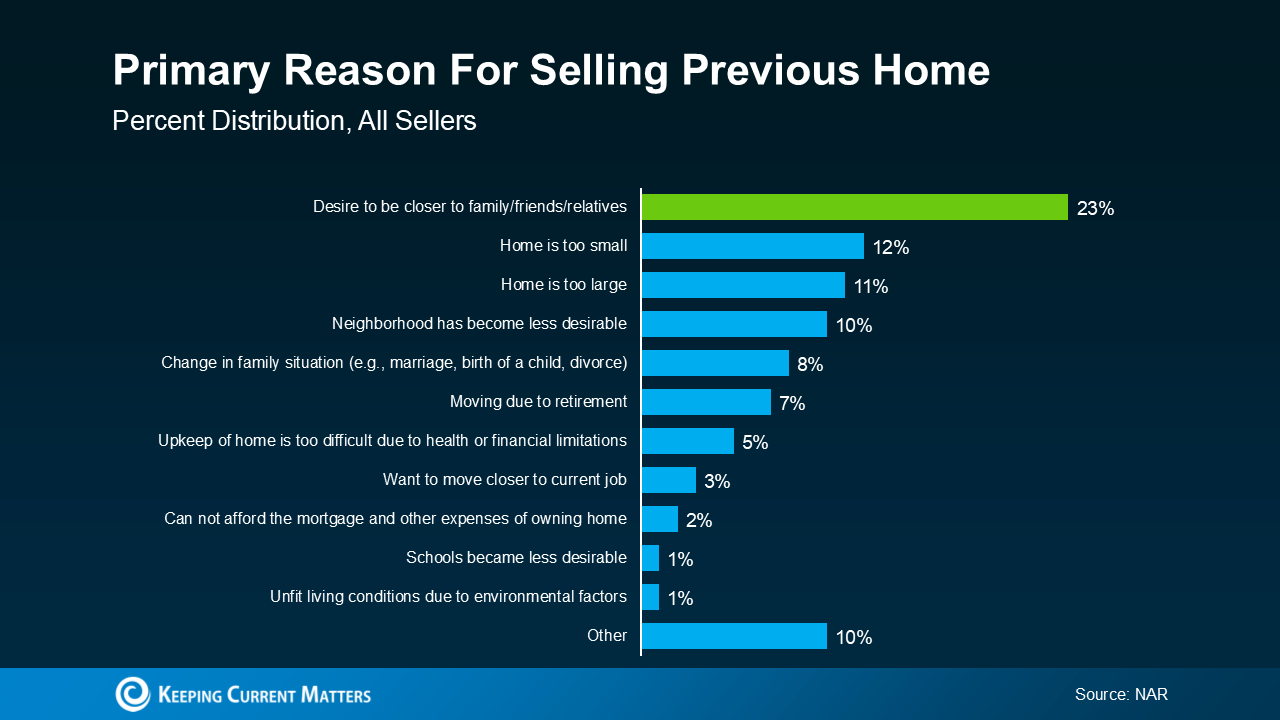

Have you ever thought about packing up and moving to be closer to the people who mean the most to you? Maybe you’re tired of long drives to see your family or wish your kids could spend more time with their grandparents. Clearly, a lot of other people feel the same way.

According to recent data from the National Association of Realtors (NAR), the desire to be near family and friends is the #1 reason people move (see graph below):

That’s because moving isn’t just about finding a new house – it’s about living a life where you’re surrounded by the people who matter most. Whether it’s catching up over weeknight dinners, watching your kids play with their cousins, or just knowing someone’s there when you need them, living near loved ones changes everything.

That’s because moving isn’t just about finding a new house – it’s about living a life where you’re surrounded by the people who matter most. Whether it’s catching up over weeknight dinners, watching your kids play with their cousins, or just knowing someone’s there when you need them, living near loved ones changes everything.

Let’s dive into why so many people are making this move and how it could be the best decision for you, too.

Why Family Comes First

Living near family and friends is a universal motivator that cuts across all types of buyers, whether you’re buying your first home or making a big lifestyle change.

