Keeping Current Matters | Nov 28, 2023

When it comes to what’s happening in the housing market, there’s a lot of confusion going around right now. You may hear one thing in conversation with your friends, see something totally different on the news, and read something on social media that contradicts both of those thoughts. And, if you’re thinking about making a move, that can leave you with a lot of lingering questions. That’s where a trusted local real estate agent comes in.

Here are the top 3 questions people are asking about today’s housing market, and the data to help answer them.

Mortgage rates are higher than they’ve been in recent years. And, if you’re looking to buy a home, that impacts how much you can afford. That’s why so many buyers want to know what’s ahead for mortgage rates. The answer to that question is: no one can say for certain, but here’s what we know based on historical trends.

There’s a long-standing relationship between mortgage rates and inflation. Basically, when inflation is high, mortgage rates tend to follow suit. Over the past year, inflation was up, so mortgage rates were as well. But inflation is easing now. And this is why the Federal Reserve has recently paused their federal funds rate hikes, which means many experts believe mortgage rates will begin to come down.

And in some ways, we’ve started to see hints of slightly lower mortgage rates in recent weeks. But it’s certainly been volatile and will likely continue to be that way going into next year. Some ongoing variation is to be expected, but the anticipation is, that in 2024, we’ll see a downward trend. As Aziz Sunderji, Strategist at Home Economics, says:

“The bottom line is that interest rates are likely to be lower-perhaps even lower than many optimists think – in the weeks and months to come.”

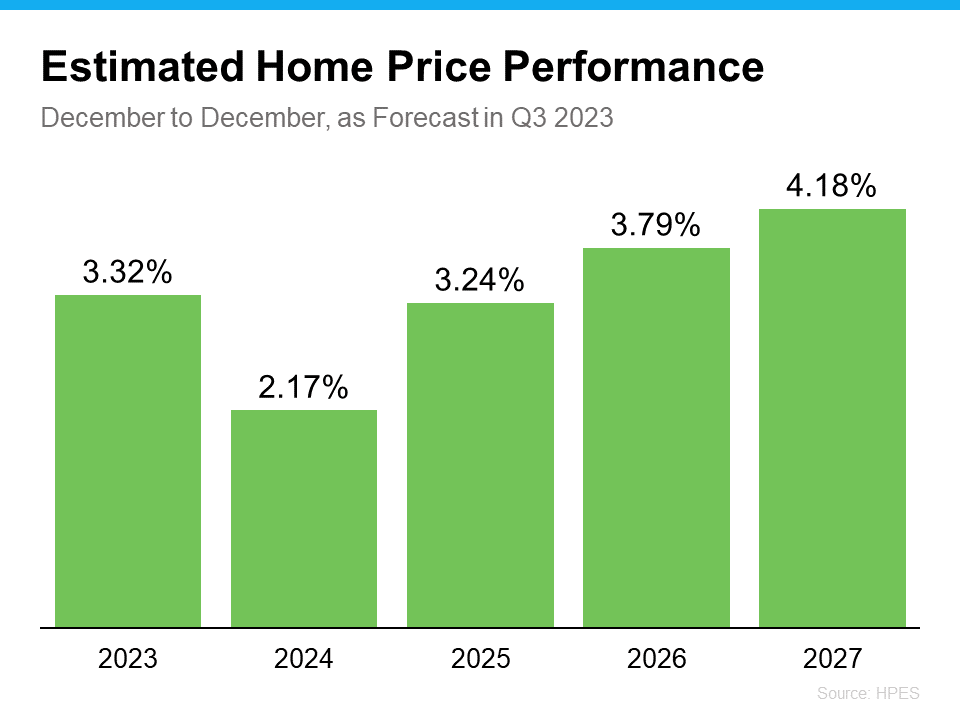

While there’s been a lot of concern prices would come crashing down this year, data shows that didn’t happen. In fact, home prices are rising in most of the nation. Experts say that trend will continue, just at a slower pace that’s much more normal for the housing market – and that’s a good thing.

