Here’s everything you need to know about what’s happening in the Real Estate Market.

Real Estate News in Brief

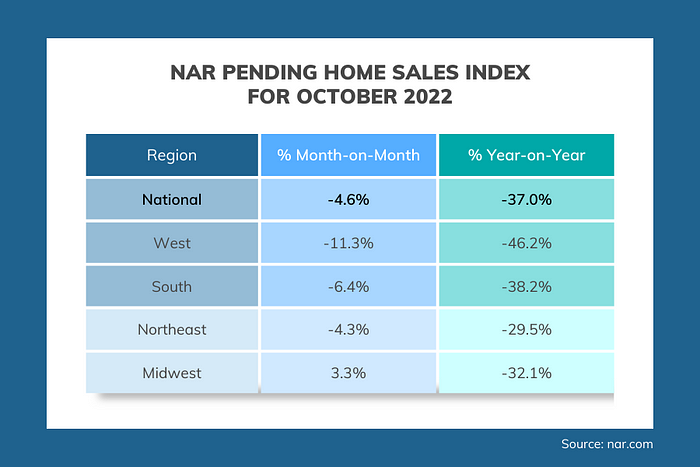

The NAR’s Pending Sales Index for October fell 4.6% in a month and 37% compared to October 2021. Pending sales in the West region were down 46%. [Source: NAR] Keep in mind that 30-yr mortgage rates were >7% for the entire month of October. They’re now around 6.3%.

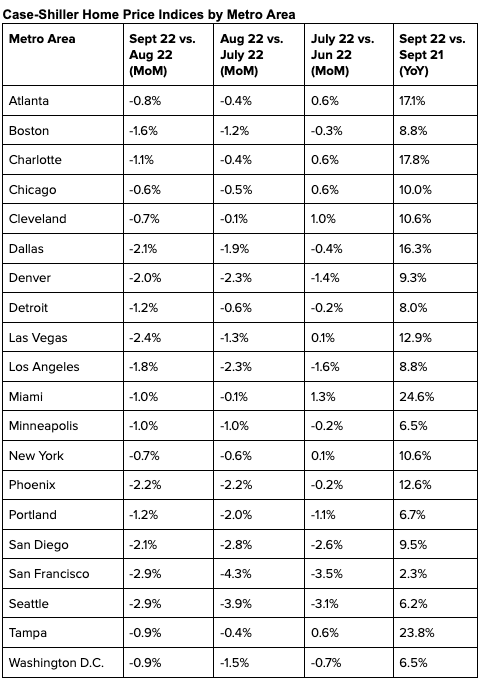

The Case-Shiller Home Price Index for September fell 1% in a month. From their peak in June, national home prices have slid ~2.5%, while prices in SFO & SEA are now down more than 10%. [Source: CoreLogic]

Fed Chair Jerome Powell said that “the time for moderating the pace of rate increases may come as soon as the December meeting” during a speech at the Brookings Institution. In other words, no more +75 bps.

The day after Powell’s comments, the PCE inflation figure for October came in at an annualized rate of 6%, better (that is to say, lower) than expectations and a further deceleration from 6.3% in September and the peak of 7% in June. [Source: BEA]

Companies added only 127k jobs in November, vs. +239k in October. This was well below Street expectations. Job losses in manufacturing & biz services dragged the total lower. [Source: ADP]

The NAHB’s Chief Economist expects a mild recession from 4Q 2022–2Q 2023, but sees mortgage rates at or below 6% by end-2023/early 2024, either because the Fed has ‘beaten’ inflation, or because the recession turns out to be bigger than expected. [Source: NAHB]

Pending Sales for October

With 30-year mortgage rates above 7% for the entire month, we knew that October pending sales would be bad — and they were. The NAR’s Pending Home Sales Index (PHSI) dropped 4.6% in a month. That’s the 5th-straight monthly decline in the PHSI. Compared to October 2021, the PHSI was down 37% YoY.

The contraction was significantly worse in the West, with October pending sales dropping 11% MoM and down 46.2% YoY. That’s right, pending sales nearly halved in the West.

Pending sales are a forward indicator of existing home sales (leading by 1–2 months). So prepare yourself for some nasty November and December existing home sales figures.

But there’s a silver lining: mortgage rates are already 90–100bps (a full percentage point) lower. As NAR’s Chief Economist Lawrence Yun wrote, “October was a difficult month for buyers as they faced 20-year-high mortgage rates…[but] The upcoming months should see a return of buyers as mortgage rates appear to have already peaked and have been coming down since mid-November.”