But it’s especially important to repeat buyers. Unlike first-time homebuyers, who may be more focused on looking in more affordable areas, repeat buyers often have more flexibility on where they live. Many Baby Boomers, for example, have built significant equity in their homes, giving them the freedom to prioritize what matters most – like retiring near their grandkids. As Ali Wolf, Chief Economist at Zonda, says:

“25% of Baby Boomer households plan to retire near their children and grandchildren . . .”

Making a move to be closer to friends and family is all about creating a meaningful next chapter in your life where loved ones are just around the corner.

The Benefits of Living Near Loved Ones

But moving closer isn’t just a lifestyle choice – it’s a decision that offers real benefits:

- Spending More Time Together Whether it’s joining family dinners, going to weekend activities, or simply having someone nearby to talk to, these moments strengthen relationships and make life more fulfilling.

- Sharing Resources Living close to family can provide practical advantages, too – like sharing childcare, tools, or household items.

- Cutting Down on Travel Instead of spending hours on the road to spend time together, you can enjoy more spontaneous visits. This not only enhances your quality of life, but it also provides peace of mind in case of emergencies.

- Being There for Big Moments It also offers both emotional and practical support during life’s milestones. From graduations to tough times, being close to loved ones helps you feel connected and cared for.

Ready To Make Your Move?

At the end of the day, home isn’t just a place you live – it’s where your people are. Whether you’re looking to spend more quality time with family or enjoy the practical benefits of being closer to loved ones, the decision to move closer to those you care about is a deeply personal one.

Bottom Line

If you’re thinking about making a change, CA Real Estate Group would love to help. Together, you can explore neighborhoods that brings you closer to the people and places you love most.

Let’s Connect

Let’s connect and plan your next steps. Find out if we’re the right real estate team for you!

CA Real Estate Group | Caliber RE Group

Christine Almarines @christine_almarines

Realtor DRE# 01412944 | (714) 476-4637

Anaid Bautista @wealthwithanaid

Realtor DRE# 02179675 | (949) 391-8266

Letty Luna @lettylunarealestate

Realtor DRE# 02174000 | (562) 879-4181

PT Nguyen @sellsocalbuypt

Realtor DRE# 02223919 | (714) 756-0240

Coast One Mortgage | November 27, 2020The holiday months and winter may not be traditional peak homebuying seasons – there are historically less homes on the market – but there are actually advantages to being a buyer during the holiday season. With less competition, tax benefits, and motivated sellers, the holidays are actually a great time to buy a home. According to a report from ATTOM Data Solutions, December 26 is the #1 day of the year to purchase a home. Think of it like the Black Friday of real estate.

Here are some benefits and tips on buying a home during the holiday season.

1. Have a clear focus

In order to take advantage of savings during this time, you need to be organized and have a clear idea of what you want in a home so you can act quickly if needed. Make sure you have all of your financial documentation ready, have saved up a down payment, and have your “wants/needs” list on hand.

2. Look for motivated sellers

Many sellers who list their home during the holidays are motivated to sell for a variety of reasons. Whatever the reason, you can benefit by negotiating a great price on the house. Consider other incentives to ask for, like an adjusted closing date that works for you.

Available homes might have been on the market for some time, or you could even come across an “old expired listing” that didn’t previously sell during the original listing period and is active again. Private sellers are not the only motivated sellers during this season. Banks and other financial institutions are motivated to get foreclosed properties off of their books before the end of the year. Ask your real estate agent about these types of properties.

3. Tax benefits

Depending on your financial situation, and what your tax liability looks like for the upcoming calendar year, you could qualify for some tax benefits purchasing a home this time of year.

If you itemize deductions when you file taxes, you may be able to deduct points purchased upon closing, property taxes, and mortgage interest rates. If you’re purchasing a home as an investment asset, and have a business entity, there may be even more tax benefits available to you. Make sure you talk to your accountant for specific details.

4. Work with a well-connected real estate agent

Since fewer properties are listed between Halloween and New Year’s, you’ll want early access to the homes you’re most interested in. If you have a connected real estate agent, they’ll know about available properties ahead of time and be on the lookout for hidden gems or unpublicized listings.

Make sure your real estate agent’s communication style gels with yours, too. If you’re trying to take advantage of holiday listings, you’ll want your realtor to be responsive to both you and the seller’s agent of the property you’re interested in.