To help show just how confident experts are in this continued appreciation, take a look at the Home Price Expectation Survey from Pulsenomics. It’s a survey of a national panel of over 100 economists, real estate experts, and investment and market strategists. As the graph below shows, the consensus is, that prices will keep climbing next year, and in the years to come.

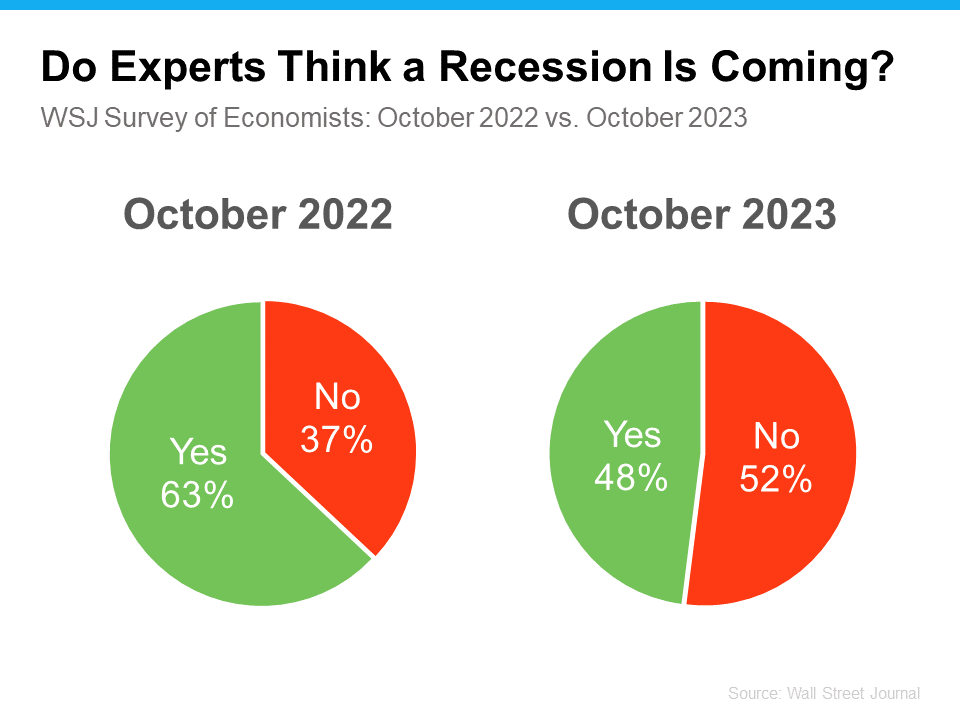

While recession talk has been a common thing over the past few years, there’s good news on that front.

The Wall Street Journal (WSJ) polls experts on this topic regularly. And last year at this time, most of them thought a recession would have happened by now. But as experts look at all the leading indicators today, they’re changing their minds and saying a recession is getting less and less likely. The latest results show that more experts now think we’re not headed for another recession (see chart below):

This is big news for the housing market. And while the 48% to 52% split may seem close to half and half, the key thing to focus on is that the majority of these experts think we’ve avoided a recession already.

The big takeaway? The data shows there isn’t cause for concern – there are actually more signs of hope. Let’s connect to talk more about the housing market questions on your mind as we head into the new year.

Keeping Current Matters | November 20, 2023

This time every year, homeowners who are planning to move have a decision to make: sell now or wait until after the holidays? Some sellers with homes already on the market may even remove their listing until the new year.

But the truth is, many buyers want to purchase a home for the holidays, and your house might be just what they’re looking for. As an article from Fortune Builders explains:

“ . . . while a majority of people take a step back from the real estate market during the holiday months, you may find when the temperature drops, your potential for a great real estate deal starts to rise.”

To help prove that point, here are four reasons you shouldn’t wait to sell your house.

1. The desire to own a home doesn’t stop during the holidays. While a few buyers might opt to delay their moving plans until January, others may need to move now because something in their life has changed. The buyers who look for homes at this time of year are usually motivated to make their move happen and are eager to buy. A recent article from Investopedia says:

“Anyone shopping for a new home between Thanksgiving and New Year’s is likely going to be a serious buyer. Putting your home on the market at this time of year and attracting a serious buyer can often result in a quicker sale.”