In fact, there are signs that a recovery in activity (thanks to lower rates) is already happening. The MBA (Mortgage Bankers Association) tracks new purchase loan applications on a weekly basis. This is the fourth week in a row that applications have risen week-on-week.

Case-Shiller for September

For the third consecutive month, home prices declined on a month-over-month basis. The national index was down 1.0% MoM, but the 20-city index was down 1.5% MoM. Don’t be fooled by the small numbers; these are big decreases. If this happened every month, prices would be down 12–18% in a year.

As in August, prices declined in each of the 20 big cities. However, for the cities experiencing the sharpest price drops (San Francisco, Seattle, Las Vegas etc.), the magnitude of price declines actually slowed a bit in September.

NAHB Webinar

Here’s how the National Association of Homebuilders’ Chief Economist, Robert Dietz, sees things:

2020–2021: Unsustainable, above-trend growth in home sales

2022–2023: Compensating below-trend growth in home sales

2024+: A return to trend growth in home sales (with >1 million in new home sales annually)

He expects a mild recession for the next three quarters, unemployment rates rising to near 6% (from 3% today) in 2024 and national home prices falling ~10%. At the same time, his message was essentially optimistic — lower inflation, interest rates and home prices will bring buyers (and builders) back relatively quickly.

A few anecdotes I found interesting:

- ~50% of the webinar attendees (most of whom were builders) said that they were responding to slowing demand with either price cuts OR enhanced incentives

- The construction industry needs ~750,000 new workers every year to keep pace with demand and replace retirees

- Right now, two cities in Texas (Houston and Dallas) are adding more new homes than the entire state of California

Note: In any given year, existing home sales are 7–15 times higher than new home sales. This isn’t because builders are lazy. It’s because there are around 145 million existing housing units. Even if builders were able to construct 2 million homes a year (something they’ve never achieved before), that would only raise the total housing stock by 1.3%.

Mortgage Market

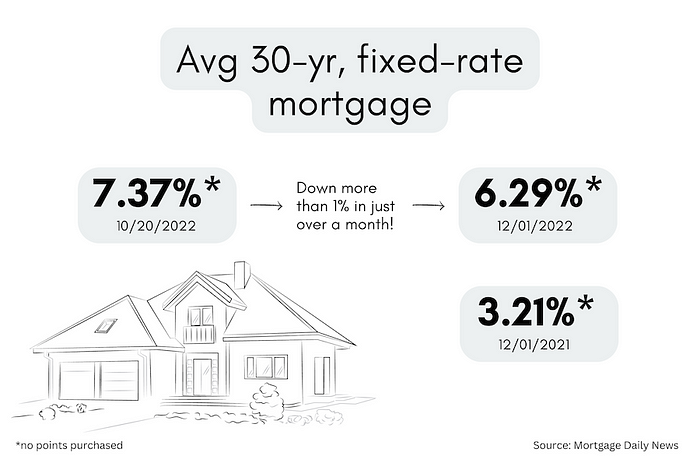

After months of extreme volatility, 30-yr mortgage rates had flatlined at 6.6% for several weeks. But with another good (well, improving) inflation figure, and Powell sounding a bit less hawkish, the bond market was in party mode yesterday, rising 70–80 basis points.

Higher mortgage bond prices = lower mortgage bond yields = lower mortgage rates. Yesterday, the 30-yr mortgage rates moved sharply lower to 6.3% — that’s a full percentage point lower than the peak of 7.37% on October 20!

They Said It

“When home prices decline, it’s pretty rare for there to not be a recession.” — NAHB Chief Economist Robert Dietz

“To anyone with a sense of history, the home boom must be a source of wonder. Housing usually leads the economy into a recession. Mortgage rates rise, then housing construction and home sales fall.” — Robert J. Samuelson in a 2002 Newsweek article

Inspiration

There are many different approaches to measure ‘affordability.’ But they all depend on three factors: 1) household income, 2) home prices, and 3) mortgage rates.

Right now, all three factors are moving in buyers’ favor:

- Workers are getting paid more

- Home prices are starting to slide

- Mortgage rates have peaked

Plus, there are more homes available, and less competition than last year, and sellers are more willing to negotiate on things like repairs, covering some closing costs, paying for points etc.

The key is to stay in regular contact with CA Real Estate Group. Your agent will let you know about price cuts, point out stale listings, and will keep you informed about mortgage rates. Also, waiting for the ‘perfect’ moment could be counterproductive. When (if!) conditions look perfect, they’ll look perfect to everybody else too.