5. Inquire about Pocket Listings

Pocket listings are homes not listed on the local MLS (multiple listing service) or otherwise publicized. Sellers who want to maintain a certain level of privacy will often put their home up as a pocket listing. This is when having a savvy, connected real estate agent will really help you. Less visibility also means less competition for you as a buyer!

If you’ve found a home you love, or are ready to purchase a home, now might be the time for you! With less competition, you might have more luck putting down a smaller earnest money deposit – something that could be less successful when sellers are fielding multiple offers during busier times of year.

Take advantage of the perks and don’t let the holidays deter you from making an offer on a home this season.

Keeping Current Matters | Dec 3, 2024

A lot of people assume spring is the ideal time to sell a house. And sure, buyer demand usually picks up at that time of year. But here’s the catch: so does your competition because a lot of people put their homes on the market at the same time.

So, what’s the real advantage of selling your house before spring? It’ll stand out.

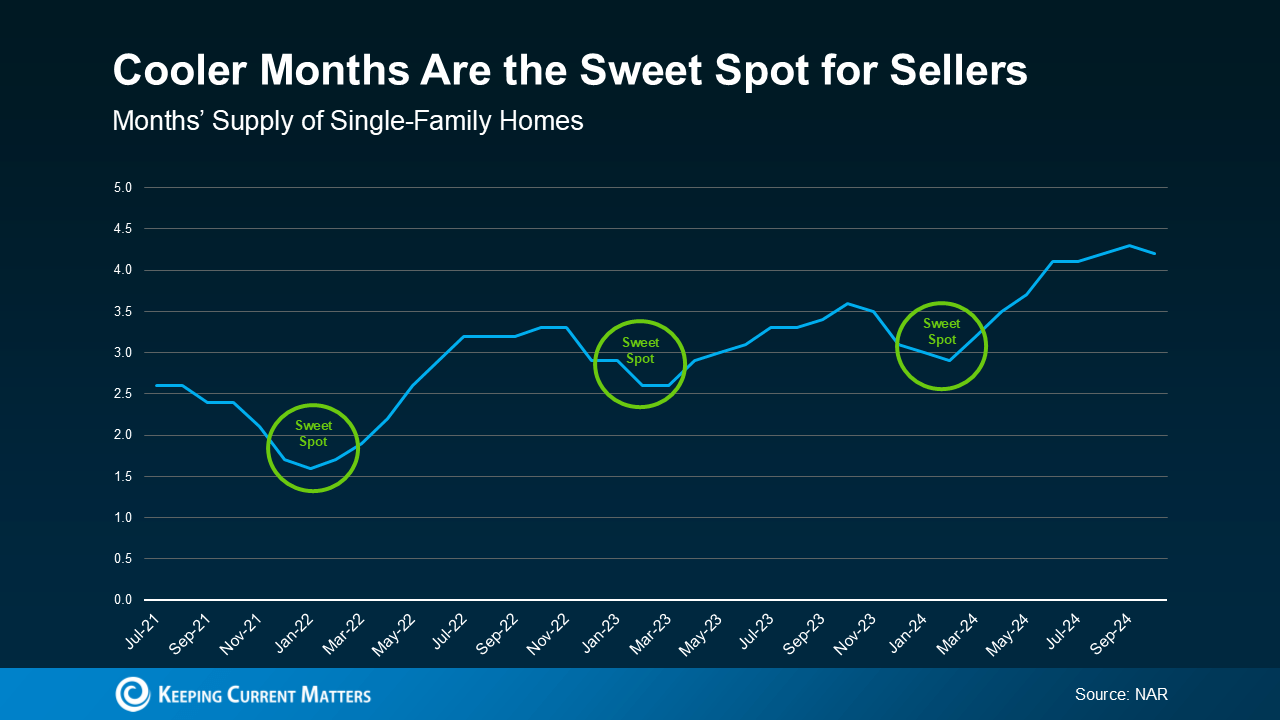

Historically, the number of homes for sale tends to drop during the cooler months – and that means buyers have fewer options to choose from.