2. While the supply of homes for sale has increased a little bit lately, overall inventory is still lower than it was before the pandemic. What does that mean for you? If you work with an agent to price your house at market value, it could still sell quickly because today’s buyers are craving more options – and your home may be exactly what they’re searching for.

3. You can determine the days and times that are most convenient for you for home showings. That can help you minimize disruptions to your own schedule, which can be especially important during this busy time of year. Plus, you may find buyers are more flexible on when they’ll tour a house this time of year because they have more time off from work around the holidays.

4. And finally, homes decorated for the holidays appeal to many buyers. For those buyers, it’s easy to picture gathering with their loved ones in the home and making memories of their own. An article on selling at this time of year offers this advice:

“If you’re selling around a holiday and have decorations up, make sure they accent—not overpower—a room. Less is more.”

There are plenty of good reasons to put your house on the market during the holiday season. Let’s chat and see if it’s the right time for you to sell.

Keeping Current Matters | Nov 1, 2023

Maybe you’re in the market for a home and are having a hard time finding the right one that fits your budget. Or perhaps you’re already a homeowner in need of extra income or a place for loved ones. Whether as a potential homebuyer or a homeowner with changing needs, accessory dwelling units, or ADUs for short, may be able to help you reach your goals.

As AARP says:

“An ADU is a small residence that shares a single-family lot with a larger, primary dwelling.”

“An ADU is an independent, self-contained living space with a kitchen or kitchenette, bathroom and sleeping area.”

“An ADU can be located within, attached to, or detached from the main residence. It can be created out of an existing structure (such as a garage) or built anew.”

If you’re thinking about whether an ADU makes sense for you as a buyer or a homeowner, here’s some useful information and benefits that ADUs can provide. Keep in mind, that regulations for ADUs vary based on where you live, so lean on a local real estate professional for more information.

Freddie Mac and the AARP identify some of the best features of ADUs for both buyers and homeowners:

“Having an accessory dwelling unit on an existing property has become a popular way for homeowners to offer independent living space to family members.”

These are a few of the reasons why many people who benefit from ADUs think they’re a good idea. As Scott Wild, SVP of Consulting at John Burns Research, says:

“It’s gone from a small niche in the market to really a much more impactful part of new housing.”

ADUs have some great advantages for buyers and homeowners alike. If you’re interested, reach out to a real estate professional who can help you understand local codes and regulations for this type of housing and what’s available in your market.

Keeping Current Matters | Nov 3, 2023

Keeping Current Matters | Oct 24, 2023

When it comes to selling your house, you’re probably trying to juggle the current market conditions and your own needs as you plan your move.

One thing that may be working in your favor is how few homes there are for sale right now. Here’s what you need to know about the current inventory situation and what it means for you.

When you’re selling something, it helps if what you’re selling is in demand, but is also in low supply. Why? That makes it even more desirable since there’s not enough to go around. That’s exactly what’s happening in the housing market today. There are more buyers looking to buy than there are homes for sale.

To tell the story of just how low inventory is, here’s the latest information on active listings, or homes available for sale. The graph below uses data from Realtor.com to show how many active listings there were in September of this year compared to what’s more typical in the market.

As you can see in the graph, if you look at the last normal years for the market (shown in the blue bars) versus the latest numbers for this year (shown in the red bar), it’s clear inventory is still far lower than the norm.

Buyers have fewer choices now than they did in more typical years. And that’s why you could still see some great perks if you sell today. Because there aren’t enough homes to go around, homes that are priced right are still selling fast and the average seller is getting multiple offers from eager buyers. Based on the latest data from the Confidence Index from the National Association of Realtors (NAR):

An article from Realtor.com also explains how the limited number of houses for sale benefits you if you’re selling:

“. . . homes spent two weeks less on the market this past month than they did in the average September from 2017 to 2019 . . . as still-limited supply spurs homebuyers to act quickly . . .”