You can see how that trend played out over the past few years in this data from the National Association of Realtors (NAR). Each time, the supply of homes for sale dipped during these cooler months. And then, after each winter lull, inventory started to climb as more sellers jumped into the market closer to spring (see graph below):

Here’s why knowing how this trend works gives you an edge. While inventory is higher this year than it‘s been in the last few winters, if you work with an agent to list now, it’ll still be in this year’s sweet spot. So, while other sellers are taking their homes off the market, you can sell before the spring wave of new listings hits, and your house will have a better chance of standing out.

Here’s why knowing how this trend works gives you an edge. While inventory is higher this year than it‘s been in the last few winters, if you work with an agent to list now, it’ll still be in this year’s sweet spot. So, while other sellers are taking their homes off the market, you can sell before the spring wave of new listings hits, and your house will have a better chance of standing out.

Why wait until spring when you can get ahead of the curve now?

Fewer Listings Also Means More Eyes on Your Home

Another big perk of selling in the winter? The buyers who are looking right now are serious about making a move.

During this season, the window-shopper crowd tends to stay busy with other things, like holiday celebrations, and avoids looking for homes when the weather’s cooler. So, the buyers out looking aren’t casually browsing—they’re motivated, whether it’s because of a job relocation, a lease ending, or some other time-sensitive reason. And those are the types of buyers you want to work with. Investopedia explains:

“. . . if your house is up for sale in the winter and someone is looking at it, chances are that person is serious and ready to buy.”

Bottom Line

With less competition and serious buyers on the hunt, you’ll be in a great position to sell your house this winter. Connect with CA Real Estate Group to get the process started. Call Team Lead Christine Almarines for a free consultation at (714) 476-4637.

Keeping Current Matters | Oct 30, 2024

No one likes making mistakes, especially when they happen in what’s likely the biggest transaction of your life – buying a home.

That’s why partnering with a trusted agent and real estate team like CA Real Estate Group is so important. Here’s a sneak peek at the most common missteps buyers are making in today’s market and how a great agent will help you steer clear of each one.

Trying To Time the Market

Many buyers are trying to time the market by waiting for home prices or mortgage rates to drop. This can be a really risky strategy because there’s so much at play that can have an impact on those things. As Elijah de la Campa, Senior Economist at Redfin, says:

“My advice for buyers is don’t try to time the market. There are a lot of swing factors, like the upcoming jobs report and the presidential election, that could cause the housing market to take unexpected twists and turns. If you find a house you love and can afford to buy it, now’s not a bad time.”

Buying More House Than You Can Afford

If you’re tempted to stretch your budget a bit further than you should, you’re not alone. A number of buyers are making this mistake right now.

But the truth is, it’s actually really important to avoid overextending your budget, especially when other housing expenses like home insurance and taxes are on the rise. You want to talk to the pros to make sure you understand what’ll really work for you. Bankrate offers this advice:

“Focus on what monthly payment you can afford rather than fixating on the maximum loan amount you qualify for. Just because you can qualify for a $300,000 loan doesn’t mean you can comfortably handle the monthly payments that come with it along with your other financial obligations.”

Missing Out on Assistance Programs That Can Help

Saving up for the upfront costs of homeownership takes some careful planning. You’ve got to think about your closing costs, down payment, and more. And if you don’t work with a team of experienced professionals, you could miss out on programs out there that can make a big difference for you. This is happening more than you realize.

According to Realtor.com, almost 80% of first-time buyers qualify for down payment assistance – but only 13% actually take advantage of those programs. So, talk to a lender about your options. Whether you’re buying your first house or your fifth, there may be a program that can help.

Not Leaning on the Expertise of a Pro

This last one may be the most important of all. The very best way to avoid making a mistake that’s going to cost you is to lean on a pro. With the right team of experts, you can easily dodge these missteps.

Bottom Line

The good news is you don’t have to deal with any of these headaches. Connect with CA Real Estate Group so you have a pro on your side who can help you avoid these costly mistakes.

CA Real Estate Group | Caliber RE Group

Christine Almarines @christine_almarines

Realtor DRE# 01412944 | (714) 476-4637

Anaid Bautista @wealthwithanaid

Realtor DRE# 02179675 | (949) 391-8266

Letty Luna @lettylunarealestate

Realtor DRE# 02174000 | (562) 879-4181

PT Nguyen @sellsocalbuypt

Realtor DRE# 02223919 | (714) 756-0240