Because the supply of homes for sale is so low, buyers desperately want more options – and your house may be just what they’re looking for. Let’s connect to get your house listed at the right price for today’s market. You could still see it sell quickly and potentially get multiple offers.

Keeping Current Matters | October 18, 2023

If you’re considering selling your house right now, it’s likely because something in your life has changed. And while things like mortgage rates play a big role in your decision, you don’t want that to overshadow why you thought about making a move in the first place.

It’s true mortgage rates are higher right now, and that has an impact on affordability. As a result, some homeowners are deciding they’ll wait to sell because they don’t want to move and have a higher mortgage rate on their next home.

But your lifestyle and your changing needs matter, too. As a recent article from Realtor.com says:

“No matter what interest rates and home prices do next, sometimes homeowners just have to move—due to a new job, new baby, divorce, death, or some other major life change.”

Here are a few of the most common reasons people choose to sell today. You may find any one of these resonates with you and may be reason enough to move, even today.

Some of the things that can motivate a move to a new area include changing jobs, a desire to be closer to friends and loved ones, wanting to live in your ideal location, or just looking for a change in scenery.

For example, if you just landed your dream job in another state, you may be thinking about selling your current home and moving for work.

Many homeowners decide to sell to move into a larger home. This is especially common when there’s a need for more room to entertain, a home office or gym, or additional bedrooms to accommodate a growing number of loved ones.

For example, if you’re living in a condo and your household is growing, it may be time to find a home that better fits those needs.

Homeowners may also decide to sell because someone’s moved out of the home recently and there’s now more space than needed. It could also be that they’ve recently retired or are ready for a change.

For example, you’ve just kicked off your retirement and you want to move somewhere warmer with less house to maintain. A different home may be better suited for your new lifestyle.

Divorce, separation, or marriage are other common reasons individuals sell.

For example, if you’ve recently separated, it may be difficult to still live under one roof. Selling and getting a place of your own may be a better option.

If a homeowner faces mobility challenges or health issues that require specific living arrangements or modifications, they might sell their house to find one that works better for them.

For example, you may be looking to sell your house and use the proceeds to help pay for a unit in an assisted-living facility.

With higher mortgage rates and rising prices, there are some affordability challenges right now – but your needs and your lifestyle matter too. As a recent article from Bankrate says:

“Deciding whether it’s the right time to sell your home is a very personal choice. There are numerous important questions to consider, both financial and lifestyle-based, before putting your home on the market. . . . Your future plans and goals should be a significant part of the equation . . .”

If you want to sell your house and find a new one that better fits your needs, let’s connect. That way, you’ll have someone to guide you through the process and help you find a home that works for you.

View this post on Instagram

CONTACT ANY ONE OF OUR @CAREALESTATEGROUP AGENTS:

👩🏻 Christine Almarines @christine_almarines

Realtor DRE# 01412944 | 714-476-4637

👩🏻 Michelle Kim @michellejeankim_homes I speak Korean!

Realtor DRE# 01885912 | 714-253-7531

👩🏻 Anaid Bautista @singlemomrealtor I speak Spanish!

Realtor DRE# 02179675 | 949-391-8266

CA Real Estate Group | Powered by Keller Williams Realty

View this post on Instagram

CONTACT ANY ONE OF OUR @CAREALESTATEGROUP AGENTS:

👩🏻 Christine Almarines @christine_almarines

Realtor DRE# 01412944 | 714-476-4637

👩🏻 Michelle Kim @michellejeankim_homes I speak Korean!

Realtor DRE# 01885912 | 714-253-7531

👩🏻 Anaid Bautista @singlemomrealtor I speak Spanish!

Realtor DRE# 02179675 | 949-391-8266

CA Real Estate Group | Powered by Keller Williams Realty

KeepingCurrentMatters.com | Sep 13, 2023

Are you a baby boomer who’s lived in your current house for a long time and you’re ready for a change? If you’re thinking about selling your house, you have a lot to consider. Will you move to a different state or stay nearby? Is it time to downsize or do you want more space to accommodate your loved ones? But maybe the biggest consideration boils down to this – will you buy your next home or choose to rent instead?

That decision ultimately depends on your current situation and your future plans. Here are two important factors to help you decide what’s right for you.

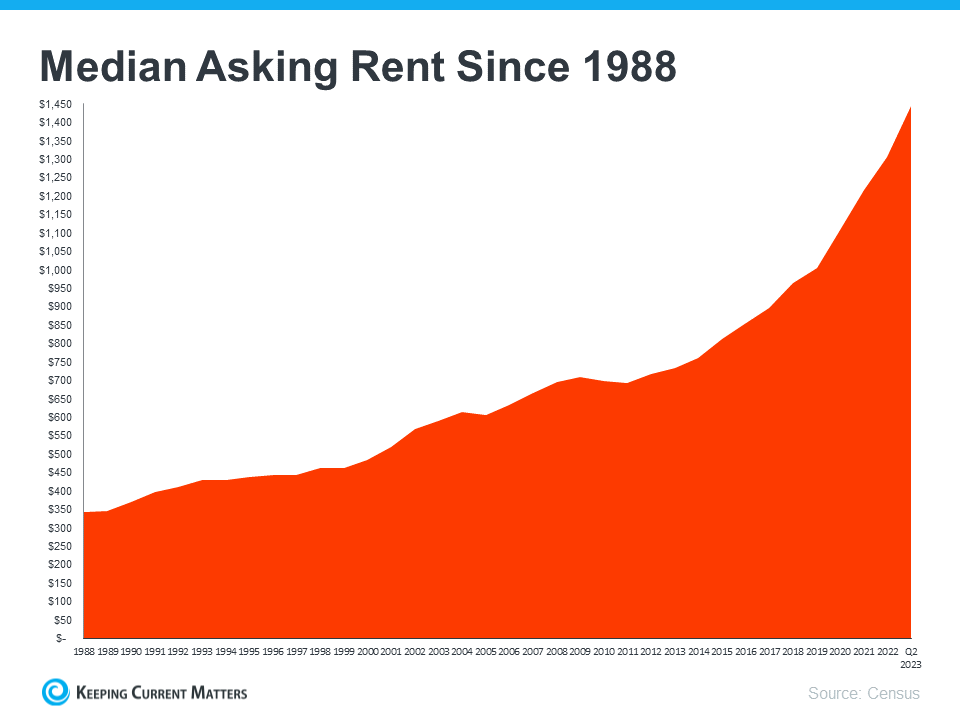

The graph below uses data from the Census to show how rents have been climbing steadily since 1988: Rents have been going up consistently over the long run. If you choose to rent, there’s a risk your rental payment will go up each time you renew your lease. Having a higher rental expense may not be something you want to deal with every year.

Rents have been going up consistently over the long run. If you choose to rent, there’s a risk your rental payment will go up each time you renew your lease. Having a higher rental expense may not be something you want to deal with every year.

When you buy a home with a fixed-rate mortgage, it helps stabilize your monthly housing payment. This allows you to lock in your monthly payment for the duration of your home loan. That keeps your payments steady and predictable for the long haul. Freddie Mac sums it up like this:

“. . . homeowners with fixed-rate loans will see little to no change to their monthly housing cost over the life of their loan. You can be confident in knowing that your mortgage payments won’t change much in the long term, even when life’s other costs do.”

According to AARP, buying your next home is a better long-term strategy than renting:

“Though each option has pros and cons, buying provides more pros, with a broader range of benefits.”

To help you choose what you’ll do after you sell, here are just a few of the benefits of homeownership that article covers:

If you’re a baby boomer who’s wondering whether you should buy or rent your next home, call Christine Almarines at CA Real Estate Group for advice at (714) 476-4637. With rents going up and homeownership providing so many benefits, it may make sense to consider buying your next home.

KeepingCurrentMatters.com | Sep 1, 2023